Introduction

- The Department for Communities (the Department)’s Child Maintenance Service (CMS) is responsible for administering statutory child maintenance schemes in Northern Ireland and the management of client funds relating to these schemes. Client funds are based on either the 2012 child maintenance scheme (CMS 2012 scheme) or the 1993 and 2003 legacy schemes, operated by the previous Child Support Agency.

- Under the Government Resources and Accounts Act (NI) 2001, the Department of Finance (DoF) has directed the Department to prepare a Statement of Client Funds Account. This is a receipts and payments account that shows receipts of child maintenance from paying parents and payments3 to receiving parents, with responsibility for the children concerned.

- The Department is also required to provide a summary of the amounts due in respect of unpaid maintenance assessments together with its assessment of the extent to which they are likely to be collected. The administration costs of running the CMS are accounted for through the Department’s Resource Account.

- I am required to examine and certify the CMS Client Funds Account and report whether the financial statements are properly presented and, whether in all material respects the receipts and payments and financial transactions conform to the authorities which govern them.

- This Report reviews the results of my 2021-22 audit of the Child Maintenance Service Client Funds Account.

Key findings

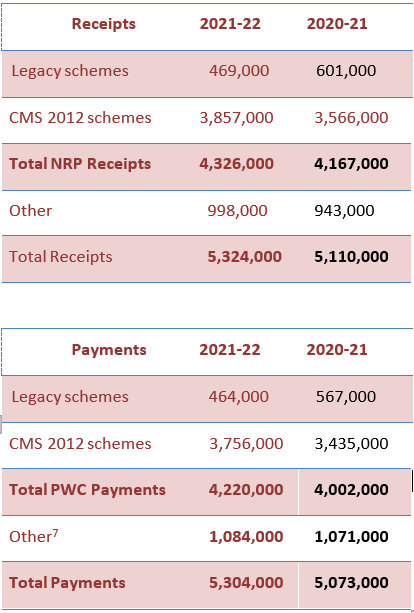

6. CMS 2012 scheme receipts for 2021-22 are approximately £3,857,000 (2020-21: £3,566,000) and associated payments are approximately £3,756,000 (2020-21: £3,435,000). For 2021-22 the Department estimated the overall rate of error in receipts and payments for these cases to be 0.52 per cent (2020-21: 0.73 per cent), a monetary impact of approximately £21,000 (2020-21: £27,500).

- In relation to legacy schemes, receipts this year are £469,000 (2020-21: £601,000) and associated payments are £464,000 (2020-21: £567,000). There is historic evidence of material inaccuracies in the maintenance cases assessed under these schemes and the Department is unable to estimate the level of error in them.

- Therefore I consider that the level of irregularity in receipts and payments continues to be material and I have qualified my regularity audit opinion again this year.

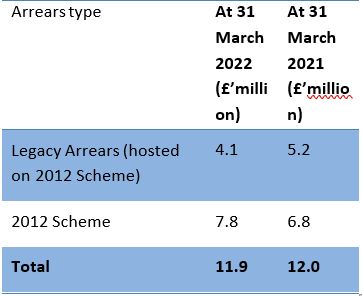

- Outstanding maintenance arrears are currently £11.9 million (2020-21: £12 million), made up of £7.8 million (2020-21:£6.8 million) from cases operating under the CMS 2012 scheme which can be substantiated and £4.1 million (2020-21: £5.2 million) transferred from the legacy schemes, for which I was unable to obtain satisfactory evidence. Arrears relating to the legacyschemes are continuing to reduce and are now 34 per cent (2020-21: 43 per cent) of the overall arrears’ balance of £11.9 million. Consequently, I have qualified my audit opinion on the financial statements in respect of this part of the arrears balance.

Statutory Child Maintenance Schemes

- The current statutory child maintenance scheme was introduced in 2012 (CMS 2012 scheme). Two earlier schemes introduced in 1993 and 2003 (legacy schemes) have now been closed and cases with “arrearsonly balances” have transferred to the 2012 scheme.

- The CMS 2012 scheme is supported by a Department for Work and Pensions’ IT system and obtains information on income directly from Her Majesty’s Revenue and Customs’

records and the Department’s social security systems to carry out assessment calculations.

- The IT systems supporting the legacy schemes were unable to generate the information needed to prepare the Account or provide accurate assessments. The level of complexity in carrying out maintenance assessments under the legacy schemes, together with inadequate computer systems, has led to significant levels of error in historical child maintenance assessment calculations. These in turn continue to have a cumulative impact on the accuracy of current legacy scheme amounts collected from parents who pay maintenance to CMS (paying parents) and those who receive payments from CMS (receiving parents). Accordingly, every year since the creation of the Northern Ireland Child Support Agency in April 1993, I have qualified my audit opinion on this Account in respect of these receipts and payments.

Receipts and payments

- The Department is required to calculate maintenance assessments in accordance with relevant legislation. Where an error is made in a maintenance assessment both the receipt and associated payment are incorrect and therefore have not complied with the relevant legislation. The Department has advised that due to the closure of existing legacy scheme cases it is not possible to generate a statistically valid sample which can be used to test the accuracy of these assessments.

The IT system underpinning the CMS 2012 scheme automatically determines the maintenance decision in 74 per cent (2020-21: 78 per cent) of cases. Where the decision is more complex Department staff have to intervene manually. The Department’s Case Monitoring Team (CMT) estimates the level of error in maintenance assessments by calculating the monetary value of error4 for CMS 2012 decisions which provides an estimate of the level of child maintenance that has been paid incorrectly.

- For 2021-22 CMT tested a statistically valid sample5 of both fully automated decisions and those requiring manual intervention, estimating an error rate of 1.8 per cent (2020-21: 2.9 per cent) for decisions needing manual intervention while fully automated cases were found to be 100 per cent accurate.

- This year the combined value of the estimated error is 0.52 per cent (2020-21: 0.73 per cent) of receipts under the CMS 2012 scheme (see Figure 1) which produces an estimated monetary value of error of approximately £21,000 (2020-21: £27,500). I am satisfied that this is a reasonable measure of the level of error in CMS 2012 receipts.

Figure 1: Breakdown of Receipts for 2020-21 and 2021-22

Source: Department for Communities and notes to the CMS 2021-22 and CMS 2020-21 accounts

- Due to the fact that it is not possible for the Department to generate a statistically valid sample to test the accuracy of these assessments I am not able to quantify the level of irregularity in the legacy scheme receipts and payments. The Department has estimated an error for the CMS 2012 scheme of approximately £21,000 (2020-21: 27,500). Therefore the

- Due to the fact that it is not possible for the Department to generate a statistically valid sample to test the accuracy of these assessments I am not able to quantify the level of irregularity in the legacy scheme receipts and payments. The Department has estimated an error for the CMS 2012 scheme of approximately £21,000 (2020-21: 27,500). Therefore the

Level of maintenance arrears

- The Department is required to disclose the amount owed by paying parents in respect of maintenance assessments. Where a paying parent does not make payments in accordance with the maintenance assessment and the Department is responsible for collecting those payments, any missed or shortfall in payment is recorded as debt.

- Where the Department has made incorrect maintenance assessments, any arrears accruing will also be at an incorrect rate. Historic inaccuracies in maintenance assessments, in the legacy child maintenance schemes, have therefore led to misstatements in individual arrears that support the outstanding legacy arrears balance. Figure 2 sets out the split between the arrears relating to legacy schemes and those relating to the 2012 scheme for the last two years.

Figure 2: Split between legacy and CMS 2012 arrears in 2021-22 and 2020-21

Source: CMS Accounts 2021-22

- The total arrears at 31 March 2022 represent the cumulative amount of arrears since child support arrangements were established in 1993. In line with legislation, the Department can only write-off arrears in very limited circumstances. The total amount of unpaid maintenance assessments of £11.9 million (2020-21:£12 million) at 31 March 2022 is shown in note 5.1 to the accounts. This figure comprises legacy arrears of £4.1 million (2020-21: £5.2 million) and arrears recorded on the system underpinning the CMS 2012 scheme of £7.8 million (2020-21:

£6.8 million).

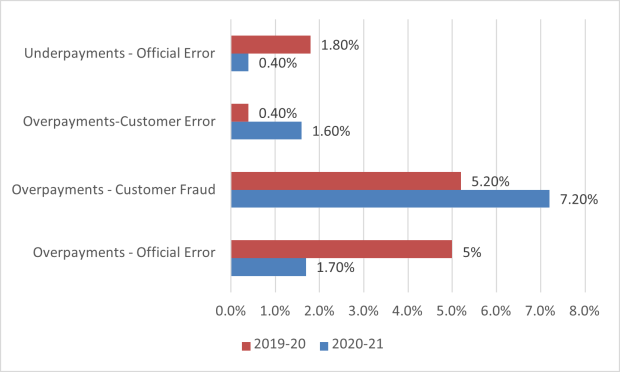

The Department has told me that the level of legacy arrears is unlikely to reduce significantly in the short- term as some legacy recoveries are very low value. Figure 3 shows that the percentage of legacy arrears has been steadily decreasing over the last five years and is currently just over a third of the total arrears balance. While the Department is able to provide me with the necessary supporting documentation for the arrears arising under the CMS 2012 scheme it is unable to do so for those arising from legacy schemes nor is it able to estimate the value of misstatements as a result of inaccurate assessments. I have therefore qualified my opinion on the financial statements in relation to the element of the arrears balance arising from legacy schemes of £4.1 million.

Figure 3: Trend in breakdown of arrears relating to legacy schemes and the CMS 2012 scheme

KJ Donnelly

Comptroller and Auditor General Northern Ireland Audit Office

1 Bradford Court Galwally

Belfast

BT8 6RB

07 July 2022