Background

- The Legal Services Agency Northern Ireland (LSANI), an executive agency of the Department of Justice (the Department), was established on 1 April 2015 following the dissolution of the Northern Ireland Legal Services Commission (NILSC) under the Legal Aid and Coroner’s Act (Northern Ireland) 2014. LSANI has retained the functions of NILSC for administering legal aid in Northern Ireland.

- I published a report on 21 June 2016, highlighting a range of concerns in relation to the management of legal aid.

-

- The LSANI’s response to suspected frauds was not effective. The LSANI’s counter fraud strategy was not comprehensive or embedded in day-to-day management. Internal controls had been established but were inadequate to prevent and detect fraud and it was dependent upon third parties to identify suspected fraud.

-

- The LSANI did not have an effective method to predict future legal aid expenditure. In partnership, it and Department sought to develop a new model for forecasting. Despite commendable effort, there remained a number of significant weaknesses, which compromised the model’s ability to predict future expenditure reliably.

- The Public Accounts Committee of the Northern Ireland Assembly has published two reports on the subject of legal aid; one in 2011 and another in January 2017. Both reports were critical of how NILSC and LSANI managed the legal aid budget over a number of years. The January 2017 PAC report contained five recommendations for improving the management of legal aid, one of which related to improving counter fraud measures.

- The audit opinions on the annual accounts of NILSC and LSANI have been qualified since 2003 due to the lack of effective counter fraud arrangements and weaknesses in the financial estimates of provisions for legal aid liabilities in the annual accounts. Whilst progress has been made by the Agency on these issues, particularly in terms of provisions for legal aid liabilities, further work will be needed to resolve them. Consequently, I am qualifying my audit opinion on the 2019-20 financial statements of LSANI.

Purpose of the Report

- I am required to examine, certify and report upon the financial statements prepared by LSANI under the Government Resources and Accounts Act (Northern Ireland) 2001.

- This report explains the background to my qualifications on the LSANI Account for the year ended 31 March 2020.

- I have qualified my opinion on the financial statements due to:

- statistics produced by the Agency estimating that £6.2 million of overpayments and

£2.1 million of underpayments of legal aid costs were made during the year due to official error; and

- limitations in the scope of my work due to insufficient evidence available to:

- satisfy myself that material fraud and error by legal aid claimants and legal practitioners did not exist within eligibility assessments of legal aid applicants and in expenditure from legal aid funds; and

- support the assumptions and judgements used in the determination of

£131.1 million out of a total year end provision for legal aid liabilities of

£152.4 million at 31 March 2020; and the resulting adjustments required to the annual legal aid expenditure.

Qualified audit opinion on irregular legal aid expenditure

- Legal aid expenditure during 2019-20 totalled £98.7 million. There are a number of reasons why this expenditure may not be applied for the purposes intended by the Assembly or conform to the authorities which govern them:

- Official error – where an error can be attributed to the actions or inactions of the Agency;

- Errors made by legal aid claimants and legal practitioners; and

- Fraud.

- The Agency has been working with the Department for Communities (DfC) to develop an estimate of the levels of fraud and error within legal aid expenditure. This work has a number of different strands and will take time to develop. However work undertaken to date enabled the Agency to provide me with an estimate of the level of official error in this expenditure.

- DfC’s Standards Assurance Unit (SAU) selected a sample of 893 payments made between January 2019 and December 2019 and tested whether they had been processed in accordance with legislation. The Agency has used this information to estimate the level of official error in 2019-20 legal aid payments. I am satisfied that the approach is reasonable.

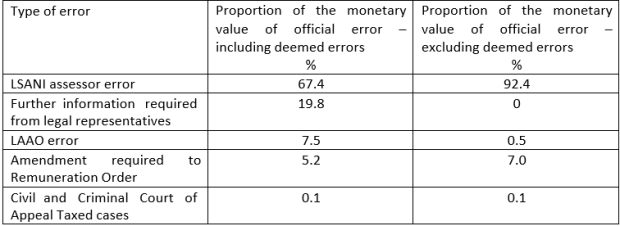

- The estimated level of overpayments in this expenditure resulting from official error is £6.2 million, whilst the estimated level of underpayments is £2.1 million. All overpayments are considered irregular as the expenditure has not been applied in accordance with the purposes intended by the Assembly. Underpayments resulting from official error are not considered to have conformed to the authorities which govern them as the corresponding transactions have not been processed in accordance with the applicable legislation. Therefore the expenditure is considered to be incorrect in 2019-20. Figure 1 provides a breakdown of these errors.

- These estimates include deemed errors of £2.5 million, where further information was required to reach a conclusion on the appropriateness of the payment.

- The types of error identified in this testing included:

- LSANI assessor error - errors identified in the work of LSANI staff during the assessment and payment of legal aid bills submitted;

- Further information required from legal representatives - errors recorded against cases where more information from practitioners to would have been needed to determine whether the payment was correct, resulting in a deemed error;

- Legal Aid Assessment Office (LAAO1) error - errors that occurred in the assessment of financial eligibility for legal aid by the Legal Aid , prior to the transfer of this function to LSANI in March 2019;

- Amendment required to Remuneration Order – updates were required to the legislation which outlines how members of the legal profession should be paid for legal aid work, including travel costs, which was actioned in July 2019;

- Civil and Criminal Court of Appeal Taxed cases - where the monitoring team were unable to view relevant payment information which was held by the courts rather than within LSANI, and this information was not obtained by the assessor at the time of payment. Official errors in this category are also recorded if mistakes are identified in the calculation of a taxed bill.

Figure 1: Percentage of the monetary value of official error per category of error (including and excluding deemed errors)

Source: LSANI – Official error in legal aid payments 2019 end of year report – 3 November 2020

- I asked the LSANI what actions it was taking to address these issues. It told me “The LSANI Accounting Officer and Senior Management Team remain committed to a zero tolerance culture in respect of fraud and error as set out in the Agency’s Business Plan and to identifying and employing best practice and the necessary resources to detect, correct and prevent fraud and error within Legal Aid.

- In 2019, an Error Unit was established to co-ordinate action across the Agency to reduce official fraud and error loss in legal aid. The Agency has worked with the SAU to identify all

the issues driving official error and to develop and agree processes to address them, particularly focusing on common errors with the highest value. This includes aligning business processes with the statutory framework, publishing our approach to assessing claims and detailing the supporting documentation required to accompany payments requests. LSANI internal instructions have been revised to support these initiatives and staff training and awareness provided to embed an accuracy culture. LSANI is recruiting a dedicated training officer to advance this work. LSANI is also recruiting a Head of Counter Fraud and consolidating fraud and error functions within the Agency. A partnership approach has been taken with the Profession to issue guidance, share LSANI findings and clarify

information needs to tackle fraud and error collaboratively.”

Limitation in scope arising from insufficient evidence that material fraud and claimant and legal practitioner error did not exist within legal aid expenditure

- Until the Agency progresses other aspects of its work on fraud and error it cannot provide me with an estimate of the level of fraud and overpayments arising from errors made by claimants and practitioners in legal aid expenditure.

- There are two aspects to the limitation in scope in respect of fraud and errors made by claimants and legal practitioners. Firstly, there was insufficient evidence to support the eligibility of certain legal aid applications: secondly, there was insufficient evidence to support the completeness and accuracy of payments to legal practitioners.

Eligibility

- Whilst some assurance was gained by LSANI from the SAU’s testing on official errors made in eligibility assessments, consideration of other aspects still need to be addressed. Means tested legal aid carries a risk that legal aid is granted to individuals who are not eligible if income details are misstated on initial application, or if changes in financial circumstances that arise during the case are not reported by the claimant. LSANI depends significantly upon third parties to verify the eligibility of legal aid applications. In criminal cases, a judge decides upon an applicant’s eligibility following the LSA checking whether an applicant is in receipt of the benefit the applicant has stated and the court’s determination of the applicant’s financial eligibility if not on a benefit. However, where there is doubt over the applicant’s means or the merits of the case, the court has a legal obligation to resolve those doubts in favour of the applicant. Consequently, it is difficult to estimate how much of criminal legal aid is dependent upon an assessment of income or what benefits are being claimed.

- In civil cases, solicitors and the LSA assess eligibility. The complexity of civil legal aid schemes gives scope for fraud or error in assessing eligibility. My main concerns relate to eligibility:

-

- there is an inherent level of fraud within the benefits system that could impact on legal aid payments. This applies to both civil and criminal legal aid; and

-

- for applicants who are not in receipt of benefits, for example those employed or self- employed, assessments rely upon the declarations made in application forms with supporting documents such as payslips and accounts, in order to assess eligibility.

- The LSANI has invested considerable resources to develop a robust strategy to counter fraud and error, working with the DfC to develop an estimate of the levels of fraud and error in the

system. The interview and review of claimant applications is the next significant part of this work. A methodology has been developed and visits to applicants were due to commence in March 2020 but in light of the Covid 19 pandemic these were cancelled. This work is now due to commence from the start of 2021 but may have to be delivered under alternate means due to social distancing restrictions.

Payments to legal practitioners

- The nature of the legal aid scheme, in making payments to legal practitioners for services, which are provided directly to claimants, creates difficulties for LSANI in determining whether the services were appropriately provided or if overpayments have been made. Currently, LSANI does not produce an estimate of the likely scale of overpayments made to legal practitioners resulting from fraud and error by claimants or practitioners.

- Under the current legislation the Agency does not have any powers to carry out inspections in the offices of legal practitioners involved in legal aid cases. This is a critical gap in the counter fraud arrangements. While the Statutory Registration Scheme is not a counter-fraud initiative, the powers the Agency will acquire in its quality assurance role under the Scheme will enable it to inspect documentation in the offices of legal aid practitioners. This is an essential element of ensuring that publicly funded legal services deliver value for money and its absence undermines the LSANI’s ability to implement a robust quality assurance process. The Access to Justice Order 2003 provided for the introduction of such a scheme. It is concerning that over 17 years later the scheme is still not in place.

- I asked LSANI what progress it had made to develop and implement the registration scheme. It told me “Now that an Assembly is in place, the Department has re-initiated a project to bring forward a Statutory Registration Scheme. The project is being taken forward on a slightly different basis to that on which consultation took place in 2017. The focus is on

introducing a ‘minimum viable model’ which can be built on over time. The challenging target is to develop revised proposals, complete further consultation and lay the four pieces of legislation required by March 2022.” An online registration facility has been developed as part of the implementation of the Legal Aid Management System (LAMS) on 1 July 2019.

This will support the roll-out of the registration scheme once the legislation is passed.

- I have limited the scope of my audit opinion on the regularity of expenditure in 2019-20 because I have been unable to obtain sufficient audit evidence to conclude that a material amount of legal aid expenditure has not been claimed fraudulently or in error by claimants and legal practitioners.

Limitation in scope arising from insufficient evidence to support the estimate of provisions

- The LSANI is not able to determine the specific number of live/active legal aid certificates currently issued. Costs for Civil Legal Aid cases are not standardised, so different firms may bill varying amounts for similar work. The LSANI uses an estimates process to calculate a statistical approximation of the likely number of legal aid certificates. It uses another estimates process to calculate the range of likely average costs of different types of cases. These estimates introduce an unacceptable level of uncertainty and error in the valuation of

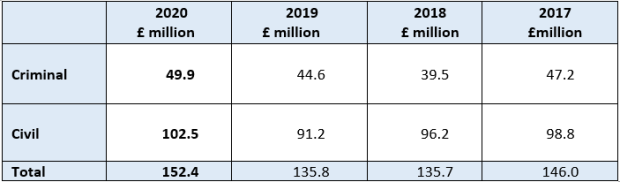

£131.1 million out of total legal aid liabilities of £152.4 million at 31 March.

- These liabilities are referred to as legal aid provisions and the figures are outlined in the table below.

Provision for legal aid liabilities at 31 March

Source: Legal Services Agency

- Previously the Agency used a lifecycle assumption to estimate the number of live certificates to be valued in the provision. When LAMS came into operation in July 2019 the Agency changed its provisions methodology and instead used the number of cases on LAMS as a starting point, with further refinements for certain items. Whilst this was more robust than the previous approach, further housekeeping work on the number of cases held on LAMS is needed and the Agency plans to take this work forward in the coming months. The average costs used in the estimation of the provision was derived from a range of reports extracted from the old case management system, a process which was complex and manually intensive. The Agency intends to revise the methodology for calculating average case costs in the coming year, by extracting information at a more granular level from LAMS instead. Some audit evidence that I required was not available to me, meaning that I could not gain sufficient assurance on the migration of data from the old case management system to LAMS, the extraction of data from LAMS and cost information from the old system and the calculation of average costs.

- Most legal aid provisions are calculated using this model (£122.1 million) however more complex cases are valued outside of the model (£30.3 million). Whilst I have sufficient assurance on the assumptions used to calculate £21.3 million of provisions valued outside of the model, I do not have sufficient audit assurance over average case costs applied in arriving at £8.4 million of this element of the liability and of whether the recognition of a liability for a further £0.6 million was appropriate.

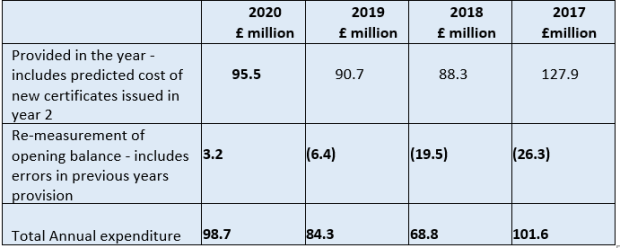

- The annual legal aid expenditure is the total predicted cost for all new certificates issued during the year adjusted for differences between the original estimate and the amounts actually paid for certificates issued in earlier years. The annual expenditure has been adjusted this year by +£3.2 million (- £6.4 million 2018-19) for these differences. The adjustment is one indication of the level of error in the previous year’s provisions estimate.

Legal Aid Annual Expenditure at 31 March

Source: Legal Services Agency

- The level of error in estimated provisions has reduced considerably over the last four years, but it remains materially inaccurate. It is not possible to assess the level of error in provisions until the Agency makes the legal aid payments in the following year.

- Significant work has been undertaken by LSANI to improve the provisions model and it is continuing to work towards providing a reasonable estimation of future legal aid liabilities. Its future plans for further work on LAMS and the provisions model will help refine the estimation of legal aid liabilities further, particularly once the LAMS’ functionality is fully utilised. Considerable progress has been made in recent years in resolving the issues relating to this estimation but further work is needed. For the estimation in 2019-20 we continue to have specific concerns about:

-

- the accuracy and completeness of the numbers of legal aid certificates; and

- the quality of management information used in the provisions valuations.

- I have qualified my audit opinion on the truth and fairness of the amount provided for legal aid liabilities at 31 March 2020 due to insufficient evidence to support the current provisions methodologies and the judgements made when calculating provisions.

Conclusions

- The Agency continues to work with the DfC to estimate the levels of fraud and error related to legal aid and to develop an effective counter fraud strategy. Work to enable the level of applicant fraud and error to be estimated was due to commence in 2020 with visits to a sample of applicants, but the impact of the Covid 19 pandemic has now pushed this back to 2021. It is disappointing that progress has been slower on developing a methodology to determine the level of fraud and error in payments to legal professionals, and considerable work is still needed in this area. The Agency has a draft methodology for estimating the level of legal practitioner fraud and error and initial testing to assist in the development of this methodology will be taken forward on a ‘test and learn’ basis during 2021. The Agency told me “Lack of resource has been a hampering factor and covid-19 related recruitment restrictions have meant the Agency is only now able to move to fill the Head of Branch post which will lead this work but has been vacant since January”. There remains insufficient

evidence to determine the level of claimant or practitioner fraud or error regarding the eligibility of legal aid payments or payments to legal practitioners in 2019-20. The Agency has estimated £8.3 million of over and underpayments for legal aid which was irregular during 2019-20 due to official error. I expect this to decrease in future years as the Agency works to address the issues identified. Only when the Agency is able to determine an estimate for applicant and practitioner fraud and error, and the underlying causes, can it act to improve its preventative and detective controls to protect public money. There is still much work to be undertaken by the Agency in the coming years and tangible progress is essential.

- The Department and the Agency have revised the methodology for determining legal aid provisions. This provides a more robust estimation of legal aid liabilities but the accuracy is limited by the quality of management information provided and there was insufficient audit evidence to support the completeness and accuracy of the provision. This situation should improve in future years with the housekeeping work planned on the LAMS system, and improving the calculation of average costs.

- The Public Accounts Committee took evidence on my report on the Management of Legal Aid on 29 June 2016 and reported its findings on 11 January 2017. Since then I have tracked progress made on addressing the committee’s recommendations. Whilst I accept that there were significant constraints on progress in some areas before a Minister and a legislative Assembly were back in place, some progress has now begun to be made and I would encourage the Department and the Agency to accelerate their work in this area.

- I will continue to keep the implementation of the Committee’s recommendations under review.

KJ Donnelly

Comptroller and Auditor General Northern Ireland Audit Office 106 University Street

Belfast BT7 1EU

November 2020