Introduction

- In each of the past four years, I have reported on significant concerns surrounding the operation of the non-domestic Renewable Heat Incentive (RHI) scheme. Each of my reports attached to the Department for the Economy’s (the Department) Resource accounts have outlined significant weaknesses in the scheme and set out the ongoing actions proposed by the Department to address these weaknesses.

- My initial report in June 2016 was followed by seven evidence sessions of the Public Accounts Committee between September 2016 and January 2017. The Renewable Heat Incentive Inquiry was then established to carry out an in-depth investigation of the operation of the scheme and published its report on 13 March 2020, making a number of recommendations to be taken forward. I have been asked to monitor and review progress in how these recommendations are being implemented and will report back to the Assembly in due course.

- My report below provides an update on:

- the running of the scheme including costs and inspections;

- why I have again decided to qualify my regularity audit opinion; and

- the future of the scheme.

- I have also qualified my regularity audit opinion on payments to North/South Bodies and the Small Business Grant Scheme (established in March 2020 in response to the Covid-19 pandemic) and my report provides further details in relation to these matters. In addition, I also provide an update on the loan due from the Presbyterian Mutual Society and why the Department has incurred an additional £1.4 million of costs in 2019-20 relating to HMS Caroline.

Non-Domestic Renewable Heat Incentive (RHI) Scheme Total costs in 2019-20

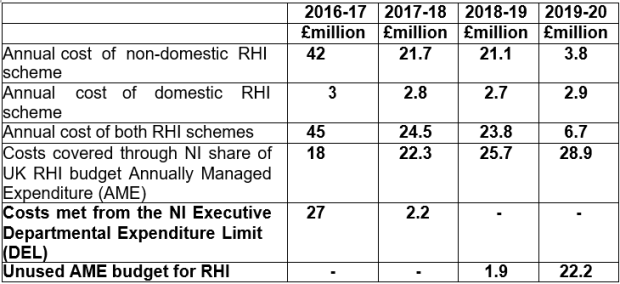

- In order to reduce costs of the scheme, the Department imposed significant changes to the tariff paid from 1 April 2017 to all users of the scheme. Legislation was passed through Westminster to extend this revised tariff rate to 31 March 2019. Further substantial reduction in RHI tariffs from 1 April 2019 have significantly reduced the cost of the scheme in 2019-20 to £6.7 million, well below the Annual Managed Expenditure (AME) budget available by £22.2 million.

Table 1: Annual costs of the RHI scheme

Source: Department

- I asked the Department to comment on this underspend and how it intends to utilise this budget. The Department told me that the tariff payments, as implemented by the 2019 Regulations, were in line with State aid requirements. AME allocations are demand lead and any unutilised budget cannot be allocated elsewhere as these must be returned to HM Treasury. It is not uncommon for AME underspends to occur across Government. The NI Executive’s “New Decade, New Approach” agreement commits to closure of RHI and replacement with a new scheme. The Department is currently developing an Energy Strategy for Northern Ireland which will include policy to support the achievement of the UK Government’s legislated target of net-zero carbon by 2050. Possible incentives for green energy, including renewable heat, are part of the consideration in the process of developing the new Energy Strategy.

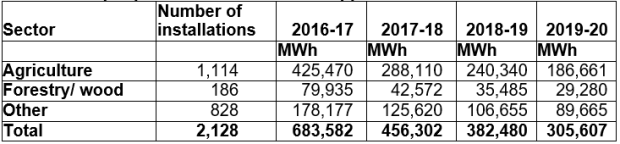

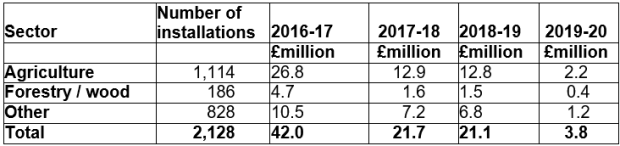

- The significant amendments to the tariffs from 1 April 2017 appears to have been a key factor in a substantial reduction in the overall heat generated under non- domestic RHI since 2016-17. The trend of the significant reduction in both heat output produced and the corresponding RHI payments has continued again in 2019-20 as outlined in Tables 2 and 3 below.

Table 2: Heat Output produced in MWh for all applicants

Source: Department Based on meter readings to May 2020

Table 3: Non – domestic RHI payments for all applicants

Source: Department

- I asked the Department to comment on this continued reduction in heat output and corresponding reduction in payments and the Department told me that the introduction of the tiered tariff on 1 April 2017 was a key control which significantly reduced the incentive to overproduce heat for the purpose of inflating the RHI payment. The current level of heat generated is now more in line with what was envisaged by the Department at the outset of the Scheme. In addition, the Department advised that many scheme participants can demonstrate different reasons for the change in the level of heat generated. Such reasons include better energy efficiency; a corresponding decrease in production; changes made to production methods; or a supplementing of the level of heat produced, using non-biomass sources.

Inspections

- I have previously reported on the need to take appropriate action where problems have been identified as a result of the inspections carried out by the Department. As at 31 March 2020, almost 750 sites (almost 70 per cent of installations) had been subject to a site visit or desk audit. Whilst progress has been made in carrying out these reviews, issues are still being identified such as the overproduction of heat and failure to provide accurate information regarding the heat use.

- I acknowledge that Covid-19 has caused the site inspections to stop for the foreseeable future and I asked the Department if it is still on course to complete the programme of site inspections and desk reviews before the end of June 2021.

- The Department told me the Inspection and Review Strategy for 2020-21 sets out how the 100% programme of inspections will be finalised through the completion of site visits, desk reviews or Ofgem business as usual (BAU) audits on all of the Non-domestic RHI installations not subject to inspection or desk review to date. The Department also told me that the Inspection and Review Strategy also outlines how, due to the commitment within the NDNA agreement concerning the future of the scheme, it is intended to have the whole process of inspections and compliance completed by the end of March 2021. To achieve this reduced timeframe, the Department plans to complete a site inspection or desk review on the remaining 238 sites (approx. 332 installations) within Phase 2 (year three) for review by the Compliance team by autumn 2020. Furthermore, it is planned all cases will be processed by Compliance and issued to Ofgem by 31 December 2020. Where instances of suspected misuse or fraud are detected, these will either be retained by the RHI Taskforce Compliance Team, or referred

to Ofgem to investigate and take enforcement action, as appropriate, in line with the Scheme Regulations.

- In order to meet this challenging target, the Department told me it is adopting a flexible approach to resourcing whereby administration teams are allocating staff to different areas within the work stream as required. Regular engagement with Ofgem and closer monitoring of Ofgem’s performance in line with agreed KPIs is being undertaken with the view to having all compliance/enforcement action completed for all remaining cases by 31 March 2021.

Judicial Review – RHI regulations

- As set out in note 18 to the accounts, there is currently a Judicial Review against the introduction of the 2019 amended RHI regulations and an appeal against the introduction of the 2017 Regulations. It is likely that these legal cases will continue for some time.

Overpayments

- Incorrect tariffs (due to rounding of annual inflationary uplifts) were applied to a number of the RHI technologies since April 2019, resulting in a total amount of

£40,000 being overpaid to some applicants. On the basis that the recipients could not be expected to know that they were being over paid and that any attempt to recoup the over payments would not be cost effective, the Department has sought and been granted approval from the Department of Finance to write off this overpayment.

Future of the Scheme

- I note the recent comments made by the NI Affairs Committee in the setting of future tariffs and that the Department recently published an independent report on hardship associated with RHI participation which will be considered as options are developed for the future of the scheme. In addition, consultation on the recent tariff review closed on 26 May 2020 with the Department currently analysing the responses.

- In light of the return of the NI Executive and the commitment within “New Decade, New Approach” to close the scheme, the Department has told me it is considering options on the future of the RHI Scheme, taking account of the key issues including legal risk, State aid, value for money, affordability and the impact on participants. I shall continue to monitor this situation.

Qualified audit opinion

- I am required under the Government Resources and Accounts Act (Northern Ireland) 2001 to report my opinion as to whether the financial statements give a true and fair view. I am also required to report my opinion on regularity, that is, whether in all material respects the expenditure and income have been applied to the purposes intended by the Northern Ireland Assembly and the financial transactions conform to the authorities which govern them.

- I have qualified my audit opinion again this year for the same reasons as the last four years:

- ongoing weaknesses in controls in the non-domestic RHI scheme; and

- expenditure incurred without the necessary approvals in place.

- While costs have again reduced in 2019-20 because of the introduction of the revised tariff in 2019, I was still unable to obtain sufficient evidence that the controls over the spending on the non-domestic RHI scheme were adequate to prevent or detect abuse of the scheme as issues are still being identified as part of the ongoing inspection process.

- I have also qualified my regularity audit opinion because of a lack of required approvals being received by the Department in relation to a proportion of the spending on the non-domestic RHI scheme. At the commencement of the scheme in November 2012, the Department of Finance and Personnel (DFP – now the Department of Finance (DoF)) had given approval for expenditure under the scheme up to 31 March 2015. DETI (DfE was previously known as DETI) was due to seek re-approval of the scheme from DFP from 1 April 2015 but this was overlooked and DFP approval was not granted until 29 October 2015.

- During this seven-month period in 2015-16, there were 788 boiler applications to the scheme, out of a total of 2,128 boiler applications (37 per cent). The ongoing costs incurred during 2019-20 in relation to these 788 applications amounted to

£0.74 million (£8.1 million in 2018-19) and as stated above, because these applications were accepted onto the scheme by DETI during a period in which there was no DFP approval, the total expenditure in relation to them continues to be irregular. To date, the Department has not formally sought specific retrospective approval for these 788 applications, but will consider it following the implementation of the long term tariff structure.

Payments to North South bodies

- I have again qualified my regularity opinion in relation to expenditure in 2019-20 of £12.3 million to Tourism Ireland Limited and £3.2 million to InterTradeIreland (total of £15.5 million (2018-19 - £18 million)). Whilst a Minister was in post from January 2020, it was not possible to secure North South Ministerial Council (NSMC) approval for the 2019 and 2020 Business Plans for these two North/South bodies. While DoF has agreed that these payments are legal in the absence of approved Business Plans, I have decided to qualify my regularity opinion as the expenditure has been incurred without the necessary approvals in place.

Small Business Grant Scheme

- In response to the unprecedented and significant impact of the Covid-19 crisis on the Northern Ireland economy and on businesses and their employees, the Small Business Grant Scheme was launched by the Department on 26 March 2020. This was an NI Executive initiative to provide one-off emergency grants of

£10,000 to small businesses to help mitigate the potential threat of business closures.

- The scheme is one of three schemes that are focused on supporting various types of businesses during the impact of Covid-19 – the other two schemes being: the Business Support Grant for the Retail, Hospitality, Tourism and Leisure Sectors and the Micro-Business Hardship Fund. Payments on the Small Business Grant Scheme occur in both the 2019-20 and 2020-21 financial years. In 2019-20, funding for payments of £67.7 million was provided by the Department in the form of cash-based Grant in Aid which appears as Programme Costs in its 2019-20 accounts, with the payments being administered by Land and Property Service (LPS). Expenditure of £220 million for the total scheme appears on an accruals basis in Invest NI’s 2019-20 accounts. Payments on the other two schemes occur in the 2020-21 year only and are not considered here.

- The scheme was required to be designed and delivered by the Department and LPS at a rapid pace and it was in recognition of these particular circumstances that it was subject to a Direction from the Economy Minister. As part of the submission to the Economy Minister, the Department highlighted a number of risks due to the nature of the scheme and the pace with which it was being delivered.

- In order to deliver this emergency grant, the Department agreed a Memorandum of Understanding (MoU) with Invest NI and the Department of Finance (DoF) / LPS. Under the terms of the MoU:

- Invest NI’s limited responsibility was to record the full estimated costs of the grant scheme on an accruals basis in 2019-20 budgets and accounts. Essentially, as Invest NI has the authority to provide grant funding to businesses, the Department acted as an agent for Invest NI to make the payments. Invest NI was not directly involved in determining the amounts payable or making the payments to the organisations;

- The Department assumed responsibility on behalf of the Executive for the scheme, including any potential error, fraud or losses arising from the administration of the scheme; and

- DoF (via LPS) was responsible for the identification and checking of eligible businesses and making the payments to those businesses. LPS’s data on ratepayers was used to determine who was eligible to receive the grant, however, I note that this was not the normal intended purpose of the LPS information. This brought some risk, but was a pragmatic approach in the absence of any better information.

- As part of their review of the scheme, LPS identified ineligible payments totalling

£3.74 million. As part of my audit, on a sample basis, my staff reviewed the payments made by LPS in respect of the total scheme and identified ineligible payments, some of which were already included in LPS’s list of ineligible payments (identified through internal control procedures) and one which was initially not included. The ineligible payments identified by my staff, if extrapolated across the total scheme, indicates the potential of up to £13.5 million ineligible payments, which I consider to be material in the context of the scheme payments. As payments by the Department for the scheme are split across two financial

years, £4.2 million of this £13.5 million relates to 2019-20 and the remainder relates to the 2020-21 financial year.

- One of the conditions of entitlement to the scheme was that businesses had to be trading at 15 March 2020. My staff identified errors where businesses were not trading from that particular property on which the grant was eligible and were therefore not entitled to receive the grant, despite in most cases completing an on line declaration. The Department told me that one assumption was that a ‘live occupancy’ for rating purposes indicated that a business was trading from the address, the assumption being that a business would not willingly pay full occupied rates for premises it was not occupying. The businesses had not therefore identified this fact to LPS at the point at which the grant payments were issued. I also note that LPS has identified other types of error that they are currently reviewing, such as landlords receiving payment instead of the tenant and duplicate payments made.

- As these payments have been paid to participants who were not eligible under the Scheme, they are irregular and as the Department is responsible for the scheme, I have qualified my regularity opinion as the expenditure does not conform to the authorities which govern it. This qualification also applies to Invest NI who were responsible for recording the costs of the scheme and I shall consider what implications this has on my audit of LPS financial statements in due course.

- I also note that DfE is currently working on a recovery process, with assistance from LPS, to clawback any grant that was paid to those not eligible. At the time of this report, 374 payments were being reviewed for possible recovery. I asked the Department for an update on the recovery of these payments and it told me that to date 62 payments have been recovered, 60 repaid in full, and 2 partial repayments.

- Given the risks involved in setting up this scheme so quickly in exceptional times, I asked the Department what controls and procedures it had in place to ensure expenditure on the scheme was eligible and whether any lessons had been learned in administering this scheme. The Department told me a memorandum of understanding was signed between DfE and DoF/LPS on 22 April 2020. LPS informed the Department that a master dataset of all eligible ratepayers was created, which embedded a comprehensive set of validations and controls for managing ratepayer and property data and IDs, portal data, applicant bank account, and e-mail validations and controls. In addition, eligibility criteria was developed by DfE, and corresponding grant processing and review procedures were put in place by LPS. The Department is currently in the process of developing a lessons learned report covering the three business grant schemes.

- The Department is commissioning research on the impact of its Covid-19 interventions in order to provide useful information on judging the impact and value for money of this scheme along with the Business Support Grant for the Retail, Hospitality, Tourism and Leisure Sectors and the Micro-Business Hardship Fund. I look forward to the outcome of this work and I will review the other two schemes as part of my 2020-21 audit at which point I may report further.

Presbyterian Mutual Society

- The Presbyterian Mutual Society (PMS) went into administration at the height of the financial crisis in 2008. In total £225m of loans were made by the former Department of Enterprise (DETI) to bail out PMS. Of this amount, £50 million, is at the end of the list of creditor priorities and is unlikely to be repaid. The remaining £175 million is being repaid through annual instalments over 10 years and the original agreement outlined that this was due to be settled in full by November 2020, facilitated through the sale of the PMS loan book, WIP and Investment property assets. The investment property assets mainly consist of retail sites and offices predominantly located in the north of England and in Scotland.

- At 31 March 2020, the total amount to be repaid is £78 million, however, I note the impact of Covid-19 has resulted in the planned exit sales strategy being seriously affected and that the Department is reviewing options, one of which may include a possible extension to the loan facility. I note that the Department is working closely with the Joint Supervisors and its advisors to establish the best way forward to ensure full recovery of the loan and notes 11 and 18 in the accounts refer to this. I have also included an emphasis of matter paragraph in my audit certificate in relation to this matter. I shall continue to closely monitor progress and may report on this matter in the future.

HMS Caroline

- HMS Caroline is the last survivor of the First World War British Grand Fleet and of the Battle of Jutland and has been docked in Belfast since the 1920’s. In October 2012 it was announced that the ship would remain in Belfast following the signing of a legal agreement with National Museum of the Royal Navy (NMRN), which outlined that DETI would be responsible to repair and maintain the ship.

- The restoration of HMS Caroline was originally intended to be delivered by 31 May 2016 to coincide with the Centenary of the Battle of Jutland. While the Ship was ready to stage the Centenary Event, the project experienced a number of significant challenges:

- agreeing and finalising lease arrangements between the Belfast Harbour Commissioners and the Northern Ireland Science Park. The issues with the leases were eventually resolved in November/December 2016 (almost two years later than originally anticipated); and

- changes in scope, which resulted in the project costs increasing by £4.3 million from the original estimated capital cost of the restoration of £14.4 million to £18.7million.

- Heritage Lottery Funding of £14.2 million has been secured to deliver the project and Tourism NI agreed to fund the remaining £4.5 million, which included £1.4 million directly attributable to delays in the project.

- The project has taken two years longer to deliver than was initially expected, mainly due to the difficulties in securing the lease arrangements which took substantially longer than expected. HMS Caroline first opened to the public on 1 June 2016 and in October 2016, it was moved from Alexandra Dock to Harland & Wolff’s ship repair dock for further restoration works. In July 2017, HMS Caroline re-opened to the public and following all major works completed, the official opening of HMS Caroline took place in April 2018. However, the Ship closed on 17 March 2020 due to Covid-19 restrictions.

- The legal agreement signed in 2012, outlined that DfE should take all reasonable and proper care of the ship and procure that the ship is made available for access by the public. Should the agreement be terminated the department is responsible for the costs of transporting the ship to Portsmouth. A further operating agreement was signed in 2017 which set out the operating arrangements. This expired on 30 June 2020. In the 2016, it was agreed that an endowment fund be created to ensure the long term financial viability of HMS Caroline.

- Whilst an endowment fund was considered, it never materialised due to the complex nature of such a fund. The key financial responsibility is that the Department is liable to fund any shortfalls should they arise in line with the agreements and with a deficit being incurred earlier than anticipated, mainly due to lower visitor numbers, the Department has incurred an additional £1.4 million of costs up to 2019-20.

- A permanent Operator solution needs to be found for the ship. NMRN are currently operating the ship in an interim arrangement, however, I note the Department’s comments in its Governance Statement and its intention to develop a revised operating agreement to include more robust controls, KPIs and funding mechanisms and I will continue to monitor progress on this issue.

Conclusion

- The Department continues to address issues arising from my previous reports on the non-domestic RHI scheme, but significant challenges remain in finalising the inspection process and closing the scheme in a cost effective way. I will continue to monitor the results of the ongoing inspection process and any further actions taken by the Department to address the concerns I have previously raised.

- I shall also continue to monitor how the Department addresses the other issues highlighted in my report concerning payments to the North/South Bodies, the Small Business Grant Scheme, Presbyterian Mutual Society and HMS Caroline.

KJ Donnelly

Comptroller and Auditor General

Northern Ireland Audit Office

106 University Street

September 2020

Belfast

BT 7 1EU