Introduction

- In 2020-21, the Department for the Economy (the Department) was tasked by the Executive to implement urgently a series of business support schemes designed to ease the difficulties and disruption being faced by businesses arising from the COVID-19 pandemic. Expenditure on a number of the schemes continued into the 2021-22 financial year, albeit at much reduced expenditure levels.

- I noted in my 2020-21 report, these schemes were delivered at extreme pace and in a challenging environment. The situation was made worse by the imposition of home working and a lack of appropriate resources. Given the urgency and speed with which these schemes were designed and delivered, the accounting treatment, and consequently the audit activity, has been complex and at times, a challenge.

Purpose of the report

- Under the Government Resources and Accounts Act (Northern Ireland) 2001 I am required to examine, certify and report upon the financial statements prepared by the Department for the Economy (the Department). This report explains the background to my qualifications on the Department’s Resource Accounts for 2021-22. In addition, it provides information on certain other issues I identified during the audit which did not result in a qualification of my audit opinion, together with an update on other recurring matters.

- All qualifications of my opinions on the Department’s Resource Accounts in 2021-22 relate to grant schemes established to support businesses during the pandemic. Within this report I comment on qualifications on two separate groups of COVID-19 business support schemes administered during 2021-22:

-

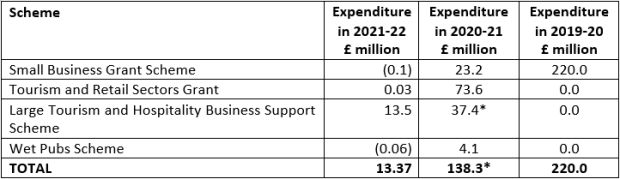

- Department administered schemes of £13.4 million in 2021-22 and £138.3 million (restated) in 2020-21 – see Figure 1; and

- Invest NI administered schemes of £14.7 million in 2021-22 and £129.8 million in 2020-21– see Figure 3.

Qualified audit opinion on the financial statements

- The Department sponsors Invest Northern Ireland (Invest NI), a Non Departmental Public Body which is not part of the Department and whose accounts are not consolidated with the Department’s. The Department instructed this body to include expenditure on a number of emergency COVID-19 business support grants in its financial statements using its powers under the Industrial Development (Northern Ireland) Order 1982. The Invest NI 2021-22 financial statements included £13.4 million for this expenditure and £138.3 million (restated) for related prior year expenditure. The opening balance of net assets at 1 April 2020 was also affected by transactions related to these schemes. However, it is my opinion that these schemes were in reality administered and controlled by the Department itself meaning the Department should

have included the expenditure in its own accounts; but it did not, as it did not have the legislative power available to it to incur the expenditure.

Figure 1: Department for the Economy administered COVID-19 business support schemes

Source: Invest NI 2021-22, 2020-21 and 2019-20 Annual Report and Accounts

*These figures have been restated since the C&AG’s 2020-21 report, see paragraph 13-14 below.

- This unusual accounting arrangement was used because the Department did not in fact have the legal authority to make the grant payments itself and determined it would take too long to obtain such powers under the Financial Assistance Act (Northern Ireland) 2009. The aim of this arrangement was to reflect scheme expenditure in the entity with the appropriate legal authority to make the payments. Invest NI has the relevant authority under the Industrial Development (NI) Order 1982. So essentially the Department designed and delivered these schemes and incurred the expenditure, while instructing Invest NI to include the expenditure in its accounts on the basis that it had the correct legal powers. However, neither International Accounting Standards nor the Government Financial Reporting Manual (FReM) allow for legal vires as a basis for recognition.

- The Department, Invest NI, DoF’s Land & Property Services (LPS) and Account NI all agreed a Memorandum of Understanding (MOU) which set out the roles and responsibilities of those involved in the policy, design, operation and delivery of the Covid-19 business support grants. In the MOU, the sole duty allocated to Invest NI is to “record the full estimated costs of the grant scheme on an accruals basis in 2019-20 budgets and accounts”. However, the primary duties in relation to establishing the scheme, its design and delivery, payment approval and taking responsibility for any losses arising from its administration, were allocated to, and accepted by, the Department. While there was some early consultation with Invest NI on the scheme, no Invest NI staff were involved in scheme delivery and Invest had no role in the payments that were made to grant recipients.

- The Department is required to provide financial statements which show a true and fair view of its financial transactions and its financial position. Therefore, instructing Invest NI to account for this expenditure rather than accounting for it itself, led to misstatements within the Department’s resource accounts in 2021-22, including the corresponding figures for 2020-21 and the opening balance of net assets at 1 April 2020. The Department only reflected the expenditure on a cash basis and described it as Grant-in-Aid to Invest NI, rather than Grant expenditure that it had paid directly to recipients. I have therefore qualified my audit opinion on the financial statements.

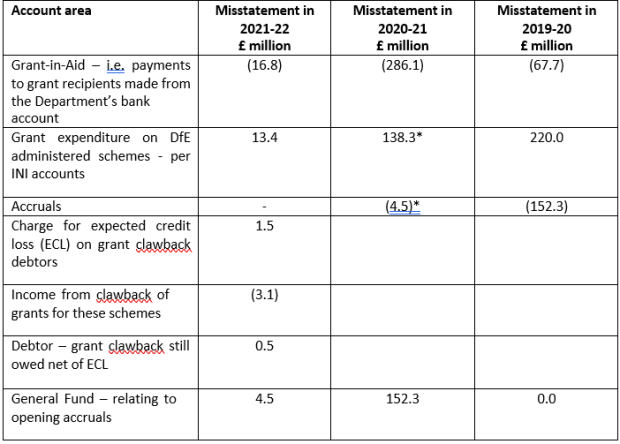

Figure 2: Misstatements resulting from the accounting treatment for Department for the Economy administered COVID-19 business support schemes

*These figures have been restated since the C&AG’s 2020-21 audit certificate, reducing each by

£2.5 million, see paragraph 13-14 below.

- The Department consulted with the Departmental Solicitor’s Office (DSO) and the Department of Finance (DoF) on this novel accounting treatment and both bodies gave their support to it. However, the legal advice is not based on the application of relevant accounting standards and DoF, although supportive, did not issue an accounts direction to the Department to provide a clear basis for the approach taken. It is a requirement of my role to form an independent audit opinion on whether the financial statements reflect a true and fair view, and comply with accounting standards and the Government Financial Reporting Manual. Since the Department controlled and administered the schemes and made the payments to recipients, without any meaningful involvement of Invest NI, it is my opinion that this money was spent by the Department.

- This is a matter of ‘substance over form’, an accounting concept which means that, in order to present a true and fair view, financial statements should reflect the economic substance of transactions or events, not their legal form. Financial statements representing a legal form that differs from the economic substance, do not result in a faithful representation. Following a detailed technical review, it is my opinion that the economic substance of the grant schemes outlined in Figure 1, is that the Department, not Invest NI, controlled and delivered the schemes and made the payments to recipients with assistance from the Land and Property Services (LPS). As a result, these transactions should have been recorded in the Department’s financial statements. I also note that the Invest NI Accounting Officer had no opportunity to govern those schemes or influence the expenditure.

- I provided the Department with an opportunity to reconsider its accounting treatment and proposed that it make an adjustment to its 2020-21 financial statements to resolve the issue.

However, after consideration, it decided not to do so. There was a further opportunity for the Department to resolve this issue by amending its 2021-22 financial statements, including its corresponding figures for 2020-21 and opening balances at 1 April 2020, but it declined to do so. Therefore, I must provide my opinion on the basis of my disagreement with the accounting treatment of these grants and the related transactions and balances.

- I have also qualified my audit opinion on the financial statements on a related issue, because they do not disclose this expenditure as material irregular expenditure as required by its Accounts Direction. I have provided further detail on this in paragraph 16 below.

An error in the prior period had not been notified on a timely basis

- I issued my audit opinions on the Department’s 2020-21 financial statements on 2 March 2022, having received representations from the Accounting Officers of both the Department and Invest NI that they had provided me with the relevant audit information that I would need to undertake my audit work. As noted in Figure 2 above, in its 2021-22 financial statements Invest NI has restated the corresponding figures relating to 2020-21 for DfE administered COVID-19 business support scheme grants and associated accruals, after reducing both by £2.5 million following identification of an overaccrual. Since it was the Department that administered the schemes and made the payments, they possessed all the relevant information. Invest NI was therefore dependent on the Department for the provision of information on these financial transactions. Whilst both bodies appear to have been aware of a potential overaccrual in the 2020-21 Invest NI financial statements, the Department had clearer detail on the issue as far back as January 2022.

- Both bodies had a responsibility to bring this to my attention before I certified the Department’s 2020-21 financial statements, but failed to do so. Although both assure me that this was not intentional, I am none-the-less concerned that this was not disclosed to me in a timely manner and I expect both bodies to put communications in place to prevent this from happening again in the future. Had I received this information before I had certified the Department’s 2020-21 financial statements, I would have taken account of this additional error in my report and audit certificate on those accounts.

Qualified audit opinion on irregular expenditure

- In addition to forming an opinion on whether the financial statements show a true and fair view I am required to give an opinion on the regularity of transactions, by considering if the income and expenditure has been applied for the purposes intended by the Assembly and whether the transactions comply with the authorities which govern them.

The Department did not have legal powers in place to cover expenditure on certain COVD-19 business support schemes it administered

- Since in my opinion, it was the Department that spent £13.4 million in 2021-22 on the COVID-19 business support grants in Figure 1 which it administered, I must now consider the regularity of this expenditure. As outlined in paragraph 6 above, the Department did not have legal powers in place to provide legal vires for this expenditure. As such, I consider expenditure of £13.4 million for 2021-22 of grants administered by the Department to be irregular, albeit that as shown in Figure 2, it has not been appropriately reflected in the financial statements at this value or description.

- As I noted in my report on the Design and Administration of the Northern Ireland Small Business Support Grant Scheme, looking ahead, it is important that departments consider what powers may be available to facilitate urgent Executive business, how those powers can be used and how collaboration will work in a crisis.

There was insufficient audit evidence that eligibility criteria for certain COVID-19 business support schemes had been met

- As part of my work on whether expenditure is regular, I must gather independent audit evidence to assess whether grants administered by Non-Departmental Public Bodies (NDPBs), which were funded by the Department, complied with the eligibility criteria established for each scheme.

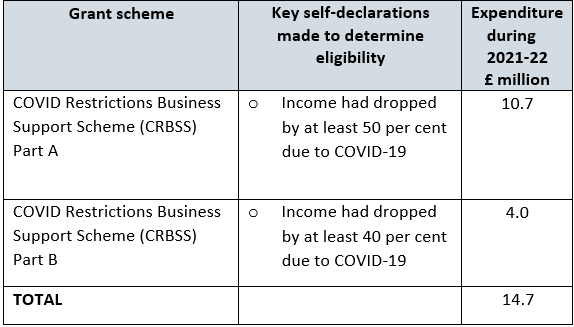

- Part of the Grant-in Aid expenditure within the Department’s financial statements relates to funding it provided for COVID-19 business support schemes run by Invest NI, which relied on self- declarations from applicants as evidence that eligibility criteria for these schemes had been met. As the schemes were designed to rely on self declaration, sufficient appropriate audit evidence was not available to me to determine whether all of the eligibility criteria were met. Expenditure on these schemes reflected in the Invest NI financial statements totalled £14.7 million in 2021-22 and is set out in Figure 3 below.

- All of these schemes relied heavily upon self-declarations made by applicants to confirm eligibility. Therefore, Invest NI could not provide me with sufficient appropriate audit evidence to verify whether the self-declarations made were, in fact, accurate. There were no alternative audit procedures available to me to obtain sufficient appropriate audit evidence to inform my regularity audit opinion in respect of these schemes.

Figure 3: Invest NI administered COVID-19 business support schemes in 2021-22 for which sufficient audit evidence was not available to support self-declarations

Source: Invest NI 2021-22 Annual Report and Accounts

- Approval for the implementation of these new schemes was given by Ministerial Direction, since the Department’s Accounting Officer was unable to provide evidence that these schemes would provide value for money or that there would not be an unacceptably high risk of error or loss of funds. Reliance on self-declarations without corroborating evidence does not mitigate the risk of fraud and error occurring.

Reporting on fraud and error in the COVID-19 business support schemes

- The Department is required to disclose a fraud and error analysis of its’ COVID-19 government support schemes, providing an evidenced based estimate of the extent of the level of fraud and error in these schemes; identifying risks of fraud and error; and explaining how these risks are managed. In addition, its Accounts Direction requires disclosure of any material irregular expenditure or income. The Department has made these disclosures in the Performance Report and within Note 24 of the 2021-22 Annual Report and Accounts.

- Protecting public funds from fraud and error is a key responsibility for all public bodies. We accept that these schemes were delivered in response to an emergency situation, nonetheless, public funds were at risk, particularly in light of self-declarations being accepted by the organisation as proof of eligibility for the grant schemes that it administered, as shown in Figure 3.

- In my report on the Department’s 2020-21 financial statements, I recommended that post payment checks were performed, proof of eligibility from corroborating evidence sought and, where necessary, funds are recouped.

- The Covid Grants Fraud and Error Project (the Project) was established by the Department in December 2020 “to review all of DfE’s Covid-19 Business Support Grant Schemes to validate and provide assurance of payments under the schemes; identify fraud and error; initiate recovery measures and manage the risk of error and fraud going forward”. Ten schemes were reviewed during the Project, with a total spend of £516.2 million between 2019-20 and 2021-22. The Project was terminated in November 2021, having estimated a fraud and error rate of 2.08%, suggesting that £10.7 million of spend over that time had been incurred due to fraud and error. By June 2022, the Department had recovered or agreed repayment plans for £4.9 million.

- Internal audit has recently undertaken a review of the Project. I reviewed the draft internal audit report and note that:

-

- An external support contract for staff substitution of a multi-disciplinary team with expertise in fraud and error risk, fraud investigation and data analytics was awarded under a Direct Award Contract. The estimated budget at the outset of this work was £350,000 in total. However before all phases of the work were completed, the contract was terminated with actual costs of £305,000. It was estimated that to complete the work in full would have cost an additional £267,000. The Project continued within the Department, however without this work being completed, all of the objectives of the Project may not have been met.

- Testing focussed solely on the first three schemes and targeted the risk of duplication of support with other COVID business support schemes. Testing was not undertaken to address other key risk areas identified, including the validity of self-declarations provided to confirm compliance with certain eligibility criteria for Invest NI administered schemes, despite the recommendation in my report on the 2020-21 financial statements that this was undertaken. A broad assumption was made by the Department that the fraud and error rate for risk areas not tested would be the same as that rate identified by duplicate testing. The Department told me that it was its best estimate, based on the evidence available at the time.

- A risk assessment was made for each of the schemes reviewed. The methodology used to calculate an overall risk rating meant that inclusion of a number of low risk aspects reduced the overall scheme risk rating, despite high risk aspects being identified. For example for the CRBSS Part B scheme there were 3 high, 3 medium and 21 low risks, creating an overall assessment of low risk. However, given that this scheme used self-declarations to confirm

certain eligibility criteria there was a clear risk of significant fraud and error. While the Department’s low risk ratings of the schemes not tested were used to inform the

Department’s decision to terminate the Project before all phases of the work had been completed, the decision was also informed by the detailed risk assessments.

-

- Not all schemes and not all high risks were tested, and broad assumptions were used that the duplication error rate identified for the three schemes tested could be used to estimate fraud and error for other risk categories and across the other schemes. In addition, the work undertaken was not subject to review by qualified statisticians. This means that the fraud and error rate calculated may not be statistically valid, and the actual level of fraud and error across these schemes may be higher or lower than estimated.

- Whilst I acknowledge the recoveries made to date and payment plans agreed, by the Department’s own estimation there may have been over £5 million of fraud and error on the schemes which has not been investigated and recovered. Indeed, given the weaknesses in the methodology used to calculate an error rate, I am concerned that fraud and error not addressed could be significantly more. Whilst I acknowledge the urgent need to support businesses at the time meant that normal controls could not be applied before the grants were issued, I am disappointed to note the clear weaknesses in the Department’s Project.

Other issues identified which did not lead to audit qualification

Non-Domestic Renewable Heat Incentive (RHI) Scheme

- In five years from 2015-16 to 2019-20, I reported on aspects of the RHI scheme including its total cost, progress of site inspections, judicial reviews following amendments to reduced tariffs payable under the scheme, and the future of the scheme. In 2021-22 costs of the scheme were again under budget, at £6.4 million (for both domestic and non-domestic RHI schemes), well below estimated costs of £33.5 million. As in previous years, I was still unable to obtain sufficient evidence that the controls over spending of £3.3 million on the non-domestic RHI scheme were adequate to prevent or detect abuse of the scheme. I have not, however, qualified my audit opinion on the 2021-22 financial statements in this respect because I do not consider the issue to be material for 2021-22.

- During 2021-22 £0.83 million (2020-21 : £2.3 million) of RHI expenditure relating to payments made in respect of applications received between 1 April 2015 and 28 October 2015 was irregular since DoF approval had not been renewed for the scheme during this period. The total irregular expenditure relating to these applications continues to accumulate each year, however I do not consider the amount relating to 2021-22 payments to be material.

- In October 2021 a judicial review against the change in tariffs brought about by the Northern Ireland (Regional Rates and Energy) Act 2019 was dismissed by the High Court in October 2021. An appeal, however, is ongoing in respect of reduced tariffs made under the RHI Scheme (Amendment) Regulations (NI) 2017. In February 2021 the Department launched a consultation on the future of the scheme, with its preferred option to close the scheme with compensation paid to legitimate current participants. I will continue to monitor future developments.

- I published a report in March 2022 on the progress made in implementing recommendations made by the RHI public inquiry. This report considered developments in governance arrangements across the Northern Ireland Civil Service (NICS), and specifically within the Department since issues around RHI emerged. It also considered what improvements have been made across government in response to recommendations made by the independent public

inquiry into the Non-Domestic RHI Scheme. It noted that two years on from the publication of the RHI Inquiry Report, progress in addressing the recommendations across the NICS has been disappointing in areas. I welcomed improvements in governance structures at the Department and noted the Organisational Development Programme it has set up, under which it will take forward its own response to a number of the Inquiry’s recommendations. However, it is critical that this is supported by an appropriate corporate culture within the Department, grounded in

the Nolan Principles to ensure the highest standards in public life, underpinned by transparency.

High Street Voucher Scheme (HSVS)

- In 2021-22 DfE delivered the High Street Voucher Scheme (HSVS). At a total cost of almost

£141.6m, the scheme formed part of the wider range of COVID-19 support packages agreed by the Northern Ireland Executive to assist businesses since the onset of the pandemic. The purpose of the scheme was to provide financial assistance to businesses through the provision of pre-paid cards with a value of £100 each to eligible applicants which could be then used to buy goods and services from businesses physically present in Northern Ireland. Arrangements were made to exclude the use of the cards for certain types of businesses such as gambling and online sales.

- Issues arose when:

- some cards were not received; or

- some cards could not be activated; or

- the full balance could not be spent for reasons outside of the cardholder’s control; or

- eligibility was not verified due to a service failure by the Department.

- This necessitated a ‘remedy scheme’ where cash payments of £0.6 million were made into individuals’ bank accounts. The High Street (Coronavirus, Financial Assistance) Scheme Regulations (Northern Ireland) 2021 and the Interpretation Act (Northern Ireland) 1954 allowed the Department to make these cash payments. Whilst I consider the payments to be regular, because the Department had the legislative powers to make them, I note that the Department had no practical way to restrict how recipients used the remedy payment, as it could with the pre-paid cards. This means that remedy payments may not have been used to provide financial support to Northern Ireland businesses as was originally intended.

- The Accounting Officer noted in his request for a Ministerial Direction for the scheme there were significant doubts over the value for money and impact on the high street. The scheme has received a considerable amount of media coverage, particularly in trying to assess the impact that it has made. I may consider this in more detail at a later stage.

Updates on matters noted in previous audits

Presbyterian Mutual Society

- At the height of the financial crisis in 2008 the Presbyterian Mutual Society (PMS) went into administration. Loans of £225 million were made by the former Department of Enterprise to bail out PMS. Of this balance, £50 million is at the bottom of the creditors’ priorities and is considered unrecoverable. The remaining £175 million was repayable by instalments and was due to be settled in full by November 2020. The Joint Supervisors of the PMS requested an extension to this repayment period due to the pandemic limiting its ability to sell assets to fund the repayments. Following professional advice on the matter, the Department extended the repayment period to November 2022.

- At 31 March 2022, the total amount still due was £28.7 million, however only £14.5 million of this is expected to be recovered and the financial statements reflects this. The actual loss which materialises will depend upon market conditions at the time that remaining assets are sold.

HMS Caroline

- I reported last year on the significant challenges the Department has faced restoring HMS Caroline and transforming the ship into a viable marine heritage visitor attraction. Visitor numbers have been disappointing since the ship’s opening, resulting in operating deficits. It was then closed to the public in March 2020, due to the pandemic.

- The interim operating agreement between the Department and the National Museum of the Royal Navy (NMRN), who operated the ship on behalf of the Department, expired in June 2020. The Department was unable to put a new arrangement in place, establish a new funding model or to procure a new operator. The attraction therefore remained closed. During this time the NMRN continued to provide oversight and maintenance of the ship, and the Department met the associated costs.

- In December 2021, a tripartite agreement was reached between the Department, the National Memorial Heritage Fund and the NMRN. Under this agreement an endowment fund was established to maintain the ship as a visitor attraction in Northern Ireland to 2038 at least, whilst releasing the Department of future obligations and liabilities. The endowment fund was agreed at £12.5 million, with the Department contributing £10 million and the National Memorial Heritage Fund contributing £2.5 million.

- The Department advised me that plans for re-opening this visitor attraction have been discussed with NMPN and HMS Caroline should be ready to be open in Autumn 2022.

Conclusion

- The majority of issues in this report are the outworkings of issues which occurred in previous years. I encourage the Department to continue making improvements to its governance structures and the work it is taking forward through its Organisational Development Programme.

Dorinnia Carville

Comptroller and Auditor General

Northern Ireland Audit Office

106 University Street

BELFAST

BT7 1EU

8 September 2022