Introduction

- Invest Northern Ireland (Invest NI) is a Non-Departmental Public Body, established in 2002 to grow the local economy by helping new and existing businesses compete internationally and by attracting new investment. Invest NI is a separate legal entity with its own independent board and Accounting Officer. It is sponsored by the Department for the Economy (the Department), but it is not part of the Department nor are its financial statements consolidated with those of the Department. In 2020-21 it recorded£508.1 million (2019-20, £175.8 million) of grant-in-aid funding from the Department; a significant proportion of the funding related to COVID-19 business support grants to Northern Ireland businesses.

- Given the political and economic concerns at the time, these grant schemes were delivered at extreme pace and in a challenging environment. The situation was made worse by the imposition of home working and a lack of appropriate resources. Given the urgency and speed with which these schemes were designed and delivered, the accounting treatment, and consequently the audit activity, has been complex and at times, a challenge.

Purpose of the Report

- I am required to examine, certify and report upon the financial statements prepared by Invest NI under the Industrial Development Act (Northern Ireland) 2002. I have modified my opinions on the Invest NI financial statements for the year ended 31 March 2021, this report explains the reasons for the modifications.

- I have provided adverse audit opinions1 due to COVID-19 business support grant expenditure totalling £140.8 million in 2020-21 and £220 million in 2019-20, together with related transactions and balances, which was controlled and administered by the Department but was, in my view, incorrectly recorded in Invest NI’s financial statements. In my view this expenditure was also therefore irregular since reliance cannot be placed on Invest NI’s legal powers to confirm that the expenditure was regular. Further details on the rationale for my opinion on the regularity of this expenditure are provided in paragraphs 7 and 17 of this report.

- Had I not provided adverse audit opinions, I would have disclaimed my regularity audit opinion because of limitations in the scope of my work due to insufficient evidence available to satisfy myself that £129.8 million of COVID-19 business support grants complied with the schemes’ eligibility criteria. A further issue would have led to a qualification of my regularity audit opinion had the issues noted above not been present. This related to irregular expenditure of £10.4 million of Expected Credit Losses and irregular income of £0.4 million of interest income, relating to a £14.2 million loan made in previous years to Glenmore Generation Limited. The Department of Finance considered this loan to be irregular, because certain conditions of its approval had not been complied with.

Adverse True and Fair audit opinion

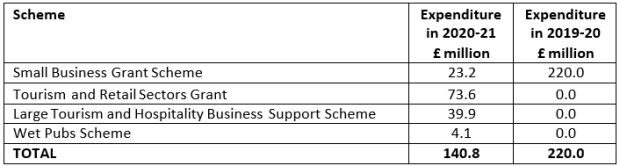

- Invest NI’s financial statements include expenditure on a number of COVID-19 emergency business support grants totalling £140.8 million in 2020-21, and £220 million in 2019-20, which were administered and paid by the Department. Neither Invest NI nor any of its staff were directly involved in the delivery of the schemes. A breakdown between the schemes is provided in Figure 1.

Figure 1: Department for the Economy administered COVID-19 business support schemes

Source: Invest NI 2020-21 Annual Report and Accounts

- Despite the schemes being administered and paid by another rganization, rather than by Invest NI, the expenditure was included in Invest NI’s financial statements, under the instructions of the Department. This unusual accounting arrangement was used because the Department did not have the legal authority to make the required payments itself. The aim of this arrangement was to reflect scheme expenditure in the entity with the appropriate legal authority to make the payments. Invest NI has the relevant authority under the Industrial Development (Northern Ireland) Order 1982. So essentially the Department designed and delivered these schemes and incurred the expenditure, while instructing Invest NI to include the expenditure in its accounts on the basis that it had the correct legal powers. However, neither International Accounting Standards nor the Government Financial Reporting Manual (FreM) allow for legal vires as a basis for recognition.

- The Department, Invest NI, DoF’s Land & Property Services (LPS) and Account NI all agreed a Memorandum of Understanding (MOU) which set out the roles and responsibilities of those involved in the policy, design, operation and delivery of the Covid-19 business support grants. In the MOU, the sole duty allocated to Invest NI is to “record the full estimated costs of the grant scheme on an accruals basis in 2019-20 budgets and accounts”. However, the primary duties in relation to establishing the scheme, its design and delivery, payment approval and taking responsibility for any losses arising from its administration, were allocated to, and accepted by, the Department. While there was some early consultation with Invest NI on the scheme, no Invest NI staff were involved in scheme delivery and Invest had no role in the payments that were made to grant recipients.

- Invest NI is required to provide financial statements which show a true and fair view of its financial transactions and its financial position. Therefore, including the expenditure of another entity led to misstatements within the Invest NI’s accounts, both in 2020-21 and 2019-20. I have therefore qualified my audit opinion on the financial statements.

- The Department consulted with the Departmental Solicitor’s Office (DSO) and the Department of Finance (DoF) on this novel accounting treatment and both bodies gave their support to it. However, the legal advice is not based on the application of relevant accounting standards and DoF, although supportive, did not issue an accounts direction to the Department to provide a clear basis for the approach taken. It is a requirement of my role to form an independent audit opinion on whether the financial statements reflect a true and fair view, and comply with accounting standards and the Government Financial Reporting Manual. Since the Department controlled and administered the scheme and made the payments to recipients, without any meaningful involvement of Invest NI, it is my opinion that this money was not spent by Invest NI and therefore should not have been recorded in its financial statements.

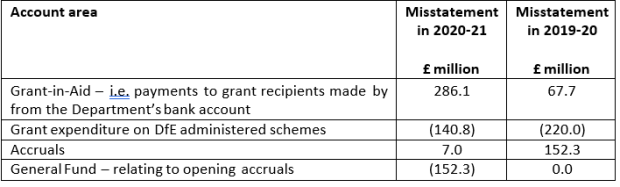

- In addition to the grant expenditure in Figure 1, Invest NI also included notional grant-in-aid from the Department of £286.1 million (2019-20, £67.7 million), representing payments made by the Department to grant recipients of these schemes, and included related accruals of £7.0 million (2019-20, £152.3 million). In my opinion, Invest NI did not have an obligation at 31 March 2020 for these schemes since it was not involved in controlling or delivering them and therefore should not have reflected an obligation for accruals within its 2019-20 financial statements. I have also taken these misstatements into account in determining my audit opinion.

Figure 2: Misstatements resulting from the accounting treatment for Department for the Economy administered COVID-19 business support schemes

- This is a matter of ‘substance over form’, an accounting concept which means that, in order to present a true and fair view, financial statements should reflect the economic substance of transactions or events, not their legal form. Financial statements representing a legal form that differs from the economic substance, do not result in a faithful representation. Following a detailed technical review, it is my opinion that the economic substance of the grant schemes outlined in figure 1, is that the Department, not Invest NI, controlled and delivered the schemes and made the payments to recipients with assistance from the Land and Property Services (LPS). As a result, these transactionsshould not have been recorded in Invest NI’s financial statements. I also note that the Invest NI Accounting Officer had no opportunity to govern those schemes or influence the expenditure.

- I provided Invest NI with an opportunity to reconsider its accounting treatment and proposed that it make an adjustment to its financial statements to rectify the issue. There was constructive engagement on this issue and Invest NI demonstrated openness to my recommendation, however, Invest NI understandably wanted to wait until the Department decided its course. Following a decision by the Department not to adjust its own accounts, Invest NI took the same position.

- Invest NI operates under a Management Statement and Financial Memorandum (MSFM) with the Department which states that “accounts be prepared in accordance with any directions issued by the minister, Department or DoF”. While Invest NI was instructed by the Department to account for the expenditure in this way (see paragraph 7 above) that instruction does not, in our view, constitute an Accounts Direction. Therefore, I must provide my opinion on the basis of my disagreement with the accounting treatment of these grants and the associated grant-in- aid and accruals, since in my opinion they should not have been included in Invest NI’s financial statements.

- The COVID business support grant schemes administered by the Department in 2020-21 of

£140.8 million (2019-20: £220 million), and the related transactions, are a substantial proportion of total operating expenditure reflected in Invest NI’s financial statements. Given its relative size and that of the associated grant-in-aid and accruals recognised for these transactions, I have determined that the financial statements do not show a true and fair view of Invest NI’s income and expenditure or of its’ state of affairs at 31 March 2021, or for the prior year.

Adverse opinion on the regularity of income and expenditure

COVID-19 grant schemes administered by the Department for the Economy

- In addition to forming an opinion on whether the financial statements show a true and fair view I am required to give an opinion on the regularity of transactions, by considering if the income and expenditure has been applied for the purposes intended by the Assembly and whether the transactions comply with the authorities which govern them.

- Since, in my opinion, it was the Department and not Invest NI which expended £140.8 million on the COVID-19 business support grants referred to in Figure 1 in 2020-21 (2019-20 £220 million), reliance cannot be placed on Invest NI’s legal powers under the Industrial Development (Northern Ireland) Order 1982 to prove the regularity of these transactions. Given these grants form a substantial proportion of the financial statements, in the absence of the Department having sufficient powers in place itself I have concluded that the income and expenditure have not been applied to the purposes intended by the Assembly and that the financial transactions recorded in the financial statements do not conform to the authorities which govern them.

COVID-19 grant schemes administered by Invest NI

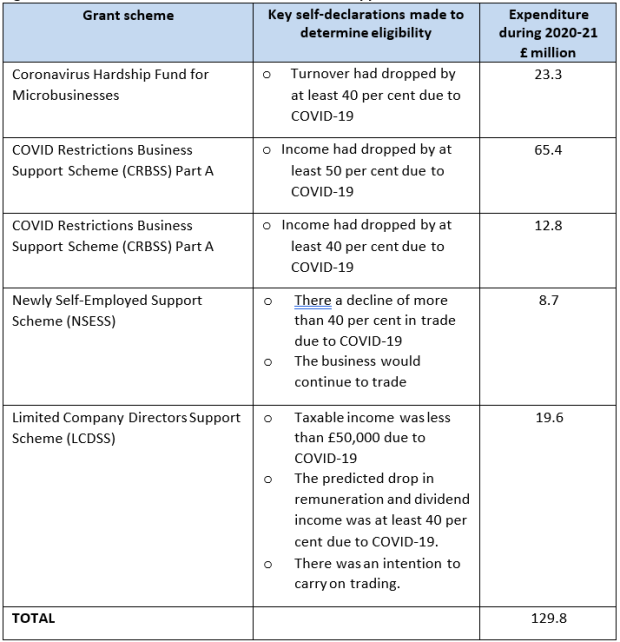

- In addition to the grant schemes shown in Figure 1 which were administered by the Department, a number of new support schemes were launched and administered by Invest NI in 2020-21 in response to the continued impact of the pandemic on Northern Ireland’s economy. As part of my work to provide an opinion on the regularity of transactions, I must gather independent audit evidence to assess whether a sample of grants administered by Invest NI complied with the eligibility critieria established for each scheme. All of these schemes were designed to rely upon self-declarations made by applicants to confirm eligibility. Therefore, Invest NI could not provide me with sufficient appropriate audit evidence to verify whether the self-declarations made were, in fact, accurate and to allow me to determine whether all of the eligibility criteria relating to expenditure totalling £129.8 million had been met for the Invest NI administered COVID-19 business support grant schemes set out in Figure 3 below. There were no alternative audit procedures available to me to obtain sufficient appropriate audit evidence to inform my regularity audit opinion.

Figure 3: Invest NI administered COVID-19 business support schemes

Source: Invest NI 2020-21 Annual Report and Accounts

- Approval for the implementation of the new schemes was by Ministerial Direction, since the Department’s Accounting Officer was unable to provide evidence that these schemes would provide value for money or that there would not be an unacceptably high risk of error or loss of funds. Reliance on self-declarations without corroborating evidence does not mitigate the risk of fraud and error occurring. Whilst I recognise that clawback arrangements were built into the terms and conditions of these grants, the subsequent identification of fraud or error will take significant administrative effort and the recovery of sums may not be successful.

- The DoF published the Cabinet Office’s ‘Fraud Control in Emergency Management: COVID-19 UK Government Guide ‘2, which outlines the steps which should be undertaken by government bodies when administering emergency programmes. One of the overarching principles it highlights is that there is an inherently high risk of fraud in this context and therefore fraud risk assessments should be undertaken and continually updated for new threats and risks. Given that these schemes have already made payments that are at risk of fraud, it is important that post payment checks are now undertaken. I therefore recommend that post payment checks are performed, proof of eligibility from corroborating evidence is sought and, where necessary, funds are recouped. I understand the Department for the Economy is undertaking work in this area and I will review its outcome.

- I would also expect Invest NI to ensure that it continues to comply with the Cabinet Office guidance for any future schemes of this nature and draws on lessons learnt, by building suitable control mechanisms into them to prevent and detect fraud and to protect public funds.

- I consider this expenditure to be a significant proportion of the expenditure in the year. As a result, had I not already provided an adverse audit opinion on the regularity of income and expenditure, I would have been unable to form an opinion on whether the income and expenditure has been used for the purpose intended by the Assembly and the transactions conform to the authorities which govern them, and would have disclaimed my regularity audit opinion.

Irregular expenditure relating to a loan provided by Invest NI

- In addition to the issues described in paragraphs 16-17 and 18-22 above, an irregularity was brought to my attention by the DoF , when it determined that a £14.2 million loan made by Invest NI to Glenmore Generation Limited (Glenmore) did not comply with its conditions of approval. Expenditure of £10.4 million for expected credit losses and income of £0.4 million, related to the loan, which were reflected in Invest NI’s 2020-21 financial statements are therefore irregular. Again, had I not already provided an adverse regularity opinion, I would have qualified my regularity audit opinion for the income and expenditure relating to the loan in the 2020-21 financial statements. Further details of this issue are provided in paragraphs 26- 34 of this report.

Other issues identified during the audit of the COVID-19 business support schemes which did not impact on the audit opinion

- In December 2021 I issued a report on the Design and Adminstration of the Northern Ireland Small Business Support Grant Scheme administered by the Department, which highlighted the inherent risks of implementing such a scheme at extreme pace. The DfE Accounting Officer requested a Minsterial Direction for the scheme, stating that he had insufficient evidence it would provide value for money and that a risk to public funds due to fraud or error was present.

- Ministerial Directions were requested for all of the COVID-19 business support grant schemes administered by Invest NI, citing similar issues. We accept that these schemes were delivered in response to an emergency situation, nonetheless, public funds may be at risk, particularly in light of self-declarations being accepted by the organisation as proof of eligibility. It also means that the eligibility criteria set may have resulted in some businesses receiving a grant who did not need it. I noted that for the CRBSS, the eligibility criteria did not take account of previous

earnings and in some cases businesses received more money from the grant scheme than they would have trading normally. This may also be the case for the NSESS.

Irregular expenditure and income relating to a loan provided by Invest NI

- In August 2021 the Department of Finance advised me that it considered a £14.2 million loan made to Glenmore Generation Limited (Glenmore) by Invest NI since 2015 to be irregular because it did not comply with the conditions DoF Supply had imposed at the time it had originally approved the loan.

- During 2020-21 Invest NI provided for an impairment loss of approximately £10.4 million against this loan, having already provided for £3.8 million in earlier years. Under International Financial Reporting Standard (IFRS) 9 – Financial Instruments – this impairment is known as an Expected Credit Loss and is used to reflect the expectation that anticipated repayments might not take place. Interest of £0.4 million earned during the year on this loan was also reflected in the 2020- 21 financial statements. Since the loan was subsequently approved for write off, this interest income has now ceased. As the original loan is irregular, all expenditure and income streams flowing from the loan now also become irregular. I would have therefore qualified my audit opinion on the regularity of income and expenditure due to the irregular expenditure of £10.4 million of Expected Credit Losses and £0.4 million of interest income related to the loan which are reflected in the 2020-21 financial statements, since they do not conform to the authorities which govern them.

A loan was made to Glenmore Generation Limited but there were issues with its recoverability

- In 2015, Invest NI developed a business case and received approval from the DoF and DETI (now DfE) Ministers to support the development of an anaerobic digestion plant at the Glenmore Estate in County Donegal under the Sustainable Utilisation of Poultry Litter scheme. The intent was to facilitate the export of poultry litter from NI and subsequently the importation of the biogas produced to generate renewable energy for use by companies based in NI. The total cost of the project was estimated as £24.3m, with £1 million being input by the project promoter and main contractor. The promoter was the ultimate owner of Glenmore Generation Limited (Glenmore). Of the remaining £23.3 million funding requirement, Invest NI would contribute 40 per cent (£9.3 million), which would be drawn down in tranches, and a private sector partner would supply the remaining 60 per cent (£14.0 million). The financing offered by Invest NI was issued as a loan to be repaid over a period of 15 years. Interest was charged at a rate of 12 per cent during the construction phase and at 10 per cent thereafter on an equal footing basis3 with the private sector partner’s financing, where neither obligation ranked above the other if repayment was triggered. DoF Supply approval is required when expenditure proposed by central government bodies is outside of the delegations permitted by the DoF. In this case approval was required due to the quantum of the loan and DoF approval was given August 2015, with certain conditions attached.

- The anaerobic digestion plant suffered significant commissioning issues and the plant was struggling to ramp up production to profitable levels. Over the course of the project additional funding was required, with the Invest NI Board approving funding of £0.9 million in August 2018 for additional project costs outside of the scope of the original offer. Not all of the original £9.3 million loan facility approved by DoF Supply had been drawn down, meaning that the overall

value of the Invest NI loan remained within the limits initially approved by DoF Supply. However, as a result of approximately £10.5 million, including rolled-up interest, of further funding being provided by the private sector partner in August 2017, January 2019 and May 2019, seniority rankings changed. This meant that the private sector partner now held seniority for loan recovery over the initial loans from both parties. DoF Supply was not informed of this change in rankings.

- In response to ongoing losses and an unsustainable debt burden Glenmore’s directors obtained professional advice and sought an expedited sale of Glenmore. Ultimately a sale to a third party could not be achieved and Glenmore was refinanced and remained under the control of the project promoter. Invest NI received separate professional advice that the offer would provide no financial return to Invest NI, however the refinancing allowed the best, and possibly only, opportunity for the project to be turned around so that it might fulfil the dual benefits envisaged by Invest NI to sustainably use poultry litter and provide biogas for NI companies. The reason that the offer would not provide a financial return to Invest NI was because it was less than the

£10.5 million of additional funding provided by the private sector partner, and as such the senior debt with that partner held preference. The private sector partner will also lose all of its original loan and is unlikely to recover all of its additional £10.5m funding.

Invest NI requested DoF approval to write off the full amount of the loan

- On 2 April 21, Invest NI approached the DoF, through its sponsor department (DfE) for approval to write off a loss totalling £14.2 million on the loan to Glenmore (comprising loans of £9.3 million and accumulated interest owing of £4.9 million). This approval was required urgently to allow the refinancing offer to proceed and DoF approval for this request was initially granted. However the DoF subsequently reviewed in detail a report on the Glenmore project, commissioned by Invest NI’s Board and written by its internal auditors. As a result the DoF noted several issues, leading it to conclude the loan was irregular because several conditions attached to its approval for the original loan had not been met. Issues identified included:

-

- Invest NI relied on the private sector partner’s conclusion that preconditions for the loan had been met prior to drawdown, rather than undertaking work and concluding itself4, as required by the DoF.

-

- The DoF Supply team should have been advised of all proposals specifically relating to the refinancing of the debt as a condition of its approval of the loan. However, the following had not been brought to its attention:

- The scope and scale of the project, and associated risks, had been substantially changed due to the private sector partner’s additional financing holding seniority.

- The repayment period had been extended from 15 to 17 years, and no repayments had been made in line with the anticipated schedule.

- The refinancing proposal had not been notified to the DoF prior to the write-off request.

- The project promoter’s financial position had deteriorated during the course of the loan, affecting the viability of the £1million guarantee offered and the risk profile of the project.

-

- A risk register for what had been a high risk project at the outset had not been maintained. Papers provided to the DoF Supply team during the approval process noted the risk profile of the loan and that Invest NI’s investment would be on an equal footing basis. DoF approval was given on the basis of this assurance as to how risk would be managed.

- The DoF was also concerned that Invest NI had not advised it immediately of the internal audit findings issued on 5 March 2021 and that the change of circumstances was only notified to the DoF when the request for write off approval for the loan was submitted on 2 April 2021. Invest NI told DoF that it did not believe irregular spend had been incurred. It did not seek retrospective approval, however DoF Supply noted that, even if it had made such as request, the requirements for retrospective approval would not have been met.

- I asked Invest NI to explain why it had not identified the need to seek DoF approval during the course of the loan as circumstances changed and what action it was taking to prevent this happening in future. It told me;

“As the project proceeded, some of the identified risks materialised with further funding required to continue operations. Invest NI consulted with DfE on whether this was a material change that would be required to revert to DoF Supply for further approval. However, this assessment and discussions with DfE centred on whether or not there was a change in scale or scope and it was agreed that the scope of the project was largely the same although the scale, measured by way of the total investment, was greater. There were exceptional circumstances that led to an increase in costs related to the project that were neither planned nor anticipated but we took the view that the underlying project remained fundamentally the same, albeit at a higher cost. As the increase of Invest NI’s loan facility was within the 10% tolerance it was determined that the change was not material and it did not need to be referred back to DfE / DoF.

However, Invest NI accepts that it did not consider the circumstances in their totality and that DoF should have been consulted about the requirement for re-approval at this point.

In addition, Invest NI acknowledges that the work carried out to assess whether the pre- conditions had been met was not sufficiently thorough and that too much reliance was placed on the due diligence undertaken by the private sector partner.

Furthermore, despite a detailed risk assessment at the casework stage and ongoing monitoring, we accept that the absence of a project specific risk register meant that the risk monitoring and escalation process was not sufficiently robust to respond to the changing risk profile of this project.

Given the issues arising, in November 2020, Invest NI Audit and Risk Committee requested that Internal Audit services undertake a lessons learnt review of the case. As a result of the recommendations made, Invest NI is implementing additional measures for future cases. This includes the establishment of a committee to oversee complex and high risk cases, as well as additional monitoring to provide greater oversight and control. Invest NI has also established a Governance Oversight and Compliance Council (GOCC) to implement best practice and improvements right across the governance framework and the issues identified in the Glenmore case have been included in GOCC’s action plan, with progress monitored by Invest

NI’s Audit & Risk Committee.”

- I will keep this area under consideration and may carry out a further review in future as requested by the Public Accounts Committee in their recent report on Generating Electricity from Renewable Energy.

KJ Donnelly Northern Ireland Audit Office

Comptroller and Auditor General 1 Bradford Court Upper Galwally

4 March 2022 Belfast

BT8 6RB