Foreword from the Comptroller and Auditor General (C&AG) – Dorinnia Carville

This is my fourth quality report as the C&AG of the Northern Ireland Audit Office. This report covers our audit quality arrangements and monitoring activity under International Standard on Quality Management 1 (ISQM 1) in relation to our financial audit and public reporting work for the year ended 31 March 2026.

This is the second year of our Corporate Plan 2024-2029 and delivering high quality public audit remains one of the key corporate priorities for the Office. Over the past year we have maintained a strong organisational focus on embedding quality across all aspects of our work.

The results of our quality control reviews are consistent with the previous year. Whilst the results indicate a generally acceptable standard of audit quality, they have not yet reached the level to which we aspire. We remain committed to embedding further our identified good practice and to strengthening our approach where required.

In 2025-26 we implemented the revised ISA (UK) 600 standard for group audits in our audits of 2024-25 financial statements. The Office currently undertakes 19 group audits, nine of which are complex Departmental Group accounts.

A wide range of actions for continual improvement have been taken including briefing sessions, targeted training and workshops for staff as well as enhancing the guidance available across a number of areas. We are fully committed to supporting our people in their training and continuous professional development.

The audit landscape is becoming increasingly complex as our audited bodies operate in more challenging environments. There are also increasing regulatory and professional standards for auditors which we must continue to respond to. At the same time, we are seeking to make the most of opportunities in innovation and AI whilst continuing to place quality at the centre of our work.

For the second consecutive year, I disclaimed my audit opinion on the financial statements of the Department for the Economy (DfE). This was due to an inability to obtain sufficient, appropriate audit evidence to support the information in the financial statements. Alongside my disclaimer of opinion, I issued a detailed report which outlines my rationale for reaching this conclusion. This disclaimed audit opinion was considered by the Public Accounts Committee (PAC) on 20 November 2025.

During the period, I continued to support the PAC on a number of significant inquiries including adult reoffending, managing the schools’ estate, access to general practice, homelessness in Northern Ireland and road openings by utilities. The Committee’s interest in these matters helps to promote good governance and accountability across the Northern Ireland Civil Service (NICS).

During 2025-26, we delivered an extensive public reporting programme and published reports covering a wide range of topics including partnership working, educational disadvantage, leading and resourcing in the NICS, active travel, major IT projects and waste crime.

Our Good Practice Guides continue to be valued by stakeholders. During 2025-26 we published Raising Concerns: A Good Practice Guide for the Northern Ireland Public Sector. The Guide is aimed at helping public sector organisations understand the value of an open and honest reporting culture.

Our people are at the centre of our work. In recent years, we have recruited to build our capacity and capability to enable us to deliver our financial audit work and an ambitious public reporting programme. The recruitment of a Head of Quality and Innovation during the year further demonstrates our commitment to enhancing the quality across all our work. The Head of Quality and Innovation leads the Data Analytics and Quality Teams. The Quality Team is responsible for developing and providing financial audit guidance to staff, coordinating the quality control review processes and a programme of technical auditing and accounting training for staff.

Our People Engagement Programme progressed at pace during the year with the establishment of a Programme Steering Group and three thematic working groups focused on Development, Engagement & Involvement and Systems & Structures. I am delighted to see the progress which has been made and active involvement of so many staff in the programme, which is starting to deliver outcomes which will benefit the Office across a wide range of areas and maintain and enhance NIAO as a great place to work. I remain very proud of the work of the NIAO and our achievements in the past year. As we move into 2026-27, we will build on the achievements to date, whilst continuing to adapt to new innovations alongside our constant focus on our quality.

Introduction

The NIAO Corporate Plan 2024-2029 sets out the Office’s corporate priorities. One of our three priorities is to deliver high quality public audit to support, enhance and promote high standards in public service administration, accountability arrangements and financial management. We aim to deliver this by:

Providing assurance through timely delivery of our annual financial audit programme in line with International Standards on Quality Management;

Holding the public sector to account through the delivery of high quality, timely and accurate reports; and

Delivering Good Practice Guides as set out in the Public Reporting Programme.

1.International Standard on Quality Management (ISQM) 1 requires firms to design, implement and operate a system of quality management (SOQM) to manage quality at both the engagement and organisational level.

The quality of work of the Office is fundamental. Quality management is therefore embedded across all aspects of our operations including the Office’s policies on recruitment, training and continuing professional development, quality control reviews, operational guidance specific to the performance of our work and a code of conduct.

Our quality arrangements are set out in a well-established Quality Manual. Our system of quality management is designed to ensure that the Office’s work complies with professional and other relevant standards. As the audit landscape continues to evolve, we update our Quality Manual, along with associated policies and procedures to address emerging challenges and changes in professional standards.

An annual Evaluation of Quality Management is undertaken by the Quality team and presented to the Senior Leadership Team (SLT) each December. The most recent evaluation, completed in December 2025, concluded that the NIAO system of quality management provides assurance that the quality objectives are being achieved.

This report covers our audit quality arrangements and monitoring activity under ISQM 1 for the year ended 31 March 2026. It outlines how we are delivering our corporate priority of high-quality public audit and how we provide our stakeholders with confidence in the NIAO’s statutory role in providing oversight and assurance on public sector spending.

Dorinnia Carville – Comptroller and Auditor General

Ultimate responsibility and accountability for the NIAO's system of quality management rests with the Comptroller and Auditor General.

Rodney Allen – Chief Operating Officer

Quality Management Director assigned operational responsibility for the system of quality management, including compliance with independence requirements and the monitoring and remediation process.

Executive Summary - Key highlights 2025-26

This section of the report summarises the key highlights for 2025-26.

Our system of quality management is underpinned by a suite of policies and procedures including:

NIAO Quality Manual

NIAO Code of Conduct

NIAO Financial Audit Methodology

NIAO Public Reporting Methodology

Policy Circulars

Our People

The Office recruited fifteen staff consisting of one Director, one Head of Quality & Innovation, one Head of Corporate Services, one Head of Corporate Affairs, one Data Scientist, four Auditors, four Trainee Accountants and two Higher Level Apprentices.

We are a registered training organisation and support the Graduate Trainees in completing their qualification with Chartered Accountants Ireland. In addition, we provide professional training for our Apprentices undertaking the Institute of Accounting Technicians Ireland qualifications.

During 2025-26 three staff left the Office to pursue other opportunities and two members of staff retired.

Methodology

Our financial audit methodology is well embedded, and teams now have a number of years’ experience in its application. 2025-26 was the first year of application for the revised ISA 600 for the audits of 2024-25 financial statements. To comply with the revised standard, teams adopted a new approach to auditing group accounts.

Work continued on the development of a new Financial Audit Manual in collaboration with Audit Wales. The manual will supplement current guidance and support teams in applying NIAO audit methodology.

Our Public Reporting Portal was developed and went live to all staff. The portal sets out the Office’s public reporting methodology and provides a repository of template papers for each stage of the public reporting process.

Training and continuous professional development

Training was delivered to staff on a range of topics including:

Data Analytics –Adapt training (our internally developed data analytics tool which supports staff in completing risk assessments and selecting samples for financial audit);

Local Government update – General and specific sessions;

ISA315 – Strengthening the Approach to IT Audit Risk

Financial Accounting Update;

Auditing Standards Update;

Regularity training;

Supply training;

CIPFA certificate in Performance Audit Fundamentals;

Data visualisation; and

Public reporting processes and guidance

Financial Audit

During 2025-26,147 accounts were certified - 107 central government accounts,15 local government accounts and 25 prior year accounts. In total, 22 audits with significant matters of judgement were referred to the Technical Director. The C&AG’s opinions on 11 accounts were qualified (some accounts received more than one qualification) and a further 5 other matters were highlighted in the C&AG’s audit certificate. The C&AG also disclaimed her opinion on one account.

Three financial audits were subject to an internal Engagement Quality Review by three independent directors who were assigned as engagement quality reviewers. In each case, the engagement quality reviewer upheld the conclusions reached by the engagement team.

Quality Review – Financial Audit

Three financial audits were subject to external quality control review (QCR) by the Institute of Chartered Accountants in England and Wales (ICAEW). Two of the audit files reviewed were rated as ‘generally acceptable’ and one file was rated as ‘improvement required’. In addition, ICAEW identified a number of areas of good practice in the audit files.

While the results demonstrate a generally acceptable standard of audit quality, they are not at the standard we aspire to and the Office has identified a number of areas for improvement. In response to the issues raised by ICAEW, the Quality Team has undertaken a number of actions including:

Facilitating root cause analysis with the relevant engagement teams;

Developing detailed action plans for implementation by the engagement teams;

Issuing an Audit Policy Circular to all staff outlining the findings from the Quality Control Reviews;

Holding a briefing session for all staff to discuss the findings; and

Developing and issuing updated group audit guidance.

The Quality Team will monitor the implementation of action plans and progress on actions to improve audit quality will be reported to SLT, the Audit & Risk Assurance Committee and the Advisory Board.

A number of further actions are planned which include thematic hot file reviews, follow up reviews and the establishment of a Quality Committee.

The Office currently contracts out 21% of its financial audit work to six private firms. A sample of four contracted out engagements were also subject to quality control review by NIAO managers who were independent of the audit engagement. The audits reviewed were graded as follows:

One audit was graded as ‘1 – Good’;

Two audits were graded as '2 – Generally acceptable’; and

One file was graded as ‘4 – Significant improvement required’.

The grading of ‘4 – Significant improvement required’ received this rating on the basis of a number of weaknesses identified in the audit work performed. A number of actions for future improvement have been agreed with the contractor and further details are provided in Part Three of this report.

The above actions aim to deliver continuous improvement in the quality of our financial audit work and also ensure that our people continue to learn and develop. In 2026-27, there will be a continued focus on the importance of quality in all our work, consistent with our corporate priority.

Public Reporting

During 2025-26 we published:

11 Public Reports

11 Local Government Improvement Reports

1 Good Practice Guide

1 Local Government Report

The 11 Public Reports published in 2025-26 were:

PSNI Fleet Management

Continuous Improvement arrangements in Policing

Waste Crime in Northern Ireland

Major IT projects in Northern Ireland

Active Travel in Northern Ireland

Performance of Restricted Procedures by Health Trusts

Northern Ireland Energy Strategy

Leading and Resourcing the Northern Ireland Civil Service

Raising Concerns in the Northern Ireland Public Sector

Partnership Working: Departments and Arm’s Length Bodies

Evaluation of Programmes Addressing Educational Disadvantage

Major IT Projects in Northern Ireland and the Northern Ireland Energy Strategy were selected by the Public Accounts Committee for inquiries.

Public Reporting Quality

Four public reports published in 2025-26 were reviewed by other audit agencies as part of the peer review process. Reviewers found our reports to be balanced, authoritative and persuasive and the judgments included in reports are supported by robust evidence and analysis. The reviews also identified learning points that were shared with staff working on public reporting.

Survey of audited bodies

We undertook a survey of audited bodies during the year and feedback continued to be very positive, with overall impressions being:

98% indicating that NIAO audit staff provided a high quality and professional service;

96% consider that the NIAO’s work leads to improvement in the provision of public services;

100% considered NIAO good practice guides as a useful resource.

We also undertook a survey of Members of the Northern Ireland Assembly’s Public Accounts Committee during the year and feedback was very positive. Members were satisfied with the topicality, structure and clarity of our public reports and how they supported an effective Public Accounts Committee Inquiry. Members also expressed satisfaction with the NIAO’s engagement with the Committee and our role in supporting its work throughout the current mandate.

Part One: Policies and procedures

The quality management policies, procedures and practices of the NIAO are currently documented in the NIAO Quality Manual, supplemented by, and cross referenced to, a variety of documentation and procedures including:

NIAO Code of Conduct

Financial Audit Methodology

Public Reporting Guidance

Recruitment, training and promotion policies

Staff performance management procedures

Quality control review processes

Audit Policy circulars

Our quality arrangements are set out in a well-established Quality Manual. Our system of quality management is designed to ensure that the Office’s work complies with professional and other standards. All staff can access the Quality Manual through the NIAO intranet and any changes to the Manual are communicated to staff through Audit Policy Circulars and announcements on the intranet. As the audit landscape continues to evolve, we update the Quality Manual and associated policies and procedures to address emerging challenges and changes in professional standards.

A detailed annual Evaluation of Quality Management is undertaken by the Quality team and presented to the Senior Leadership Team (SLT) each December. The most recent evaluation, completed in December 2025, concluded that the NIAO system of quality management provides the Office with assurance that the quality objectives are being achieved.

Work is ongoing on the development of a new Financial Audit Manual. This will set out NIAO financial audit methodology and supplement existing guidance, supporting engagement teams in delivering high quality financial audit work. We are working in collaboration with Audit Wales on this project and it is expected be completed later this year.

During 2025-26, a number of audit policy circulars were issued to staff covering areas such as sampling, QCR arrangements for financial audits and Whole of Government Accounts (WGA) audit instructions.

Throughout the year, the Quality Team made further revisions to tools and templates in response to user feedback. The Team also circulated guidance to staff to ensure they were kept up to date with changes in auditing standards (ISAs) and financial reporting requirements.

The Public Reporting Portal was developed during 2025-26. The Portal sets out the NIAO’s public reporting methodology and the procedures to be followed at each stage of the public reporting process including those relating to quality assurance. The Portal also provides a repository of key working papers to be used and guidance documents to assist staff in delivering high quality public reporting work.

Governance & Leadership

The NIAO Advisory Board supports the C&AG in her role as Accounting Officer, by reviewing the comprehensiveness and reliability of assurances on governance, risk management, the control environment and the integrity of financial statements and the annual report. The Board met four times during 2025-26.

To support this role, the Board has an Audit and Risk Assurance Committee (ARAC) to review the assurances provided on systems of internal control, risk management and corporate governance. ARAC comprises three non‐executive Board members of NIAO, excluding the NIAO Board Chairperson, and is independent of all NIAO operational activities. ARAC is chaired by an accountant with previous audit experience. The Committee met four times during 2025-26.

Marie Mallon OBE is the Chairperson of the Advisory Board. Three non-executive members, Claire McAleenan, Jill Laughlin and Dean Sullivan, took up post in April 2025.

ARAC was kept informed about quality related matters throughout the year. The committee also received updates on the results of the quality control reviews (QCR) and remedial actions being taken by the Office to improve audit quality.

The NIAO Senior Leadership Team (SLT) comprises the C&AG, the Chief Operating Officer and six Directors. SLT are appropriately skilled and have expertise in delivering financial audits and public reporting work. SLT receive regular updates from the Head of Quality and Innovation, the Head of Corporate Services and the Head of People and Organisational Development. They also receive regular briefings on the actions being taken to improve the quality of both financial audit and public reporting work.

The NIAO Corporate Management Team (CMT) comprises Audit Managers, Head of People and Organisational Development, the Head of Corporate Services and the Head of Quality and Innovation. CMT is responsible for operational leadership and contributing to the strategic leadership of NIAO. CMT has quality as a standing agenda item and receives regular updates from the Head of Quality and Innovation on work in this area. It also provides an opportunity for managers to share and discuss issues identified during audits, contract management, workforce and resourcing planning.

SLT has provided approval for the establishment of a Quality Committee to oversee audit quality. It is envisaged that the Quality Committee could become a sub-committee of the Board. Work will commence in 2026-27 to develop detailed proposals including membership and terms of reference.

Ethics

The Office has established clear procedures to promote and uphold high standards of ethical behaviour across all staff. To enhance transparency, we publish a register of interests of the SLT and our Advisory Board members on our website.

Further details on compliance with ethical standards is included in Part Two of this report.

Part Two: People & Engagement Resources

Our people are critical to the success of NIAO. Their attraction, development and retention are pivotal to delivering our strategic priorities. One of our corporate priorities is to invest in our people and resources in order to be a high performing, people-focused organisation.

The well-embedded NIAO People Strategy is central to our strategic and organisational planning and supports the achievement of our overall strategic priorities, delivered through a comprehensive People Plan.

Recruitment, retention and development of staff continue to be a high focus for NIAO as we build and maintain capacity and capability within the organisation. It is essential that these priorities are supported by strong leadership.

As an Investors in People (IIP) accredited organisation we are committed to the continuous investment in our people’s development, talent and motivation.

Following the most recent biennial staff engagement survey, the NIAO People Engagement Programme was established in 2025-26. A Programme Steering Group has been formed to provide strategic oversight and direction. Membership comprises the Chief Operating Officer, a Trade Union representative, an External Strategic Advisor, the Head of People and Organisational Development, a SLT representative and a representative from CMT.

Three Development Working Group have also been established to lead delivery across three key themes:

Development;

Systems & Structures; and

Engagement & Involvement.

Each working group is led by a Director, with members drawn from various grades and roles in the Office. Each group is responsible for identifying and delivering projects that address themes identified from the staff survey.

During the year, significant progress has been made to deliver the identified projects. In the months ahead, work will continue on the projects with a number nearing completion. A programme of engagement will take place across the organisation to inform and update staff of ongoing developments. The People Engagement Programme demonstrates our commitment to working in partnership with our staff to shape further improvements and maintain and enhance NIAO as a great place to work.

Compliance with Ethical Standards and Independence

The Chief Operating Officer, Rodney Allen, as Quality Management Director is responsible for policies and procedures in respect of integrity, objectivity, independence and compliance with the Financial Reporting Council’s Ethical Standard. The Quality Management Director also acts as the Office’s Ethics Partner.

The Office has established quality objectives to ensure that it fulfils its responsibilities in accordance with relevant ethical requirements. The C&AG’s independence is enshrined in statute. This underlines the need for her and her staff to be objective and impartial in all their work, including delivering accurate, fair and balanced reporting.

The NIAO Code of Conduct (the Code) outlines the ethical requirements to which staff must adhere. The requirements encompass the five fundamental principles of professional ethics:

Integrity

Objectivity

Professional Competence and Due Care

Confidentiality

Professional behaviour

The Code requires staff to be independent of audited bodies or other interested groups. They must have an unbiased attitude to the issues and topics under review. The Code requires staff to complete an annual return setting out any potential conflicts of interest, including personal or domestic relationships with employees of bodies they audit. All completed declarations are recorded and held centrally in the eHR system. They are subject to review by the Ethics Partner.

The Code also requires staff to notify their line director immediately of any changes in circumstances affecting their previous declarations. In addition, all staff complete a declaration of independence for each audit engagement they work on.

The FRC’s Ethical Standard (2024) requires the engagement team to consider threats to independence, objectivity and integrity in respect of all covered persons. Covered persons are defined as "a person in a position to influence the conduct or outcome of the engagement". Each year, the Quality Management Director identifies all covered persons and reviews their Code of Conduct return. Where the Quality Management Director considers these individuals have potential conflicts with audit engagements, he will notify the engagement directors and engagement managers affected to ensure that appropriate safeguards are put in place to mitigate risk. To provide evidence on audit files, confirmation is provided to all staff when this exercise is complete. In 2025-26, staff were notified that the exercise had been completed on 11 June 2025.

Staff rotation

To safeguard against conflicts of interest arising from over familiarity, the Office has a policy of rotating staff. Engagement directors and engagement managers may continue with a specific client or engagement to the fifth year of association (inclusive) unless any identified threats to their or the C&AG’s objectivity or perceived loss of independence are identified that cannot be properly mitigated.

In years six and seven, there is a presumption that engagement directors and engagement managers will be rotated due to length of association alone unless there are overriding operational reasons for them to remain in place. No engagement director or engagement manager will act as part of an engagement team for a period of more than seven years in any twelve-year period.

Once rotated, relevant individuals should have no further involvement in work relating to the client for a further five-year period. Where an engagement quality reviewer involved in a financial audit subsequently becomes the audit engagement director, the combined period of service in these positions shall not exceed seven years. In addition, a cooling off period of two years is required before the engagement director can assume the role of engagement quality reviewer.

Where the role of engagement director is delegated, the same rotation requirements apply to the individual undertaking that role. The role of engagement director may be delegated were the audit engagement meets certain criteria as set out in the NIAO Quality Manual. The segmentation of each portfolio of audits ensures an alignment in roles and responsibilities commensurate with the skills of the engagement team and the audit risk of the audited entity. All other staff will be rotated regularly to ensure that they gain experience across a range of audit clients. No member of staff should work on a particular engagement for a period of more than seven years within any twelve-year period.

Any firms contracted to undertake financial audit work on behalf of NIAO are also required rotate staff in line with this policy.

Rotation requirements have been complied with in 2025-26.

Hospitality

A register of all hospitality offered to NIAO staff is maintained. For transparency, disclosures of hospitality and gifts accepted, declined and provided by each NIAO Non-Executive Member and member of the Senior Leadership Team are published on our website annually.

Recruitment

We continue to recruit and promote high quality candidates to meet our current and future needs. Recruitment is competency and values based and is conducted in compliance with equal opportunities requirements. In 2025-26 we focussed on attracting individuals with a range of different skills and experiences to enhance the diversity of our workforce and keep pace with professional developments. Details on the numbers of staff who were recruited and who left the Office during the year are included in the Executive Summary of this report.

The Office recruits Higher Level Apprentices (HLAs) in Accounting and Trainee Accountants annually, with a view to developing our own qualified accountants. There is a structured training programme which supports trainees throughout their time with the Office. This is complemented by mentoring and on-the-job training within audit teams.

During the year, we partnered with Queen’s University Belfast as part of their Master’s in Accounting programme and hosted two paid placement students for 12 weeks beginning in January 2026. The placement provided the students the opportunity to gain an insight into the role of the Northern Ireland Audit Office in scrutinising public sector finances. Placement students were provided with a meaningful learning and development experience to broaden their accounting and auditing knowledge.

Resourcing

We have established an Operational Resourcing Team (ORT), facilitated by a Director with membership drawn from staff across a range of grades. ORT leads resource planning for financial audit and public reporting work to ensure that each engagement is adequately resourced with staff who have the appropriate skills and experience. The work of the ORT team is supported by an ORT model developed by the Office’s Data Analytics Team.

Competence and capabilities of staff

We have established policies and procedures designed to ensure the Office has sufficient personnel with the skills, competence and commitment to ethical principles to perform its engagements in accordance with professional standards, and regulatory and legal requirements.

These policies and procedures are set out in the Office’s personnel, management information and Audit Policy Circulars supported by the Northern Ireland Civil Service (NICS) Staff handbook.

To ensure compliance with ethical and professional requirements, the competence of financial audit teams is assessed and documented at the outset of each audit engagement as part of our risk management procedures.

Performance management

The current performance management system provides a framework for agreeing work priorities, setting expectations, reviewing performance, and supporting professional development. It aims to promote a culture of continuous dialogue on both behaviours and performance, based on clear expectations.

The system is based on a partnership between the individual and the organisation and is designed to support staff in developing their skills and contributing effectively to achieving corporate priorities.

Performance reporting is recorded using the Office’s eHR system, which assists monitoring of compliance with the performance management policy.

Learning and Development

The Office recognises the importance of training and development and supports all staff in maintaining and enhancing the skills required for their roles. The Learning, Development and Talent Management Strategy directly aligns with the Corporate Plan for 2024-2029 and is a fundamental part of the strategic pillars within our People Strategy. This strategy supports the achievement of our strategic priorities and reflects our values as an organisation.

The Office develops the capabilities and competence of its staff through a combination of structured and unstructured training, work experience and coaching, influenced by a 70-20-10 Model for Learning.

During the year, a Learning and Development Opportunities booklet was issued to all staff, illustrating the wide range of activities on offer to support their continued development in line with the seven key areas identified in the Learning, Development and Talent Management Strategy.

The performance management framework includes consideration of training undertaken and identification of ongoing developmental needs.

The Office is a registered training organisation and supports trainees in completing their qualification with Chartered Accountants Ireland. In addition, we provide professional training for our apprentices undertaking the Institute of Accounting Technicians Ireland qualifications.

To support the delivery of our priorities, it is essential that our staff have the necessary skills and experience. Approximately 64 per cent of staff hold professional accountancy qualifications. We also have a number of staff with specialist skills across a range of areas including IT audit, data analytics skills and professional corporate services.

In recent years we have built capacity internally and all IT audit work is now delivered in-house. IT audit staff have been supported to undertake their ISACA Certified Information Systems Auditor (CISA) qualification. IT audit training is also offered to all staff to ensure we continue to develop the skills of engagement teams in this area and to enable us to respond as the IT environments of our audited bodies become more complex.

The Quality Team develops an annual technical training programme, including a number of mandatory courses to support audit quality and ensure staff remain up to date with the auditing and accounting standards. Attendance is monitored and followed up where necessary.

Staff can apply for a variety of training courses to meet Continuing Professional Development (CPD) and the competency requirements of their roles. Booking takes place via the eHR system which facilitates accurate recording of training and development. In addition to booking training, eHR allows staff to centrally record their CPD activities, including those undertaken outside core work.

Qualified staff have a responsibility to ensure that they are attending courses and updating their knowledge in order to comply with the requirements of their respective professional institutes. Staff are supported by the office to maintain professional accreditations with respective Institutes.

The training needs for staff are identified from a variety of sources including:

strategic workforce planning;

Corporate/Business plans;

changes in working practices e.g. new technology, legislation and systems;

technical requirements;

professional requirements;

statutory and mandatory requirements; and

performance management, including personal development plans.

During 2025-26 a range of technical training was delivered covering a range of topics including:

Data Analytics –Adapt training (our internally developed data analytics tool which supports staff in completing risk assessments and selecting samples for financial audit);

Local Government update – General and specific sessions;

ISA315 – Strengthening the Approach to IT Audit Risk

Financial Accounting Update;

Auditing Standards Update;

Regularity training;

Supply training;

CIPFA certificate in Performance Audit Fundamentals;

Data visualisation; and

Public reporting processes and guidance

In addition to formal training provided, the Quality Team have issued guidance on several technical matters to financial audit teams covering topics, such as group audit, asset valuations, audit sampling, auditing estimates, external confirmations, payroll substantive analytic procedures, auditing short periods of account and sustainability reporting.

All of our audit staff have access to Croner-I, an online reference service which allows users to access auditing and accounting standards. It also provides online training courses and practical advice on the application of accounting and auditing standards.

All new staff are assigned a ‘buddy’ when they join. New buddy guidance is being developed to strengthen this role. On-boarding procedures for new staff includes training on NIAO audit methodology. The NIAO welcome booklet was updated during 2025-26 and will be rolled out to new starts joining NIAO during 2026-27.

Trainees receive in-house introductory accounting and audit training prior to commencing their studies. During 2025-26, a new in-house training programme for trainees was developed which covers the knowledge and skills required as they progress through their training contracts. It is anticipated that the programme will launch in 2026-27.

We also continued to provide a range of technical training for our public reporting staff including a public reporting day, which comprised a review of future developments and public reporting guidance. A session was also held to guide our public reporting staff on meeting the needs of the Public Accounts Committee.

We identified the CIPFA Certificate in Performance Audit Fundamentals as being relevant to our public reporting work. Seven staff have successfully completed the certificate, and we are planning to facilitate more staff completing the course in 2026-27. Further training on data visualisation has taken place for our champions’ network.

The Office has also submitted an application to join EURORAI, the European Organisation of Regional External Public Finance Audit Institutions. EURORAI is a cooperation project aims to foster and promote cooperation and exchanges of knowledge and experience amongst public audit institutions across Europe.

Staff Wellbeing

The Wellbeing Strategy, launched in October 2023, aims to ensure that individual and organisational wellbeing is embedded in everything we do. The annual action plan has successfully been delivered. The Wellbeing Committee continues to support the delivery of the Wellbeing Strategy and action plan through our wellbeing champions.

The Committee plans and delivers a programme of events focusing on our pillars of physical, mental, social and financial wellbeing. A wide and varied programme of activities is provided.

Our programme is supplemented by access for all staff to an on-site gym and a wide range of social events arranged by our active Sports and Social Committee who work in partnership with the Wellbeing Committee.

All staff have access to a Wellbeing Hub via the intranet site or app at any time. The Hub promotes wellbeing activities and provides access to advice, information, tools and resources, and signposting to partner organisations. The Hub has been customised to provide staff access to our policies and procedures, and NIAO news and features.

In addition, staff have access to an Employee Assistance Programme which provides direct access to health and wellbeing support including confidential counselling services and individual health checks to support staff wellbeing.

Equity, Diversity & Inclusion

During 2025-26, our Equity, Diversity & Inclusion (EDI) Committee worked towards obtaining the Diversity Mark accreditation. Accreditation was awarded in February 2026. The Committee also developed NIAO’s first EDI Strategy which was officially launched in April 2026. An Action Plan is currently being developed by the Committee to support delivery of the Strategy.

The committee has appointed EDI Champions for Disability; Inclusion and Accessibility; LGBTQIA+; Gender equality; neurodiversity; race and ethnic minorities; and family/carers.

Throughout the year, the committee delivered a number of activities and initiatives including the provision of period products and menopause packs, internal communications to support and promote EDI related events and delivered a well-attended six-week introductory course in Sign Language.

Use of technology

We currently use ‘Pentana’ as our audit software package to document our financial audit work. We regularly engage with other audit agencies to monitor developments in audit software. A fundamental review of audit software applications is planned for 2026-27.

During 2025-26, our data analytics team further developed the Adapt app extending its use across a wider range of financial audits. The Office continues to make greater use of data analytics to improve quality, insights and efficiency in financial audit. The data analytics team has provided bespoke analysis of high-volume datasets to some financial audit teams. This has enabled those teams to identify high-risk or unusual patterns which warrant further investigation.

We recognise the opportunities presented by advancements in AI. In March 2026, terms of reference were introduced for all staff setting out the governance and acceptable use of AI in NIAO. This includes principles, responsibilities and oversight arrangements required to ensure compliance with cyber security, information governance and professional standards.

Co-pilot is the only AI platform which is approved for use by NIAO staff. Currently all staff have access to Copilot Chat. An AI working group has been established to explore the opportunities in this area including a trial of Microsoft 365 Copilot across financial audit, public reporting and corporate services.

The Office recognises the limitations of AI including the risk of generating inaccurate outputs and the ability to hallucinate. AI generated content will not be used as audit evidence and must be subjected to appropriate review and verification by audit staff. The findings from the Copilot trial and new guidance issued by the Financial Reporting Council will inform any further guidance to be developed for staff in seeking to use AI innovatively and efficiently in our work.

Use of external resources

We contract out, in financial terms, around 21 per cent of our financial audit work to private sector firms. This partnership supports the efficient delivery of financial audits and also enables us to benchmark our work against the private sector.

In all contracted-out audit arrangements, the C&AG retains overall responsibility for the audit of the financial statements and signs the audit certificate.

Details of how we monitor the quality of our contracted-out financial audits are set out in Part Three of this report.

We continue to monitor the extent to which we work in partnership with private sector firms.

Part Three: Engagement performance

Overall responsibility for engagement performance and quality rests with the engagement director assigned to each audit.

During 2025-26 we certified 107 central government accounts and 15 local government accounts. In the period we also certified 25 prior year accounts.

Acceptance and continuance procedures

As the C&AG is appointed as auditor under statute, acceptance procedures are not always applicable. In accordance with ISQM 1, we have procedures in place to ensure that we only undertake or continue relationships and engagements where we have:

considered the nature and circumstances of the engagement including the integrity and ethical values of the audited body;

assessed the Office’s ability to perform the engagement in accordance with professional standards and applicable legal and regulatory requirements; and

ensured the financial and operational priorities of the Office do not lead to inappropriate judgments about whether to accept or continue a client relationship or specific engagement.

The majority of audits undertaken by us are by statutory appointment and in these circumstances, we cannot withdraw or decline the appointment. However, Practice Note 10 Audit of Financial Statements and Regularity of Public Sector Bodies in the UK (Revised 2024) (PN10), identifies alternative courses of action in such circumstances. For example, we can report to the NI Assembly on matters which might otherwise have caused us to withdraw from the engagement.

Acceptance and continuance procedures are outlined in the NIAO Quality Manual and the electronic audit template for all audits regardless of whether these are statutory appointments. All new client and engagement requests must be submitted to the C&AG for approval.

There were four new engagements assigned under statute during 2025-26. These are the Irish Language Commissioner, The Office of the Commissioner for Ulster Scots and the Ulster British Tradition, the Office of Identity and Cultural Expression and the Legal Services Oversight Commissioner for Northern Ireland.

Technical and specialist advice

We have a designated Technical Director whose responsibilities include:

- Establishing policies and procedures to provide reasonable assurance that engagements are performed in accordance with professional standards, and regulaory and legal requirements.

- Providing informed advice on technical matters and reviewing certifciate modifications and C&AG reports.

- Liaising with other public sector audit agencies on technical matters of common interest.

The Technical Director, supported by the Head of Quality and Innovation and their team, provides advice to staff on complex or judgemental accounting and auditing issues. All audit qualifications or proposed audit qualifications must be referred to the Technical Director. Where a conflict arises (e.g. the Technical Director is involved in an audit requiring technical review), the matter is assigned to an independent director or handled by the Quality Management Director.

Differences of opinion within the engagement team or between the engagement team and an engagement quality reviewer should be referred to the Technical Director for resolution.

During 2025-26, a wide range of technical guidance and advice was provided to audit teams on key audit or accounting issues. This covered topics such as group audits; using the work of experts; accounting estimates; ethical requirements; sustainability; sampling; materiality; asset valuation; and leases.

In total, 22 audits with significant matters of judgement were referred to the technical director during 2025-26. Arising from these, the C&AG’s opinions on eleven accounts were qualified (some accounts received more than one qualification), the C&AG disclaimed her opinion on one account. On a further five accounts other matters were highlighted in her audit certificates.

Review of engagement performance

During the period, the vast majority of audits performed were subject to a two-stage review process:

First Stage Review

- a detailed review of all working papers and audit procedures by another team member who is senior to the preparer

- detailed review is the responsibility of the engagement manager but the task may be delegated to another team member

- this ensures that the audit team is complying with ISA (UK) 220 - Quality Management for an Audit of Financial Statements

Second Stage Review

an overall review undertaken by the engagement director to confirm that sufficient and appropriate audit evidence has been obtained to satisfy the objectives of the engagegment procedures and to support the recommended audit opinion

this review will consider the major issues of judgement and other key areas of the audit process

Our Quality Manual sets out instances when portfolio directors may delegate ‘engagement director’ responsibility. Audits that are assessed as being lower risk and lower complexity may have only one stage of review and are delegated to another member of the audit team who will act as the engagement director. The rationale for adopting this approach will be clearly documented and approved by the portfolio director.

Engagement Quality Review (EQR)

We have established policies set out in the Quality Manual to identify audits which require an engagement quality review (EQR). An EQR provides an objective evaluation of significant judgements made by the engagement team and the conclusions reached. This review is undertaken by an engagement quality reviewer who is a director and is independent of the audit engagement.

As part of the financial audit planning process, the engagement director is responsible for determining whether an EQR is required, taking account of the following factors:

whether the entity is a Public Interest Entity (PIE) or whether any relevant laws or regulations require an engagement quality review; or

the nature of the engagement, including the extent to which the entity’s financial statements are of high Assembly or public interest; or

the identification of unusually complex circumstances or technical risks and/ or judgements in an engagement or class of engagements; or

whether it is likely that there may be a significant modification to the audit opinion; and/or

if an engagement quality review is an appropriate response to address one or more quality risk(s); and/or

where senior engagement staff are new to their role.

An engagement quality reviewer is assigned for all high-risk audits of first year directors to ensure audit quality.

The Technical Director determines which individual will perform the role of engagement quality reviewer taking into account an individual’s independence from the body being audited, their specific skill set and their experience at director level.

The engagement quality reviewer must not be a member of the engagement team, and an engagement director may not act as engagement quality reviewer until a period of at least two years has passed after previously serving as engagement director.

The engagement quality reviewer will raise any concerns regarding the appropriateness of significant judgments or conclusions reached with the engagement director. If those concerns are not resolved to the engagement quality reviewer’s satisfaction, the engagement quality reviewer notifies the Technical Director or the Quality Management Director that the engagement quality review cannot be completed.

During 2025-26, three financial audits were subject to EQR. In each case the reviewer upheld the judgements and conclusions made by the engagement team.

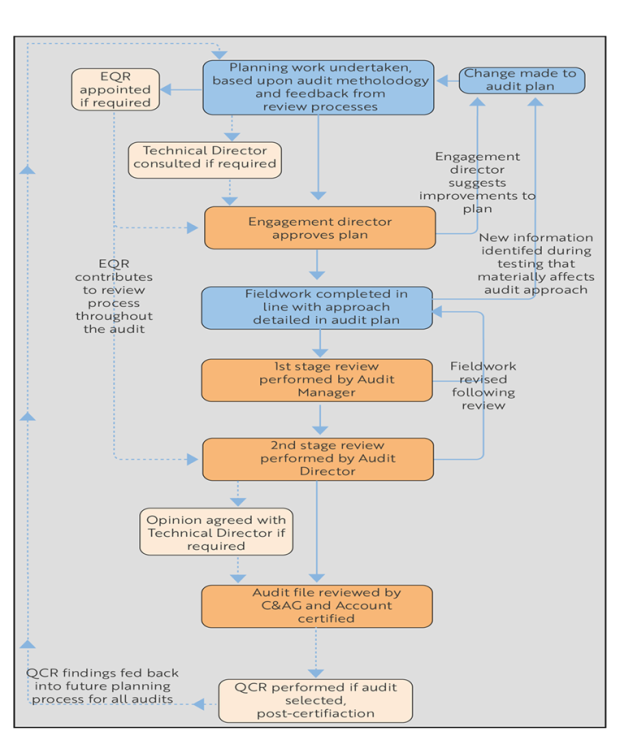

The diagram below outlines the review processes during a financial audit.

This diagram presents a flowchart of the audit process, showing the sequence of activities and quality review steps, with feedback loops throughout.

The process begins with planning work undertaken based on audit methodology and feedback from review processes. At this stage, an Engagement Quality Reviewer (EQR) and a Technical Director may be consulted if required. The EQR contributes to the review process throughout the audit.

The Engagement Director approves the audit plan. During the process, the Engagement Director may suggest improvements, or new information identified during testing may lead to changes to the audit plan.

Fieldwork is then completed in line with the audit plan. If review findings require it, fieldwork may be revised.

The audit then undergoes two formal review stages: a first-stage review performed by an Audit Manager, followed by a second-stage review performed by an Audit Director.

Where necessary, the audit opinion is agreed with the Technical Director. The audit file is then reviewed by the Comptroller and Auditor General (C&AG), and the account is certified.

After certification, a Quality Control Review (QCR) may be carried out if the audit is selected. Findings from QCR are fed back into the planning process for future audits, ensuring continuous improvement.

The diagram includes multiple feedback loops indicating that insights from reviews, testing, and quality control can influence earlier stages, particularly planning and fieldwork.

Quality control reviews

In-house financial audits

As part of quality monitoring procedures, we undertake an annual programme of quality control reviews. This is coordinated by the Head of Quality & Innovation and overseen by the Technical Director. It is a key mechanism for promoting audit quality and continuous improvement.

The objective of the reviews is to consider whether each audit was properly planned and conducted in accordance with our methodology and professional standards, and whether the audit documentation supports the opinion provided.

The Institute of Chartered Accountants in England and Wales (ICAEW) was appointed in October 2024 to provide an independent quality control review service. In line with good practice, this ensures that the monitoring arrangements are independent.

ICAEW select the audit engagements to be reviewed, in accordance with the approach set out in the Quality Manual:

engagement directors with ten or more financial audit engagements are reviewed every two years. Otherwise, engagement directors will be reviewed every three years;

one delegated audit engagement is reviewed every three years; and

where possible, one high risk audit is reviewed each year.

Where a quality control review identifies significant improvements are required, that engagement director’s portfolio of engagements will be included in the following year’s selection, and an additional review will be undertaken.

The 2025 sample period covered all in-house financial audit engagements certified between October 2024 and September 2025, and the review process commenced in November 2025.

ICAEW assessed two files as ‘generally acceptable’ and one file as ‘improvement required’, they also noted areas of good practice in the files reviewed.

The results are not at the standard we aspire to and improvements are required. The key areas identified for improvement were group audits and using the work of management’s expert.

In response to the findings, a range of remedial actions have been put in place, including:

Facilitating root cause analysis with the relevant engagement teams to identify underlying issues;

Developing detailed action plans to ensure lessons learnt are applied in future audits by the engagement teams;

Issuing an Audit Policy Circular to all staff outlining the findings from the Quality Control Reviews;

Holding a briefing session for all staff to discuss the findings;

Delivering training covering key themes including group audit and management’s experts; and

Developing and issuing updated group audit guidance including revised templates.

The Quality Team will monitor the implementation of the action plans. Progress on actions to improve audit quality will be reported to SLT, the Advisory Board and the Audit & Risk Assurance Committee.

Further actions planned include:

thematic hot file reviews of planning for a sample of audit engagements focusing on group audit, management’s experts and regularity;

a follow up review will be performed of the audit rated as ‘Improvement required’ to ensure that lessons learnt have been implemented for the 2025-26 audit; and

the establishment of a Quality Committee which could become a sub-committee of the Board.

These actions are designed to bring about continuous improvement in audit quality and support the ongoing development of our staff. During 2026-27, there will be a continued focus on quality in all our work, in line with our corporate priorities.

Review of contracted out audits

NIAO contracts private sector audit firms to deliver a proportion of its audit engagements. While contractor firms provide shadow audit certificates, the C&AG retains responsibility for certification and reporting.

In 2025-26 we assessed contractor performance through:

regular monitoring of Key Performance Indicators (KPI) and holding quarterly performance review meetings with contractors;

a programme of pre-certification file reviews, based on experience, risk and prior performance;

undertaking quality control reviews of a sample of contracted out audits. This is normally undertaken by engagement directors and managers; and

requiring contractors to undertake cold reviews of the work they are contracted to do (one audit per contract).

Overall results of KPI monitoring were generally satisfactory although significant issues were identified in relation to one contractor.

Four audits were selected for quality control review in accordance with the criteria set out in the Quality Manual. The files were graded as follows:

One audit was graded as ‘1 – Good’;

Two audits were graded as ‘2 – Generally acceptable’; and

One audit was graded as ‘4 – Significant improvement required’.

The audit graded as ‘4 - Significant improvement required’ reflected weaknesses across a number of areas. The contractor has accepted the findings and committed to implementing remedial actions.

As a result of the issues identified, the contractor will be subject to enhanced supervision and review by us in accordance with our contract management procedures. In addition, hawse have updated our audit policy circular in relation contracted out audit engagements in May 2026 and revisions to the Quality Manual will be completed by mid 2026-27.

The findings from the quality control reviews of contracted-out audit engagements have been communicated to staff through an Audit Policy Circular and have been reported to SLT, the Advisory Board and ARAC.

Public reporting Quality Assurance arrangements

Public reporting processes are subject to a range of formal internal quality assurance checks in order to maintain and improve the quality of published reports.

The Office’s current mechanism for external quality review of public reports is through participation in a peer review process involving UK and Ireland public audit agencies. Under this process a sample of public reports is nominated for review on a reciprocal basis by participating audit bodies.

Reports are assessed against agreed criteria and feedback provided to engagement teams to support continuous improvement and the sharing of good practice.

During 2025-26, the Office assumed responsibility for the administration of the peer review process. The Quality Management Director approved four NIAO reports for external peer review. Reviewers found our reports to be balanced, authoritative and persuasive and the judgments included in reports are supported by robust evidence and analysis. The reviews also identified learning points that were shared with staff working on public reporting.

Peer review remains an important mechanism for enhancing the quality of public reporting through independent challenge, constructive feedback and exchange of best practice.

As highlighted throughout this report, there is a continued focus on improving the quality of our work including public reporting. Looking ahead, the Office will continue to explore the possibility of introducing other methods of external quality assurance.

Assembly of certified audit files

Our Quality Manual requires that completed electronic audit files are assembled and closed no later than 60 days after the date of the audit certificate, in line with ISQM 1. This requirement is incorporated into our financial audit methodology and electronic audit software.

During 2025-26, 48 per cent of all audits certified were closed within 60 days (67 per cent in 2024-25; 67 per cent in 2023-24). This indicates a significant shortfall in compliance with the required standard.

In response, the Quality Team will closely monitor compliance, and regular reminders will be issued to managers detailing the requirement to close the audit file within the 60-day time limit. Monthly reports will also be provided to SLT and CMT to highlight instances of non-compliance.

Complaints

We maintain policies and procedures to ensure that complaints and allegations relating to audit work are handled appropriately and in line with professional, regulatory and legal requirements. The NIAO Code of Conduct requires staff to raise any such matters with their line manager, director or, where appropriate, the Chief Operating Officer.

Feedback on the quality of our financial audit work is an important source of insight. This helps us understand stakeholder expectations and identify areas for improvement.

Audited bodies are provided with information on making a complaint in the Report to those Charged with Governance issued at the completion of an audit. In addition, our website provides further information and contact details regarding complaints about the work of the Office.

Two complaints were received during 2025-26 which were both satisfactorily resolved in the year.

Auditee Survey

We undertook a survey of audited bodies during the year and received 55 responses, with 107 organisations invited to participate. Feedback was very positive, with overall impressions being:

98% indicating that NIAO audit staff provided a high quality and professional service;

96% consider that the NIAO’s work leads to improvement in the provision of public services; and

100% considered NIAO good practice guides as a useful resource.