Land & Property Services

Introduction

- I am required under the Accounts Direction given by the Department of Finance in accordance with Section 11(2) of the Government Resources and Accounts Act (Northern Ireland) 2001 to report my opinion as to whether the financial statements give a true and fair view. I am also required to satisfy myself that, in all material respects, expenditure and income have been applied to the purposes intended by the Northern Ireland Assembly and conform to the authorities which govern them; that is, they are ‘regular’.

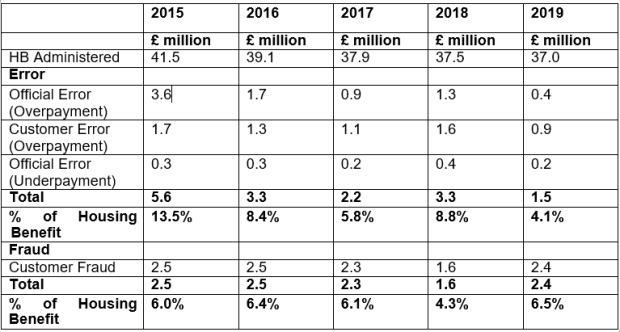

- LPS administers housing benefit1 for rates of owner occupiers on behalf of the Department for Communities (DfC). Unlike all other Social Security benefits where payments are made, LPS administers housing benefit in Northern Ireland by offsetting housing benefit against the rate accounts of people who own their own house but are entitled to apply for a reduction as they are on low income and suffering financial hardship. There is estimated to be a substantial amount of fraud and error within these transactions amounting to 10.6 per cent2 of LPS total housing benefit expenditure of

£37.0 million as per Figure 1. This is a decrease of 2.5 per cent compared to the 13.1 per cent recorded last year.

- The Rate Relief Regulations (Northern Ireland) 2017 came into operation on 27 September 2017 aligning with the operation of Universal Credit3. This legislation introduced a new Rate Rebate Scheme administered by LPS for those in receipt of Universal Credit.

- In 2019-20 LPS administered £3.3 million of rate rebate that is reflected in the LPS Trust Statement. LPS estimated the amount of fraud and error within these transactions to be 7.2 per cent of LPS total rate rebate expenditure4.

- I consider the level of fraud and error in housing benefit expenditure to be material. Therefore my opinion on the regularity of this benefit expenditure is qualified.

- I do not consider the level of fraud and error in rate rebate expenditure to be material for the year ended 31 March 2020. However, this will be kept under consideration as more claimants migrate to Universal Credit and new claims for Universal Credit increase, particularly due to the impact of COVID-19, resulting in greater eligibility for the Rate Rebate Scheme.

Basis of Qualification

Fraud and Error- Housing Benefit

- DfC’s Standards Assurance Unit (SAU) reported in March 2020 the extrapolated levels of fraud and error for housing benefit administered by LPS during the calendar year 1st January to 31st December 2019. This report highlights estimated levels of fraud and error amounting to £2.4 million and £1.5 million respectively.

- Figure 1 below shows that the level of error has decreased from £5.6 million in 2015 to

£1.5 million in 2019 over the five year period.

Figure 1: Estimated fraud and error in Housing Benefit administered by LPS deemed to be irregular

Source: Analytical Services Unit, DfC

The total percentage of Fraud and Error in 2019 figures is 10.6 per cent of the HB administered by LPS.

- I recognise that over a number of years LPS has made considerable efforts to improve fraud and error rates but the increase in Customer fraud by 50% from 2018 is concerning. My opinion on regularity therefore remains qualified.

Other Matters

- There are a number of matters referenced in the Performance and Accountability Report and the Governance Statement in the accounts. I note specifically the following matters:

Outstanding Valuation Caseload

- There has been an increase in the outstanding non-domestic valuation caseload with 5,472 cases outstanding at 31 March 2020 (3,973 cases at 31 March 2019). There has also been a rise in the number of domestic cases outstanding, 12,580 at 31 March 2020 compared to 11,054 at 31 March 2019.

- The estimated impact on the rate revenue figure of the outstanding domestic and non- domestic caseload at 31 March 2020 is £8.0 million. This is a decrease of £0.7 million from 31 March 2019.

Vacancy Discharges

- The estimated level of error in the overall vacancy discharge figure of £42.3 million is 4.25% although this is likely to be overstated due to inspections being targeted at higher value properties. When LPS find that a ratepayer has been in occupation of a property (whether via a vacancy inspection or otherwise), the correct assessment is back-dated to when occupation began and therefore no revenue is lost.

- LPS plans to continue their existing inspection programme in partnership with Councils and to trial new methods of data sharing and collection to identify at the earliest opportunity vacant properties that have become occupied. Data is being provided by LPS to assist with a data matching and analytics Council-led initiative to identify properties for inspection with a high probability of occupancy. LPS does not, however, have a vacancy inspection target in the 2020-21 year due to the restrictions associated with Covid-19. Vacancy inspections are likely to progress again during the 2021/22 rating year.

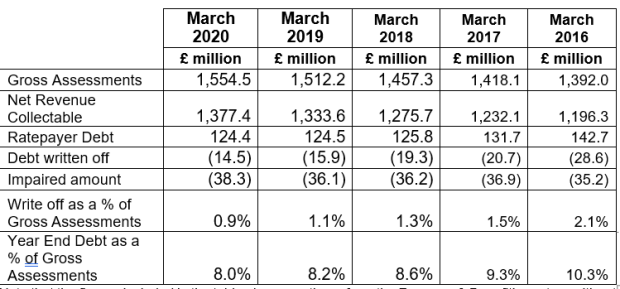

Ratepayer Debt

- Figure 2 below shows the level of ratepayer debt of £124.4 million at 31 March 2020. Debt written off in year was £14.5 million and impaired debt, which is unlikely to be repaid in full, amounted to £38.3 million at 31 March 2020.

Figure 2: Trends in Ratepayer Debt

*Note that the figures included in the table above are those from the Revenue & Benefit’s system without the Year End accounting adjustments (e.g. accrued income & losses) and as such differ slightly from the figures in the Financial Statements.

- I recognise the improvement by LPS through its debt management strategy but there is still £124.4 million ratepayer debt outstanding which is not available for public use. LPS

have pointed out this includes late rate assessments and debt that is under a payment arrangement and the majority of the debt outstanding at year end is expected to be recovered. It is therefore important that all necessary steps are taken to maximise recovery.

Small Business Grant Scheme

- Expenditure on the small business grant scheme is not included in the LPS Trust Statement (Rate Levy Accruals Account). The Department for the Economy (DfE) assumed responsibility on behalf of the Executive for the scheme, including any potential error, fraud or losses arising from the administration of the scheme. DoF (via LPS) was responsible for the identification and checking of eligible businesses and making the payments to those businesses. Ratepayers’ information was used to determine who was eligible to receive the grant.

- The Small Business Grant Scheme was launched by DfE on 26 March 2020. Its purpose was to provide one-off emergency grants of £10,000 to small businesses to help mitigate the potential threat of business closures arising from the COVID-19 pandemic.

- The scheme was required to be designed and delivered by DfE and LPS at a rapid pace, giving rise to a number of potential risks. It was in recognition of these particular circumstances that a Direction from the Economy Minister was issued.

- During the course of the DfE audit process, NIAO reviewed the scheme payments made by LPS. The sample testing identified three errors amounting to a total of £30,000. This was extrapolated to indicate a total possible payment error rate of 6.1%.

- These payments have been paid to participants who are not eligible under the scheme and are therefore irregular. As DfE was responsible for the scheme, I qualified my regularity opinion in respect of their accounts as the expenditure does not conform to the authorities which govern it. This qualification also applied to Invest NI who were responsible for recording the costs of the scheme.

- It was always my intention to carry out further work on the scheme as part of the DfE 2020-21 audit. However, since I reported on this scheme, some further information has emerged and I decided to initiate an earlier review of the scheme.

- This review will focus on elements of the scheme from which lessons can be learned. It will involve some further testing of payments and more broadly will look at the key decisions taken at the earliest stages of the scheme’s development around how need was identified and the approach taken to address it. I also intend to look at decisions around scheme eligibility and how these were applied, as well as reviewing the work done to date by the Strategic Oversight Group. I will attempt to reflect the economic and political context in which the scheme was conceived and delivered, including the need for a Ministerial Direction. Whilst there has been some delay in obtaining information relating to this work, I aim to publish my report in April 2021.

COVID-19 Related Issues

- The minister for finance announced a rate support package for businesses as a result of COVID-19. This package was in the form of a rates holiday for the first four months of the 2020-21 year for all non-domestic properties (with the exception of Utilities and public bodies) and a full year’s holiday for all non-domestic properties in the retail, hospitality, leisure and tourism sectors. This package is estimated to cost up to £317

million and will be funded directly from the regional rate. As such, cash collected during 2020-21 will be much lower than that collected in recent years.

- LPS together with the Society for Local Authority Chief Executives (SOLACE) engaged with the University of Ulster’s Economic Policy Centre to carry out some analysis of the rate base resulting from the COVID-19 pandemic. LPS has told me they are reviewing the results of this research with Councils to identify any impacts on the estimated rates revenue funding levels for Councils and the NI Executive in 2021-22. LPS however believe that the rate support offered will mitigate the risk of substantial revenue reductions, pending decisions taken by the executive.

Update on Application Based Rebate Fraud

- I have previously provided details on a fraud perpetrated by a member of LPS staff in 2014. The total value of the fraud was £130,000 and to date LPS has retrieved

£97,500. LPS have told me that this case is now closed and the remaining balance has been written-off.

Additional Fraud Occurrence in 2019

- In recent years there have been 2 significant fraud cases in LPS involving employees. Details on the first fraud case are contained in my report attached to the 2016-17 LPS accounts, which can be found on the Department of Finance’s website.

- In June 2019, LPS informed me of the second internal fraud. This related to the misappropriation of refunds due on customer accounts. The LPS investigation has examined approximately 2000 refunds the staff member was involved in approving over a 12 year period. LPS has identified the suspected misappropriation of 56 refunds by the staff member with a total value of £125,000. The staff member was dismissed in October 2019.

- In December 2019, following additional information identified by the PSNI investigation, LPS is exploring further possible fraudulent activity by the same staff member. The PSNI have completed their investigation and the matter is now with the Northern Ireland Courts and Tribunal Service. I will report further on this case when the judicial process is complete.

- I will also revisit the matters above as part of the 2020-21 audit of the LPS Rate Levy Accruals Account.

KJ Donnelly

Comptroller and Auditor General Northern Ireland Audit Office 106 University Street

Belfast BT7 1EU

19 February 2021