Performance Report

27 Public Reports:

- 7 Value for Money Reports

- 1 Impact Report

- 1 General Report

- 1 Good Practice Guide

- 12 Local Government Reports

- 5 Other Reports

£65.6 Million in savings for the taxpayer.

National Fraud initiative co-ordinated in Northern Ireland.

Prompt Payment of suppliers:

- 97.5% within 30 days

- 84.9% within 10 days.

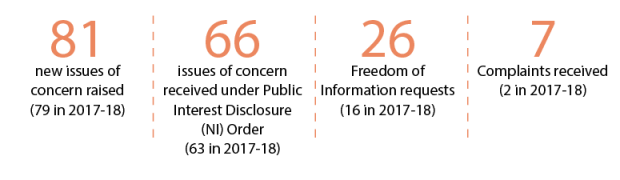

66 issues raised by whistleblowers.

15 MLA queries dealt with.

151 Accounts Audited:

- 136 Central Government

- 15 Local Government.

OVERVIEW

The purpose of this overview is to provide a short summary of the Northern Ireland Audit Office’s structure, purpose and performance during the year. It also sets out the key risks to the achievement of our objectives, providing sufficient information for users to form a high level understanding of our organisation and its performance.

Chairperson’s Statement

In December 2018 I was delighted to join the Northern Ireland Audit Office (NIAO) as the new Chairperson of the Advisory Board. With a long career in PwC, I came to the NIAO already with an appreciation of the work of the Office, having fulfilled a range of roles as external auditor, internal auditor, risk and governance advisor and also following many years of working in contractual partnership on the completion of public sector audits. The role of the Advisory Board is to provide objective and impartial advice to the Comptroller and Auditor General (C&AG) and to assist him in the discharge of his functions. In my role as Chair, I intend to bring independence of thought, informed by the knowledge and experience I have gained outside the NIAO.

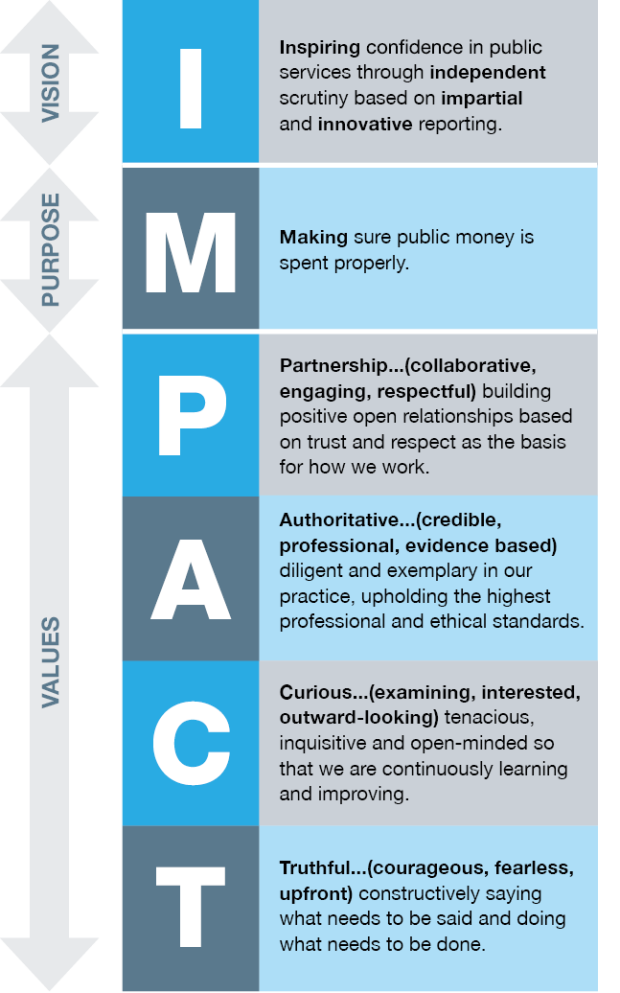

When appointed, I was very quickly struck by the vibrancy and appetite that exists within the NIAO to make an impact in the public sector, driven by the new Vision, Purpose and Values Statement. This is an exciting time for the NIAO with the recent launch of the Business Transformation Programme and the three year Strategic Corporate Framework underpinning the Office’s longstanding desire to deliver for the taxpayer.

In my new role, I have an opportunity to share my experience and help harness this energy and fresh confidence in the Office. I am impressed with what I have seen to date – the values, which embrace partnership, curiosity, courage, and upholding the highest professional and ethical standards, promote the right message for an organisation to which I am proud to be appointed as its Chairperson. Recently I have been joined on the Board by three new non-executive members, Noel Hyndman, Marie Mallon and John Turkington. With their collective talents, I am confident we can support and advise the Comptroller and Auditor General and his staff as the Office progresses its three corporate strategic priorities and makes real collaborative impact to the benefit of citizens and public services in Northern Ireland.

Martin Pitt

Chairman

26 June 2019

Comptroller and Auditor General’s Statement

2018-19 has been a challenging, yet rewarding, year for the Northern Ireland Audit Office (NIAO). We have published reports which are topical, timely and provide added value to the wider public sector. For example, our report on the preparedness of Northern Ireland for exit from the EU, which was produced over a short number of weeks and was well received by our stakeholders. Our public reports have been delivered against a backdrop of political paralysis, as the NI Assembly has not sat since early 2017, a Parliament which has been dominated by Brexit, and the ongoing public inquiry into the Renewable Heat Incentive Scheme, which continues to loom large over the public sector, its culture, and how it will operate in the future.

We have a public service with unacceptably long waiting lists in health, schools under severe budgetary pressures and a public sector in need of radical transformation and reform. In this arena, we continue to play a pivotal role in helping to build a modern, high performing public service that is accountable to taxpayers and citizens.

The accountancy and audit world is in a state of flux. Following the collapse of Carillion, and the Kingman Review, it has been recommended to government that the Financial Reporting Council should be replaced with a new independent regulator with clear statutory powers and objectives. In February, Sir Donald Brydon was appointed by the Secretary of State for Business, Energy and Industrial Strategy to review the quality and effectiveness of audit. I welcome these reviews and see them as opportunities to further strengthen public audit and the work of my Office over the next number of years.

My Office is transforming to meet emerging challenges. I have initiated a Business Transformation Programme to ensure that I continue to have a highly skilled and motivated workforce, that our working practices are modern and that we continue to operate in an innovative and vibrant working environment. I have also established a Future and Quality of Audit working group to address the recent reviews and their implications, and to ensure that we meet the quality requirements for our audits.

In financial audit, we have established new long-term contractual arrangements with our private sector partners.

We also need to ensure that, moving forward, digital technology is embedded into our working methods and systems. I am delighted we have been successful in securing funding from Govtech Catalyst, a fund launched by the Cabinet Office to help the public sector identify and work with cutting edge technology firms to find innovative solutions to operational service and policy delivery challenges.

Our achievements in 2018-19 have been wide-ranging. We have delivered the audit of 151 accounts from across the central and local government sectors and produced 27 public reports covering the findings of our financial audit work, value for money examinations in areas such as health, education, agriculture, social welfare and justice, a good practice guide on Performance Management for Outcomes, and Local Government Annual Improvement Reports for councils.

We have a responsibility to provide value for money on the services we deliver for our stakeholders, and a key measure we use is the savings to the public purse resulting from our work. Exceptional savings of £65.6 million were achieved in 2018-19. Our achievements have been secured against a backdrop of real cost reductions of 24.5 per cent over the past 5 years, and considerable change in our internal operations. Change has included the introduction of a new governance model to better meet the needs of the Office. I am grateful to the previous non-executive members for their service to public audit and contribution to the NIAO. I recently welcomed the new non-executives, led by our Board Chair, Martin Pitt. I am delighted with the considerable experience and foresight they bring to the table.

I wish to thank all my staff for their contribution to the successful outcomes in 2018-19. As I have stated previously, the skills and experience of our people underpin the provision of the professional cost-effective service that we provide. I am committed to ensuring that all my staff remain highly skilled, motivated and flexible to be well placed to handle the challenges ahead and ensure the NIAO remains a professional, effective public audit function, standing ready to fully deliver in a functioning political environment and inspiring confidence in public services through impartial and innovative reporting.

Kieran Donnelly

Comptroller and Auditor General for Northern Ireland

26 June 2019

Purpose and activities of the NIAO

Our role

The Northern Ireland Audit Office (“the NIAO” or “the Office”), established in 1987, has a pivotal role in helping to build a modern, high performing public service that is accountable to taxpayers and citizens. We do this by providing objective information, advice and assurance on how public funds have been used and accounted for, and encouraging best standards in financial management, good governance and propriety in the conduct of public business.

Our vision, purpose and values

Our strategic priorities

Further information is set out on page 26.

Our independence

The head of the NIAO, the Comptroller and Auditor General (“the C&AG”), is an Officer of the Northern Ireland Assembly (“the Assembly”) and a Crown appointment made on the nomination of the Assembly. Under the Audit (Northern Ireland) Order 1987, the holder of the office is a corporation sole, and responsible for the appointment of NIAO staff who assist him in the delivery of his statutory functions. The C&AG and the NIAO are totally independent of government.

Our accountability

The NIAO and the Audit Committee of the Assembly, which oversees NIAO performance, have agreed a Memorandum of Understanding on the governance and accountability of the Office. The Memorandum (available at www.niassembly.gov.uk/) sets out:

- the values and standards of the NIAO in carrying out its work;

- the internal governance arrangements of the NIAO and, in doing so, provides confidence to the Assembly and wider public regarding the arrangements for the governance and accountability of the NIAO; and

- the commitments of the C&AG and the NIAO to the Assembly Audit Committee on the actions they will take to uphold transparency and manage public money effectively.

Key issues and risks

A number of challenges and developments in our operating environment are summarised as follows:

Digitalisation

- The public sector has strengthened its digital delivery and access to on-line government services.

- We continue to develop our skills and capabilities to audit digital systems.

- In September 2018, we were successful in applying for £1.25m of funding from Gov Tech Catalyst for a data analytics project challenging private sector firms to develop a data enabled public sector audit approach.

- Audit in the digital era forms a key strand in our Digital Services Strategy.

Budgetary Constraints

- The public sector continues to face significant budgetary pressures.

- Our annual net resource outturn has decreased by 19.8%1 (25.4% in real terms) in the last five years.

- Savings have been achieved primarily through natural wastage and the implementation of a staff Voluntary Exit Scheme (VES).

Resourcing

- Full Time Equivalent staff numbers have fallen by 3 (3%), from a total of 102 in 2017-18 to 99 in 2018-19.

- FTE numbers have fallen by 41 (29%) from 140 in 2011-12 to 99 at 31 March 2019.

- In the four years to 31 March 2019, voluntary exits resulted in the departure of 37 permanent members of staff (33.4 FTE).

- Our focus has been to rationalise management and bolster front-line resources.

- A loss of valuable experience has placed greater emphasis on training needs. Six additional graduate trainees have been recruited in-year.

Governance Structure

- A new governance structure has been introduced and new non-executive members appointed.

- An Advisory Board has been introduced to provide objective and impartial advice to the C&AG and to assist him in the discharge of his functions.

- To provide support in these functions, the Board has an Audit and Risk Assurance Committee to review the comprehensiveness of assurances on systems of internal control, risk management and corporate governance.

Brexit

- The implications of Brexit for the planning and delivery of services across the Northern Ireland public sector are unprecedented.

- Uncertainty remains around the outworking of the process and what its impact will be on government reform.

PERFORMANCE ANALYSIS

Our performance

The NIAO Strategic Corporate Framework 2018-21 (available at www.niauditoffice.gov.uk), sets out the Office’s role, strategic priorities and impact indicators. It also examines the funding required to achieve these.

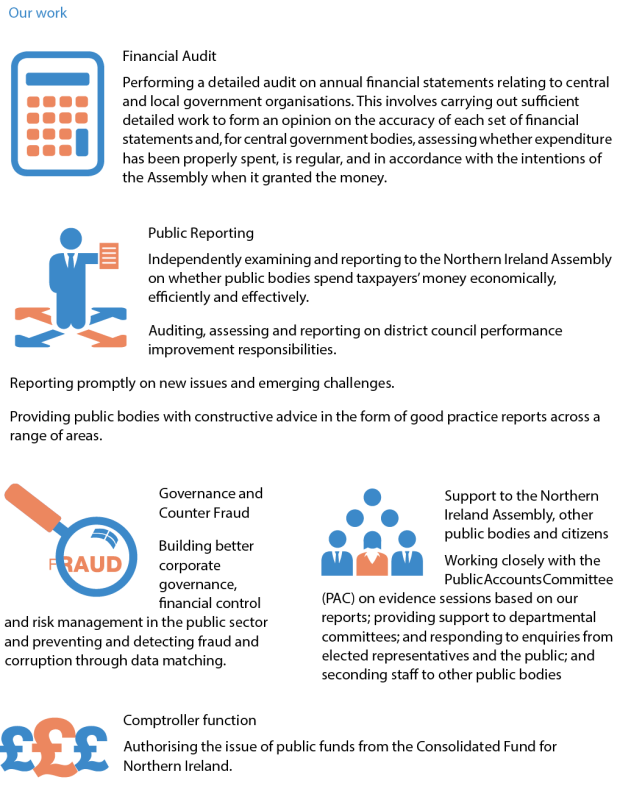

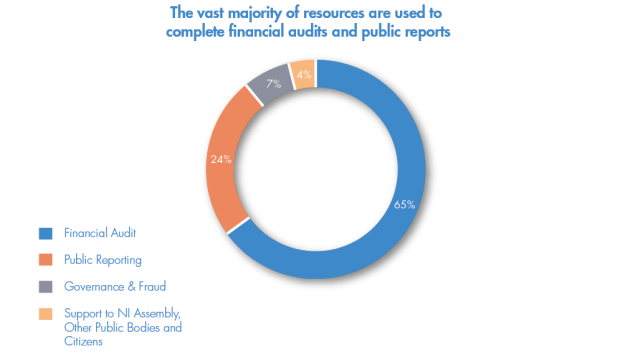

Financial audit

Financial audit work undertaken by the Office comprises the audit of central and local government accounts:

Central government

The C&AG has a statutory responsibility to audit the financial statements of all Northern Ireland departments, executive agencies and other central government bodies, including non-departmental public bodies, health and social care bodies and some public sector companies, and to report the results to the Assembly.

The purpose of our financial audit is to provide independent assurance that the accounts of an audited body give a true and fair view of its financial position, have been prepared in accordance with the relevant accounting requirements and that the transactions underlying the financial statements are in line with the intentions of the Assembly and other authorities.

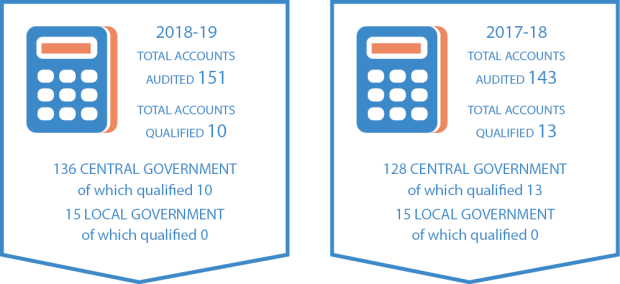

In 2018-19, we certified 136 central government accounts (2017-18; 128). The increase in the number of accounts certified is as a result of the certification of a number of outstanding accounts from previous years (nine 2016-17 and one backlog) and a decrease in the number of accounts not yet certified at year end.

For the audit of central government bodies there is an explicit requirement for the auditor to provide an additional audit opinion on whether, in all material respects, expenditure and income have been applied for the purposes intended by the Assembly and conform to the authorities which govern them; a regularity opinion.

If at the end of an audit we consider that the accounts do not present a true and fair view, that expenditure and income have not been incurred in line with Assembly intentions, nor conform to the authorities which govern them, then the C&AG will qualify his opinions on the accounts. Ten central government accounts were qualified in 2018-19 (2017-18; 13). Of the 10, seven were qualified solely on the basis of the regularity opinion. In these cases, and in other cases where there are significant issues arising, we make a report to the Assembly which may be considered by the PAC.

We inform the organisations we audit of the issues we find during our work, giving our independent view on areas where the audited body could improve its governance, controls and financial management. We liaise with management to obtain their response to the issues identified.

During 2018-19 we continued to work with the Office of the Comptroller and Auditor General in Dublin on the shared audit and certification of North South bodies. We also continued to have close working arrangements with the National Audit Office for the accounts we audit on its behalf. This is a significant workload and includes audits of the European Agricultural Funds, lottery and whole of government accounts.

Local Government

A senior member of NIAO staff is designated by the Department for Communities, with the consent of the C&AG, as the Local Government Auditor. This role is undertaken by the Office’s Chief Operating Officer, Pamela McCreedy. The Local Government Auditor, assisted by NIAO staff, is responsible for the audit of local government bodies. In 2018-19 we completed the audits of 15 local government accounts (2017-18; 15). None of the opinions on the local government accounts certified in 2018-19 were qualified (2017-18; nil).

Public Reporting

The Office produces a wide range of public reports each year, reflecting its broad audit remit.

The reports completed in 2018-19 are shown below. Copies of the full reports can be obtained from our website at www.niauditoffice.gov.uk.

Value for Money

Structural Maintenance of the Road Network

Welfare Reforms in Northern Ireland

The Social Investment Fund

The UK Border: how prepared is Northern Ireland for exiting the EU?

The Financial Health of Schools

Firearms Licensing in Northern Ireland

National Fraud Initiative 2016-17

Impacts Report

Eradicating Bovine Tuberculosis in Northern Ireland

General Report

General Report on the Health and Social Care Sector

Good Practice Guide

Performance Management for Outcomes

Local Government Reports

Local Government Auditor’s Report 2018

11 Local Government Annual Improvement Reports 2019 (one per Council)

Other Reports

Agri-Food and Biosciences Institute 2016-17

Agri-Food and Biosciences Institute 2017-18

Legal Services Agency (NI) Account 2017-18

Department for the Economy Resource Account 2017-18

Education Authority Annual Report and Accounts 2016-17

Value for Money Reports

Our examinations into economy, efficiency and effectiveness (value for money) consider how public bodies use their resources. Our value for money work is informed by a careful analysis of the audit field. We select a balanced programme of studies which aims to:

- provide the Assembly with independent information and advice about how economically, efficiently and effectively departments, agencies and other public bodies have used their resources;

- encourage audited bodies to improve their performance in achieving value for money and implementing policy; and

- identify good practice and suggest ways in which public services could be improved.

Our value for money studies focus on specific areas of government expenditure and seek to make a judgement on how well resources have been managed and services delivered. In 2018-19, these covered a range of topics across the Northern Ireland public sector in areas such as health, education, agriculture, social welfare and justice. In these reports, we sought to measure performance; identify the factors underlying that performance; and offer practical recommendations aimed at adding value.

Examples of our value for money reports include the following:

The Social Investment Fund (SIF)

Background

At the time of our report, SIF had awarded funding of £79 million to 68 projects across Northern Ireland. This was initially intended to be spent in the three years to March 2015. However delivery of many of these projects has been delayed and the SIF delivery period was extended to 2019-20. The SIF budget was also increased by over £13 million.

Report Findings

The report identified a number of serious concerns, including: conflicts of interest which were not always appropriately dealt with; documentation around project selection and prioritisation was poor and the scheme did not operate transparently; governance arrangements were initially poor; and project delivery targets were overly ambitious.

The Financial Health of Schools

Background

This report examined the extent to which schools have been able to manage within their delegated budget for the period 2012-13 to 2016-17 and whether schools’ surpluses or deficits are within the limits set by the Education Authority (EA).

Report Findings

The report found that there had been a 9.3 per cent reduction in the General Schools Budget between 2012-13 and 2016-17.

At 31 March 2017, almost 46 per cent of Controlled and Maintained schools had accumulated surpluses, whilst 16 per cent had accumulated deficits, which were in excess of EA’s prescribed thresholds. Seven post-primary schools had a deficit in excess of £1 million at 31 March 2017. The report concluded that the system is coming close to a tipping point and action needs to be taken.

Welfare Reforms in Northern Ireland

Background

The Report examined the key changes to benefit rates and entitlements; looked at Personal Independence Payment and Universal Credit; highlighted the issues which emerged from our engagement with the Third Sector; and dealt with expenditure, outcomes measurement and the impact on social housing providers, particularly NIHE.

Report Findings

The report highlighted the decision by the Northern Ireland Executive to fund a mitigation package of £0.5 billion to “top-up” reductions in benefit payments for the four years ending March 2020 and noted that the uptake on mitigation payments was below estimates, with £136 million of available funding not utilised in the first two years.

The full impact of welfare reforms has not yet been felt in Northern Ireland, and some claimants may face significant hardships when current mitigation measures come to an end in March 2020.

Impact Reports

An impact report on Eradicating Bovine Tuberculosis in Northern Ireland was published in November 2018 which examined the escalating costs of the programme and the continued prevalence of the disease, and outlined the Department of Agriculture, Environment and Rural Affairs’ proposals to adopt a new strategic approach to control, and ultimately eradicate, the disease.

General Reports

In December 2018, we published a General Report on the Health and Social Care sector. This report reviewed several key areas, including the financial performance of HSC Trusts; timely access to hospital care; the Business Services Transformation Programme (BSTP); and consultancy payments made on a waiting times initiative.

Good Practice Guides

A good practice guide on “Performance Management for Outcomes”, was published in June 2018 to help public bodies implement the move to an outcomes based approach, as recommended by the Organisation for Economic Co-operation and Development (OECD) report, in its assessment of public sector reform agenda, published in 2016. This guide was launched at an event sponsored by the Chief Executives’ Forum.

Local Government Reports

Under the Local Government Act (Northern Ireland) 2014, there is a statutory duty to publish a Local Government Annual Improvement Report for each council. The purpose of these reports is to identify if councils have discharged their duties in relation to improvement planning and if they are likely to comply with the requirement to make arrangements to secure continuous improvement in the exercise of their respective duties.

The Local Government Auditor published an annual report on the exercise of her functions in September 2018 which commented on a range of topics arising from her audit work.

Other Reports

Six other reports were also published during the year that had arisen as a result of findings from financial auditing.

Governance and fraud prevention and detection

We work closely with audited bodies to promote good practice in governance arrangements and help combat fraud. Good governance structures which are well embedded in organisations are a key attribute to achieving corporate goals and are crucial, particularly in times of financial constraint. During this financial year we attended the audit committees of most of our audited bodies, providing support, advice and guidance to both non-executives and senior staff.

We continued to be involved in providing training to both staff and non-executives of audited bodies through programmes developed by the Chief Executives’ Forum. These programmes focussed on accountability and governance and were aimed at a number of different groups including Accounting Officers, senior managers, Board members and Audit Committee members.

We continue to support public sector bodies as they maintain their fight against fraud. Budgetary pressures remain a reality so it is essential that public bodies use all means at their disposal to prevent and detect misuse of public funds. Only in this way can frontline resources be maximised. We maintain a small counter fraud unit which provides support, advice and guidance on fraud related matters to public sector organisations.

A key focus continues to be the prevention and detection of fraud and error through data matching. Data matching involves comparing pieces of data or information held by one organisation against other records held by the same or another organisation, in order to highlight potentially fraudulent claims and payments.

Since 2008 we have co-ordinated the Northern Ireland public sector’s participation in the National Fraud Initiative (NFI), a UK wide data matching initiative to combat fraud and error, which runs every two years. We reported on the fifth exercise on 19 June 2018. To date in Northern Ireland, almost £35 million of fraud and error has been identified. The next data matching exercise is ongoing and will be reported on in June 2020.

We continue to promote the use of real time data matching under the NFI in order to prevent fraud and error entering the system and a small number of organisations are exploring this option.

Support to the Northern Ireland Assembly and the public

We will provide a sitting Assembly with independent support to enable it to hold the Executive to account for its financial management and the value for money it provides to the taxpayer for the public funds it spends. Our main engagement is through the support we provide to the Public Accounts Committee (PAC). We present our reports to the Assembly and the majority of these are considered by the PAC at hearings in which it takes evidence from the senior departmental officials involved.

Following consideration of the evidence, the PAC publishes its own report and recommendations to the Assembly. The Executive is then required to respond to these recommendations, specifying the action the audited body intends to take. We monitor the action taken and may revisit an issue where we consider that insufficient progress has been made.

However, since January 2017 no Assembly has sat. As a direct result, there has been no PAC to consider our reports and make recommendations to the Assembly.

To address this loss of accountability, it was agreed with the Secretary of State for Northern Ireland that all NIAO reports produced should be shared with her Office upon publication. For each of these reports, she obtains a departmental response from the relevant Northern Ireland department, submitted via the Department of Finance, which is placed in the Libraries of both Houses of Parliament once the response is prepared. This process was applied to our value for money publications in 2018-19.

Responding to Citizens

We continue to receive enquiries from a wide range of people about the bodies we audit. Where appropriate, we may carry out further audit work in response.

Stakeholder Engagement

Under the NIAO stakeholder engagement framework, we are committed to open, two-way communication that involves us listening to our stakeholders; keeping them informed; and being clear about how their contributions are being used. Maintaining our independence and impartiality is important, so it is not about agreeing with stakeholders. However, it involves recognising and understanding stakeholders’ individual values, beliefs, perceptions and ideas. We will continue to build on stakeholder relationships, resulting in real dialogue and interaction. The framework supports staff throughout our Office in planning, designing, undertaking and evaluating stakeholder engagement activities, and is linked to our key strategic priorities.

As part of the engagement process, we have conducted an influence/awareness exercise to determine our current awareness levels with our key stakeholders vis-à-vis where we aspire to be. The framework supports staff throughout our Office in planning, designing, undertaking and evaluating stakeholder engagement activities, and is linked to our key strategic priorities. As a result of this exercise, we have established and implemented a programme of engagement for each of them, which includes regular meetings with the Permanent Secretaries Group, meetings with departmental accounting officers, local council Chief Executives, departmental board and audit committee members, and annual meetings with local regulators and the community and voluntary sector.

The Office is active on Twitter (@NIAuditOffice). Our tweets continue to cover new reports and miscellaneous NIAO talks and presentations. We are exploring opportunities to expand our use of social media.

Impacts

We have a responsibility to achieve value for money on the services we provide to our stakeholders. One way in which we measure our success is by identifying the quantifiable financial impact of our work. In doing so, we recognise that our measurement of impact will only present a partial picture, as it is hard to quantify the deterrent effect of public audit in contributing to improved public services.

During 2018-19, quantitative financial impacts of £65.6 million were achieved as a result of the work of the Office and the PAC (2017-18: £50 million). This figure has been independently validated by the Office’s External Auditor and represents 9.5 times the net resource outturn of the Office (2017-18: 6.8 times).

The following examples demonstrate the main financial impacts achieved during 2018-19:

|

NIAO REPORT |

IMPACT |

|---|---|

|

Renewable Heat Incentive (RHI) - Our work identified the fact that the single tariff being paid to applicants to the scheme before November 2015 was in excess of the marginal cost to produce the heat and that it therefore incentivised those applicants to unnecessarily burn more fuel. We had a direct impact in reducing tariffs and also in changing the behaviour of applicants once our report was published. |

£30.8 million (cumulative impact of £63.7 million) |

|

Tackling Social Tenancy Fraud - Our 2013 report estimated that every social home recovered by local social housing providers through a proactive tenancy fraud detection programme would have the potential to save around £8,000 that would otherwise be paid out for private rented temporary accommodation. We agreed a proportionate share of the savings |

£776,000 |

|

General Report on Health & Social Care Sector 2012-13 and 2013-14 - As a result of our recommendations, a number of fraud investigations were undertaken, resulting in estimated annual savings of more than £3.5 million. We agreed a proportionate share of the savings. |

£1.43m |

|

Primary Care Prescribing – Following our 2014 report the HSC Board developed a prescribing efficiency plan for the primary care drugs budget. The HSC Board reported efficiency savings of £12.4 million. We agreed a proportionate share of the savings. |

£2.48m |

|

Collaborative Procurement Our 2012 report recognised that increasing collaborative procurement had the potential to generate financial savings without impacting on front line service delivery. As a result of improving procurement arrangements, total savings of almost £52 million were realised in 2018-19 following the award of the nine year Public Sector Network Contract. We agreed a proportionate share of the savings. |

£27.6m |

|

Reform of Legal Aid Remuneration for Legal Aid Providers Savings arising from the introduction of Crown Court Rules 2016 are forecast to save £5 million per year. Our report and PAC’s report contributed to this position and we have agreed a proportionate share of the savings. |

£2.5m |

|

TOTAL IMPACTS |

£65.6m |

The extent of savings achieved can fluctuate from year to year and is largely dependent on the nature of the studies undertaken in the value for money audit programme. Where our recommendations overlap with audited bodies’ own performance improvement work, we will consider the percentage share of the quantified financial impact that can be attributed to our influence.

Qualitative impacts of the audit function

Our Good Practice Guide on “Performance Management for Outcomes”, was published in June 2018 to help public bodies implement the move to an outcomes-based approach. Included with the guide was a “Performance Measurement Framework” and a “Good practice self-assessment toolkit” to facilitate this process.

We are members of a Review Group, led by the Department of Finance, which is examining the sponsorship arrangement for Arm’s Length Bodies. This is changing the emphasis to partnership working and follows on from our participation in an Innovation Lab to examine the arrangements and ensure the effective delivery of public services and improved outcomes

We have collaborated and participated with the “Strictly Boardroom” apprenticeship scheme, a training programme for those who want to serve on a board in the public and third sector.

We continue to collaborate with the Chief Executives’ Forum (CEF), an association of chief executive officers of civil and wider public service bodies in Northern Ireland, whose vision is to be recognised for the contribution it can make in building a better future for the people of Northern Ireland. Its strategic aims are to support the democratic process and the transformation of public services to better meet the needs of good government. As part of this collaboration, the Comptroller and Auditor General is a member and he has launched a number of his good practice guides at events sponsored by the Chief Executive’s Forum.

Performance measurement

In addition to measuring the financial impact of our audit work, we have a number of key performance measures to assist in demonstrating our productivity, quality of work and achievements in reducing costs. Performance achieved in 2018-19 against these key measures is as follows:

Key performance measures

Target: To deliver a comprehensive programme of work with reduced resources, maintaining high standards.

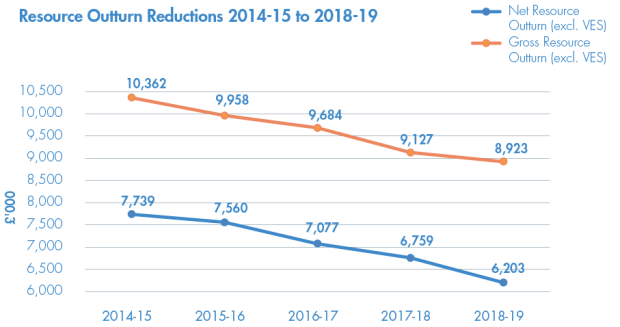

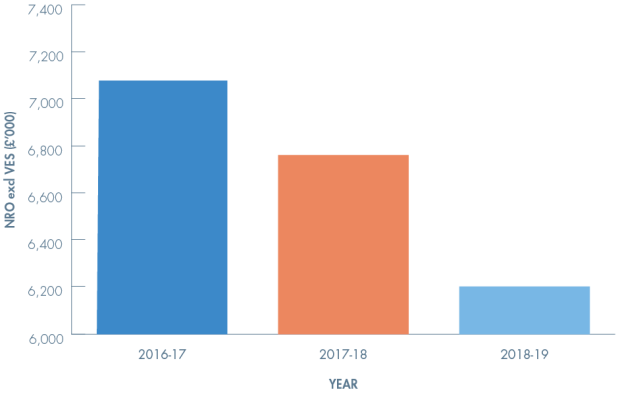

We delivered a range of audit outputs with a net resource outturn (excluding VES) that was 5.2 per cent lower in 2018-19 compared with 2017-18.

Target: To produce 33 public reports in 2018-19.

We achieved 27 reports, including five which arose as a result of findings from the financial audit process. A number of publications were delayed due to legal action and the need for legal advice.

Target: We subject our value for money reports to independent review by a panel of experts who rate the reports on a scale of one to five. We aim to ensure that our value for money reports maintain an average quality review score of at least three.

We achieved an average score of 3.4.

Target: To certify 150 accounts; 80 per cent of audited bodies within seven months and 100 per cent within twelve months.

We achieved certification of 141 accounts. In addition, 10 prior year accounts were certified in 2018-19, to total 151. Of the 141 accounts certified, 78 per cent of audits were delivered within seven months and 93 per cent within 12 months.

Target: Annual confirmation of compliance with the International Standard on Quality Control (ISQC 1), to ensure that our financial audit has complied with our audit methodology and professional auditing standards.

Eight accounts were reviewed by teams independent of the audit team. Five of the reviews were conducted by teams from the other UK public audit agencies.

Six of the eight audit opinions were found to be appropriate. Reviewers concluded that in two cases, there was insufficient evidence on file to support the audit opinion.

Resource Accounts 2018-19

Schedule 2 of the Audit (Northern Ireland) Order 1987 requires the NIAO to prepare resource accounts. Details of the Order can be found at www.legislation.gov.uk.

The financial statements on pages 71 to 89 have been prepared by us on a resource basis in accordance with the 2018-19 Government Financial Reporting Manual (FReM) issued by the Department of Finance.

NIAO Estimate

The Audit (Northern Ireland) Order 1987 requires the C&AG to prepare a Supply Estimate each financial year. Ordinarily, we present a draft estimate to the Assembly Audit Committee, established under Section 66 of the Northern Ireland Act 1998. In the continuing absence of an Executive and a sitting Assembly, the Northern Ireland Budget Act 2018 was progressed through Westminster, receiving Royal Assent on 20th July 2018, followed by the Northern Ireland Budget (Anticipation and Adjustments) Act 2019 which received Royal Assent on 15th March 2019. The authorisations, appropriations and limits in these Acts provide the authority for the 2018-19 financial year and a vote on account for the early months of the 2019-20 financial year, as if they were Acts of the Northern Ireland Assembly.

Resources

We have reduced our annual net resource outturn (costs) by 19.8 per cent (equating to 25.4 per cent in real terms) in the five years up to and including 2018-19, primarily through natural wastage and the implementation of a staff Voluntary Exit Scheme (VES).

The resources used by the Office in 2018-19 are set out in the following table:

|

Estimate (£’000) |

Outturn (£’000) |

Saving (£‘000)/(Excess) (%) |

||

|---|---|---|---|---|

|

Gross Resource Outturn |

9,864 |

9,651 |

213 |

2.2 |

|

Income |

2,720 |

2,720 |

- |

- |

|

Net Resource Outturn (NRO) |

7,144 |

6,931 |

213 |

3.0 |

|

Voluntary Exit Scheme (VES) |

730 |

728 |

2 |

0.3 |

|

NRO excluding VES |

6,414 |

6,203 |

211 |

3.3 |

|

Capital |

58 |

46 |

12 |

20.7 |

Savings arose from:

- a decrease to in-year salary costs arising from headcount reductions following a number of VES departures; and

- a reduction in the employee benefits liability.

These decreases were offset by an increase in contracted-out costs following a new five-year procurement exercise.

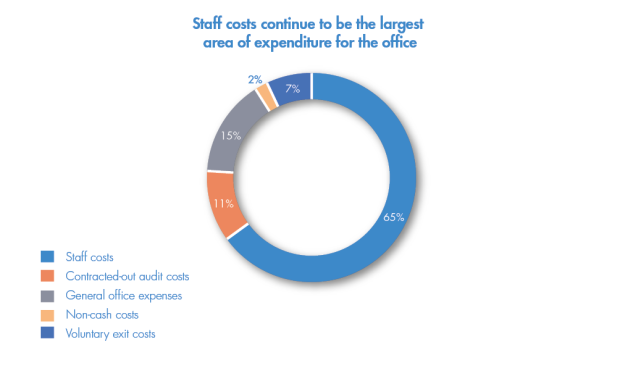

Staff costs continue to be the largest area of expenditure for the Office:

Resources were used as follows:

In addition to the above, the cost of administering the Comptroller Function was £14,000, as shown at Note 2 to the Financial Statements.

Income includes:

- fees received from:

- some central government bodies and North South bodies in respect of the audit of their accounts;

- the National Audit Office, for audits we carry out on its behalf;

- local government bodies, for the audit of their accounts and performance improvement;

- recoupment of salary and associated costs for seconded staff; and

- rental income from subletting areas of our building.

Each element of income, and the direct costs associated with it, is shown in the Accountability Report, at page 63.

Any income in excess of the Estimate must be submitted as Consolidated Fund Extra Receipts. In 2018-19, excess income of £60,443 was earned as a result of earlier than anticipated completion of chargeable audit work and income greater than that initially forecast in respect of European Agricultural Funds work.

Resources required in the future

The 2019-20 Budget has been maintained at the 2018-19 level in cash terms. In the absence of a sitting Assembly, the budget was approved by Parliament at Westminster through the Budget Act 2019. Allocated resources are shown in the following table:

|

2019-20 (£’000) |

|

|---|---|

|

Gross Resource Requirement |

9,995 |

|

Income |

2,700 |

|

Net Resource Requirement (NRR) |

7,295 |

|

GovTech Funding |

250 |

|

NRR excluding VES and Small Business Research Initiative |

7,045 |

|

Capital |

490 |

GovTech funding

Data Analytics is a fast developing area which will have an impact on the audit process in the future. In view of this, we have secured funding of £250,000 for 2019-20 through the Department for Business, Energy and Industrial Strategy. This funding will be directly allocated as grants to successful applicant organisations to conduct research in this area and to help develop new techniques or systems.

Re-developing our Office Accommodation

Our premises are to be redeveloped as part of a project to better utilise the space that we currently occupy. Additional capital expenditure has been included in the budget for 2019-20 to cover potential costs in the first full year of this project.

Reconciliation of Resource Expenditure between Estimates, Accounts and Budgets

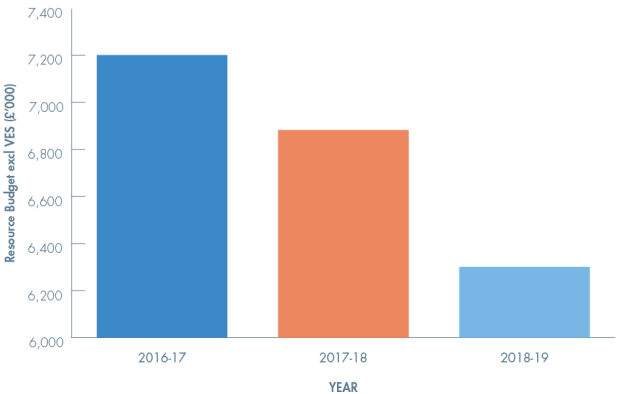

The Government Financial Reporting Manual requires a table showing a reconciliation, on an outturn basis, between the Net Resource Outturn, the Net Operating Cost and the Budget. This table is shown below:

|

2018-19 (£’000) |

2017-18 (£’000) |

|

|---|---|---|

|

Net Resource Outturn |

6,931 |

7,354 |

|

Consolidated Fund Extra Receipts |

(61) |

(30) |

|

Non-supply expenditure |

160 |

160 |

|

Net Operating Cost |

7,030 |

7,484 |

|

Consolidated Fund Extra Receipts |

- |

- |

|

Inter-departmental notional charge |

- |

- |

|

Resource Budget Outturn of which: |

7,030 |

7,484 |

|

Department Expenditure Limits (DEL) |

7,045 |

7,503 |

|

Annually Managed Expenditure (AME) |

(15) |

(19) |

Payment of Suppliers

The Office is committed to the prompt payment of bills for goods and services received, in accordance with the Better Payment Practice Code. Unless otherwise stated in the contract, payment is due within 30 days after delivery of the invoice or the goods and services, whichever is later.

During 2018-19, the Office paid 97.5 per cent of bills (2017-18; 98.7 per cent) within this standard.

In addition to this, the government has said that, wherever possible, public sector bodies should seek to pay suppliers within 10 working days of receipt of the invoice. In 2018-19, we met this standard for 84.9 per cent of invoices received (2017-18; 96.3 per cent).

Future development of the business

IMAGE PLACEHOLDER Figure_2

Our three strategic priorities for the period 2018-21 in our Corporate Strategic Framework are as follows:

1. In providing assurance, adding value and promoting excellence in public administration:

- We will continue to support effective democratic scrutiny by providing assurance to increase public confidence, especially during critical transitions in Northern Ireland government and public administration.

- We will promote and share good practice from the Northern Ireland public sector and elsewhere to stimulate improvement.

- Our audit work will help public sector leaders to gain assurance and improve economy, efficiency and effectiveness.

- We will expose corruption and malpractice that we identify and disseminate the lessons learned across our public services.

Why this is important: …significant transformation is anticipated over the next few years. Sharing good practice is a catalyst for improvement. Our role is to enhance public confidence in how Northern Ireland is governed, at the same time being diligent and exemplary in our own practice.

2. In supporting transformation in the public sector:

- Our public reports will take account of single and cross-cutting themes.

- Our outputs will be relevant and proportionate in relation to Northern Ireland public sector priorities.

- We will respond rapidly to emerging issues in a changing environment and to concerns raised by elected representatives.

- We will use our influence and strategic view to help public sector leaders deliver effective joined up government.

Why this is important: …we will focus on the issues that really matter to support clear accountability and value for money. Early intervention during the roll-out of government programmes will increase our relevance and impact, while minimising the negative impact of any poor practices before they have advanced too far. We will be proactive in supporting positive change and innovation across all parts of the public sector. Working across silos is a major barrier to the implementation of the Programme for Government so we will take a strategic view across departments to counteract this.

3. In transforming our business to meet the emerging challenges of the future:

- We will develop our internal capability through further investing in a highly skilled, motivated and versatile workforce.

- We will embed digital technology in working methods and systems across the NIAO.

- We will continue to modernise working practices to increase productivity.

- We will design and deliver an innovative and vibrant working environment, including modernising our accommodation.

Why this is important: …successful organisations help staff balance the demands of their work and their other life responsibilities; to remain relevant and sustainable we will continuously maximise the use of all our resources and provide our staff with the best support.

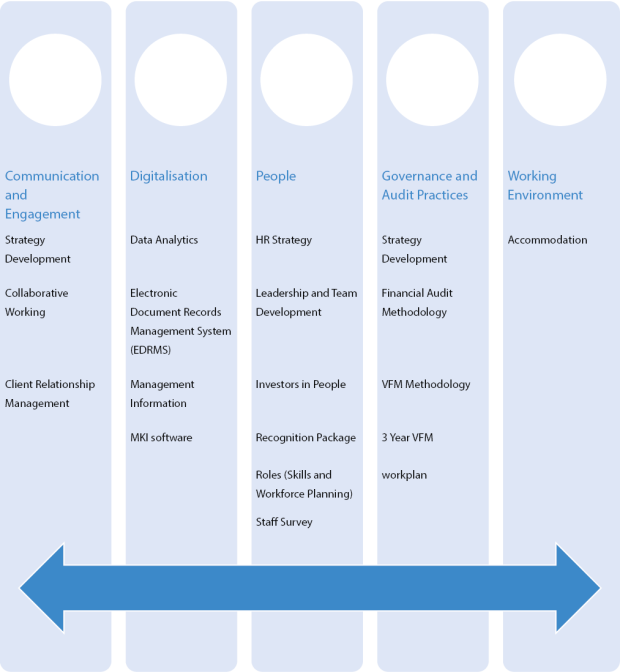

To deliver against each of our priorities, we have initiated a Business Transformation Programme. It will allow us to embed our VALUES and achieve an IMPACT in everything we do. It will ensure the delivery of high quality, efficient and effective services, internal and external, now and into the future.

NIAO transformation revolves around three key points of focus:

- Strategy

- People

- Service Delivery

Five pillars of transformation, each with associated work streams, have been identified. These are:

- Communication and Engagement

- Digitalisation

- People

- Governance and Audit Practice

- Working Environment

Progress with our Business Transformation Programme is being reported through Senior Management Team and Advisory Board.

Sustainability, environmental, social and community matters

We are committed to sustainable practice and minimising our impact on the environment. We meet these commitments by disposing of waste carefully, recycling appropriate materials, and by conserving the energy we consume. Locally, we have removed individual waste paper bins to encourage staff to think more carefully about personal recycling.

Redundant electronic and electrical equipment is passed to an external contractor who expunges all data to a standard set by government and then recycles the hardware; redundant furniture is disposed of by way of re-use or environmental destruction; and electricity consumption has been reduced by replacing halogen lighting with lower energy alternatives and air conditioning units with more energy efficient units. Our reprographic equipment will only print on the input of a personal code, with a default setting for two-sided printing in black and white, reducing the amount of unnecessary printing and thus paper consumption. In addition, we have reduced the number of printed copies of each public report, issuing reports electronically where appropriate.

The Office’s procurement guidance requires procurement decisions to have regard to equality of opportunity and sustainable development. Much of what we procure, including services for the upkeep of our premises, is through Northern Ireland Civil Service (NICS) wide contracts. These contracts, established locally by the Department of Finance’s Central Procurement Directorate, are committed to delivering on the NICS’ sustainability, environmental, social and community objectives. For example, contractors are encouraged to work with small suppliers (i.e. fewer than 50 employees); micro suppliers (i.e. fewer than 10 employees) or Social Economy Enterprises throughout their supply chains. Payment to subcontractors should be made within 30 days of receipt of a valid invoice.

In seeking to reduce its environmental footprint, we have travel initiatives aimed at encouraging staff to avail of more sustainable modes of transport to travel to and from work:

- The NICS Cycle to Work scheme was implemented in 2013-14 and, to date, 21 NIAO staff have participated.

- A dual charging point for electric vehicles has been installed to encourage staff to switch to vehicles with cleaner fuels.

Our Accounts Payable Unit continues to issue electronic invoices and remittances to suppliers and staff, reducing paper and printing consumption and associated postal charges. The introduction of tablets has reduced consumption further, by replacing hard copy documents used at various internal and external meetings.

The Office continued its involvement with Business in the Community Northern Ireland (BITCNI), a membership organisation for companies that are committed to doing business responsibly and working together on societal issues where they can make a real difference. For the BITCNI “Be a Saint Day”, the Office volunteered with the National Trust at Castle Ward, to relay a playground surface and plant more than 50 trees. Members of staff also participated in the Time to Read and Time to Count programmes at local schools.

In addition, various other fund-raising events were arranged to support a number of very worthwhile charities.

Kieran Donnelly

Comptroller and Auditor General for Northern Ireland

26 June 2019

Accountability Report

£6.93 million: Net Resource Outturn for 2018-19

Auditor’s report: Unqualified independent auditor’s report

8.2% £556,000: Net Resource Outturn savings (excluding VES) compared with last year

£6.21 million: Staff Costs

93 Other Staff:

- 44 male

- 49 female

6 Senior Management Team:

- 4 male

- 2 female

99 FTE: Staff in post at 31 March 2019

CORPORATE GOVERNANCE REPORT

The purpose of the corporate governance report is to explain the composition and organisation of the NIAO’s governance structures and outline how they support the achievement of our objectives.

Directors’ Report

The directors of the NIAO comprise the senior managers and the non-executive members, whose details are set out below.

NIAO Senior Management Team

Subject to the C&AG’s statutory position as corporation sole and his primacy in setting strategy, policy and procedures, the Senior Management Team (SMT) is the principal mechanism for directing the business and decision making in the NIAO. This team is chaired by the C&AG and its membership over the reporting period was as follows:

Senior Management Team

C&AG’s Advisory Board

The Advisory Board is responsible for providing objective and impartial advice to the C&AG to assist him in the discharge of his functions, and works in partnership with the Comptroller and Auditor General and the Senior Management Team. The Board scrutinises the work of the NIAO in the five areas of strategic clarity, commercial sense, talented people, results focus and management information. It also scrutinises and advises on Office finances on an ongoing basis.

The Advisory Board comprises both executive (C&AG and Chief Operating Officer (COO)) and non-executive members, the latter bringing an independent and external perspective to the work of the Board.

The Chairperson of the Advisory Board is appointed by the C&AG through open competition, based on merit, following endorsement by the Audit Committee of the Assembly.Non-executive members will be similarly engaged and will be members of the Advisory Board.

Each non-executive member is appointed for a three year period, which may be extended for a maximum of a further three years by the C&AG with the endorsement of the Audit Committee of the Assembly.

In 2018-19, the Advisory Board’s membership was as follows:

Martin Pitt (Chair from December 2018)

In December 2018, the Officeappointed Martin Pitt as the new Chairperson of the Advisory Board. He was previously a partner within PwC’s Audit and Assurance Team and Head of Internal Audit, bringing with him over 30 years’ experience working with public and private sector bodies across the UK. Throughout his career, he has advised organisations on issues relating to corporate governance and risk management.

Paul Douglas (until 17 November 2018)

Up until November 2018, Paul Douglas was the Chairperson of the Advisory Board. He had 28 years’ experience in a large public sector organisation, the PSNI, with 15 years as a senior manager. Between 2008 and 2010, he was involved in the strategic change process as his area moved from four districts to one. He currently serves as a Lay Commissioner with the N.I. Judicial Appointments Commission.

Áine Gallagher (until 17 November 2018)

Áine Gallagher previously worked as the Director of Corporate and Business Services for the Northern Ireland Hospice; Director of Operations for Culture Company 2013 Ltd; as a member of the Corporate Finance Appraisal and Advisory Division in Invest NI; and with PwC, where she trained as a Chartered Accountant and worked for 10 years in both the audit and advisory departments.

Pat Cumiskey (until 6 November 2018)

Pat Cumiskey has over 40 years’ experience in a number of audit and senior financial management positions in the public sector, including a five-year spell, initially as a CIPFA trainee, in the early years of the NIAO. He was Acting Chief Executive in 2014 in Banbridge District Council, leading the council through its final year. He currently serves as a Lay-member to the Northern Ireland Valuation Tribunal.

Pamela McCreedy

Chief Operating Officer

As Chief Operating Officer, Pamela McCreedy leads and manages the NIAO’s operational business and supports the C&AG in the strategic leadership of the NIAO, including stakeholder management. She is responsible for cultural change within the NIAO, and for developing greater flexibility in management structures and service delivery. She has also been appointed Local Government Auditor from 1 February 2018, with responsibility for leading all local government audits across Northern Ireland.

Three further non-executive members were appointed to the Advisory Board, effective from 1 April 2019.

Professor Noel Hyndman

Professor Noel Hyndman has been Professor of Accounting at Queen’s University Belfast since 2002. Previously he was Professor of Accounting at the University of Ulster (until 2002) and has held Visiting Professorships at the University of Ottawa in Canada and the University of Sydney in Australia, as well as being an Erskine Fellow at the University of Canterbury in New Zealand. He is a Chartered Global Management Accountant and a Fellow of the Chartered Institute of Management Accountants. He is currently Chair of the British Accounting and Finance Association’s (BAFA’s) Public Services and Charities Special Interest Group, and a member of BAFA’s Executive Committee. Professor Hyndman has been Academic Advisor to the Chartered Accountants Ireland Educational Trust since 2011.

Marie Mallon (MBE)

Marie Mallon (MBE) is Chair of the Labour Relations Agency, a position she has held since 2014. Prior to that she was Director of HR and Deputy CEO of Belfast Health and Social Care Trust for seven years, having previously held the position of Director of HR with the Royal Hospitals Trust. Mrs Mallon is a Chartered Member of the Chartered Institute of Personnel and Development (CIPD) and obtained a distinction in her MSc in HR Leadership from University of Manchester. She is currently an associate of the Health and Social Care Leadership Centre and also undertakes independent HR consultancy. She has recently been appointed Chair of the Chairs’ Forum and in 2015 she was awarded an MBE in the Queen’s birthday honours list for services to health and social care.

John Turkington

John Turkington is Principal of Turkington Chartered Accountants and previously held senior roles as Director of Corporate Banking, Director of Property Banking and Regional Director of Commercial Banking with the Ulster Bank for 11 years. He has more recently held an all-island role in Specialised Relationship Management in the Ulster Bank, following a career in practice. He is a graduate in accounting and LLB Law, with a post-graduate Diploma in Accounting from Queen’s University Belfast, and a Fellow of the Chartered Accountants of Ireland.

NIAO Audit and Risk Assurance Committee

The C&AG, as the Accounting Officer of the NIAO, is responsible for ensuring that there are effective arrangements for governance, risk management and internal control.

The Advisory Board supports the C&AG in this role by reviewing the comprehensiveness and reliability of assurances on governance, risk management, the control environment and the integrity of financial statements and the annual report.

To provide support in these functions, the Board appoints an Audit and Risk Assurance Committee to review the comprehensiveness of assurances on systems of internal control, risk management and corporate governance. The Audit and Risk Assurance Committee is independent of all NIAO operational activities and is composed solely of non-executives.

In 2018-19, its membership was as follows:

Non-Executives

- Áine Gallagher (Chair) until 17 November 2018

- Pat Cumiskey until 6 November 2018

- Paul Douglas until 17 November 2018

- Gillian Body until 7 September 2018

Gillian Body (until 7 September 2018)

Gillian Body retired from the Wales Audit Office in June 2017 with over 35 years’ experience in public audit. She was previously Assistant Auditor General with the Wales Audit Office, where she was responsible for the full range of value for money work undertaken by that Office across the Welsh public sector. She is CIPFA qualified and spent her early career working for the National Audit Office. She also had secondments with the Office of the Comptroller and Auditor General in Dublin and with the Australian National Audit Office in Canberra.

From 1 April 2019, the membership of the Committee is:

Dr Noel Hyndman (Chairperson)

Marie Mallon MBE

John Turkington

Register of interests

None of the non-executive or executive members of the Office’s governance structures in 2018-19 held company directorships or significant interests which might conflict with their responsibilities. Also, none had any other related party interests.

Auditor of the NIAO

The Department of Finance has re-appointed Baker Tilly Mooney Moore as the external auditor of the NIAO for a three-year term commencing with the audit of the 2018-19 accounts, with the option to extend for a further two years.

In addition to its work to form an opinion on the financial statements, Baker Tilly Mooney Moore reviews the NIAO’s statement of financial impact which is reported on page 19. Details of the cost of the work done by the external auditor are disclosed in Note 4 to the Financial Statements.

Disclosure of relevant audit information

The C&AG has taken all the steps that he ought to have taken to make himself aware of any relevant audit information and to establish that the auditors are aware of that information. So far as the C&AG is aware, there is no relevant information of which the auditors are unaware. The C&AG has taken personal responsibility for the annual report and accounts and the judgments required for ensuring they are fair, balanced and understandable.

Personal data-related incidents

There were no protected personal data-related incidents which required reporting to the Information Commissioner’s Office (ICO). However, the ICO was made aware of an incident concerning an internal data breach in our human resources system. An internal investigation was completed and we are content that settings are accurate and appropriate and any future software upgrades will prompt a control check on permissions. In addition the ICO has confirmed that no further action is required.

Complaints

We have a complaints process in place to ensure that complaints from both clients and the public are dealt with in a timely, open and fair way, in line with public sector good practice. The process has three stages, the details of which can be found on our website at www.niauditoffice.gov.uk/index/contact_us/complaints_page.htm. If a complainant remains dissatisfied following the outcome of these three stages, they may refer the matter to the Northern Ireland Public Services Ombudsman’s Office, in accordance with the Northern Ireland Public Services Ombudsman Act (Northern Ireland) 2016.

During 2018-19, we received seven complaints. Four of these were reported to the NIAO, two were referred to the NI Public Services Ombudsman (NIPSO) and one was reported to the Information Commissioner’s Office (ICO). Five cases are closed; two remain open, one under consideration with NIPSO and one being processed by the NIAO.

Further information on the monitoring of complaints can be requested from:

Information Manager

Northern Ireland Audit Office

106 University Street

Belfast

BT7 1EU

028 9025 1097

Health and Safety

Our health and safety policy is made available to all staff. Suitably trained staff perform health and safety responsibilities.

No incidents were recorded during 2018-19 and no report to the Health and Safety Executive for Northern Ireland under the Reporting of Injuries, Diseases and Dangerous Occurrences Regulations was required.

All staff have access to an independent and confidential counselling, support and advice service. This counselling support is free to staff at the point of use and is totally external to the Office.

Statement of Accounting Officer’s Responsibilities

Under Article 6(3) of the Audit (Northern Ireland) Order 1987, the NIAO is required to prepare, for each financial year, resource accounts of the kind mentioned in Section 9 of the Government Resources and Accounts Act (Northern Ireland) 2001, detailing the resources acquired, held or disposed of during the year and the use of resources by the NIAO during the year.

The accounts are prepared on an accruals basis and must give a true and fair view of the state of affairs of the NIAO and of its net resource outturn, application of resources, changes in taxpayers’ equity and cash flows for the financial year.

In preparing these accounts, the Accounting Officer is required to comply with the requirements of the Government Financial Reporting Manual and in particular to:

- observe the relevant accounting and disclosure requirements, and apply suitable accounting policies on a consistent basis;

- make judgments and estimates on a reasonable basis;

- state whether applicable accounting standards, as set out in the Government Financial Reporting Manual, have been followed, and disclose and explain any material departures in the accounts;

- prepare the accounts on a going concern basis; and

- confirm that the Annual Report and Accounts as a whole is fair, balanced and understandable, and take personal responsibility for the Annual Report and Accounts and the judgements required for determining that it is fair, balanced and understandable.

Under the Audit (Northern Ireland) Order 1987, the Department of Finance has appointed the C&AG for Northern Ireland as Accounting Officer for the Northern Ireland Audit Office.

The C&AG for Northern Ireland’s relevant responsibilities as Accounting Officer, including responsibility for the propriety and regularity of the NIAO’s finances for which he is answerable, for the keeping of proper records and for safeguarding the NIAO’s assets, are set out in Managing Public Money Northern Ireland, published by the Department of Finance.

As the Accounting Officer, the C&AG takes all the steps that he ought to have taken to make himself aware of any relevant audit information and to establish that the NIAO’s auditors are aware of that information. So far as he is aware, there is no relevant audit information of which the auditors are unaware.

Governance Statement

Introduction

As Accounting Officer for the NIAO, I have responsibility for maintaining effective governance and a sound system of internal control that supports the achievement of the NIAO’s policies, aims and objectives, while safeguarding the public funds and assets for which I am personally responsible, in accordance with the responsibilities assigned to me in Managing Public Money Northern Ireland.

Structure of governance

The NIAO’s governance structure reflects the statutory position of the C&AG, as set out in two key pieces of legislation:

- The Audit (Northern Ireland) Order 1987 provided for the office of C&AG to be a corporation sole and established the NIAO to assist the C&AG in the discharge of his statutory functions.

- The Northern Ireland Act 1998 requires that, in exercising his functions, except for any function conferred on him of preparing accounts, the C&AG shall not be subject to the direction or control of any Minister or Northern Ireland department or the Assembly. Accordingly, the C&AG has complete discretion in the discharge of his statutory audit functions, with responsibility for the programme of audit work, all audit opinions and judgements resting with him alone.

As the holder of this office, I have primacy in determining the strategy, staffing and structure of the Office and am responsible for designing and implementing the internal governance arrangements to support the delivery of my statutory functions. In so doing, I seek to comply with the spirit of the ‘Corporate governance in central government departments: Code of good Practice NI 2013’ (“the Code”) issued by the Department of Finance. I accept the tenets of the Code as constituting best practice, however the specific legal constitution of the office of C&AG as a corporation sole means that I cannot directly apply the 2013 Code arrangements to the NIAO. In particular there is no provision in legislation for the establishment of a board.

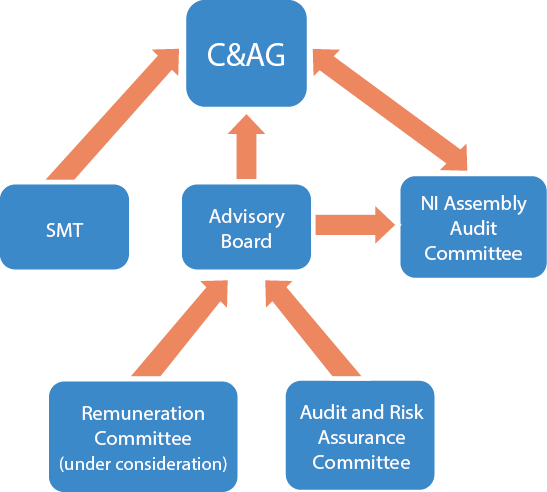

The internal governance arrangements of the NIAO that I have established are illustrated below. They are also set out in a ‘Memorandum of Understanding on the Governance and Accountability Arrangements of the Northern Ireland Audit Office’ (MoU) agreed with the Audit Committee of the Assembly, which oversees the performance of the NIAO (available on the NI Assembly website ).

NIAO Governance Structure

In 2018-19 I re-examined the role, responsibilities and membership of both the Advisory Group (renamed the Advisory Board) and the Audit and Risk Assurance Committee. I also intend to agree a revised Memorandum of Understanding with the Audit Committee of the Assembly when it returns following its current impasse.

Overall I am content that the NIAO governance arrangements are compliant with the Code on an appropriate and proportionate basis.

Components of governance structure

NI Assembly Audit Committee

The NI Assembly did not sit during 2018-19, given the ongoing political impasse. However, on its return, I will be accountable to it via the Assembly Audit Committee, which has the role defined in section 66 of the Northern Ireland Act 1998. The Audit Committee’s responsibilities include: examining the NIAO Estimate and laying it before the Assembly; considering the NIAO’s Corporate Plan; examining the NIAO Annual Report and Accounts and reports received from the external auditor; providing advice to the Department of Finance on the appointment of the NIAO external auditor; and tabling a motion in the Assembly in respect of the salary of the C&AG.

The key elements of the internal governance arrangements of the Office are detailed below. Further information on these, including minutes of meetings, are available at: www.niauditoffice.gov.uk/governance-niao.

C&AG’s Advisory Board

For the period up to 23 October 2018, the role of the Advisory Board (previously known as the Advisory Group) was to provide objective and impartial advice to assist me in the discharge of my functions. The group scrutinised the work of the NIAO in the five areas of strategic clarity, commercial sense, talented people, results focus and management information, as set out in the 2013 Code.

The Advisory Board comprised both executives (the C&AG and the COO) and non-executives, the latter bringing an independent and external perspective to the work of the group.

In 2018-19, the Advisory Board met only once, focussing on the Office’s Business Transformation Programme and its Three-Year Work Programme. The attendance at the meeting is recorded below:

|

Members present |

C&AG’s Advisory Group 19/06/2018 |

|---|---|

|

Kieran Donnelly (C&AG) |

Yes |

|

Paul Douglas (Chair) |

Yes |

|

Áine Gallagher |

|

|

Pat Cumiskey |

Yes |

|

Pamela McCreedy (COO) |

Yes |

In addition, other officials of the Office attended, as required, to assist with the discussion of agenda items. The Office’s corporate secretariat provided it with an appropriate support service.

The Advisory Board stood down when the non-executive members’ contracts came to an end in the period September to November 2018.

A new Advisory Board has since been formed and held its first meeting on 30 May 2019.

NIAO Audit and Risk Assurance Committee

For the period up to 23 October 2018, the NIAO Audit and Risk Assurance Committee’s (ARAC) membership comprised non-executives only. One post was allocated to a representative from a public audit agency in the UK or Ireland. Other members were appointed by open competition, based on merit, and were members of the C&AG’s Advisory Board.

Its role was to support me, as Accounting Officer, in my responsibility for issues of risk, control and governance, by reviewing the comprehensiveness, reliability and integrity of assurances. This included supporting and advising me on the planned activity and results of both internal audit and external audit (see page 37) and the adequacy of management’s response to issues identified by audit activity, including external audit’s management letter.

Attendance of members in 2018-19 was as follows:

|

Members present |

NIAO Audit and Risk Assurance Committee |

||

|---|---|---|---|

|

17/05/2018 |

19/06/2018 |

23/10/2018 |

|

|

Áine Gallagher (Chair) |

Yes |

Yes |

Yes |

|

Paul Douglas |

Yes |

||

|

Gillian Body |

Yes |

Yes |

|

|

Pat Cumiskey |

Yes |

Yes |

Yes |

Following the October 2018 meeting and subsequent to each of the non-executives completing their terms of appointment, governance arrangements were re-structured, as set out at page 41, which will impact on the role and reporting arrangements of ARAC.

Under the new structure, ARAC comprises three non-executive Board members of the NIAO, excluding the NIAO Board Chairperson, who may attend by invitation, if required. The Chairperson of the newly formed ARAC, appointed by the Board Chairperson, is Dr. Noel Hyndman.

Each member is appointed for a three-year period, which may be extended for a further three years by the C&AG with the endorsement of the Audit Committee of the Assembly.

ARAC remains independent of all NIAO operational activities; its terms of reference are available at https://www.niauditoffice.gov.uk/audit-committee. It will meet at least four times a year. The Chairperson of the Committee may convene additional meetings, as deemed necessary. It may request the attendance of officials of the Office to assist with its discussions on any particular matter.

Given that the ARAC Chairperson’s term came to an end following the October 2018 meeting and the newly appointed Committee did not meet in the reporting period, it was not possible to complete an Annual Report summarising the Committee’s work. However, in these unusual circumstances, I am satisfied that while the Committee was in place, it discharged its duties as guided by its Terms of Reference, and taking account of the work of internal and external audit and assurances provided to the Committee, every effort was made to review and oversee internal control and risk management arrangements and to provide assurances to me, as Accounting Officer, in the discharge of my accountability obligations.

The newly appointed ARAC met on 7 May 2019 and it has provided me with constructive feedback on its terms of reference and on the risks to the NIAO. It has also agreed a draft programme of work for 2019-20.

NIAO Senior Management Team

The Senior Management Team comprises myself, as Chair, the Chief Operating Officer and five Directors.

The Senior Management Team meets monthly and is responsible for the strategic and operational leadership of the Office. Subject to my statutory position as a corporation sole and head of the NIAO, the team is the principal mechanism for directing business and decision making in the Office. In alignment with the Code, the business of the team covered the five key areas of strategic clarity, commercial sense, talented people, results focus and management information.

The Senior Management Team, which met 10 times during the year, covered normal scheduled business. There was over 90 per cent attendance of members at all meetings.

Relevant non-members are invited to attend these meetings. Over the course of the year, attendance took place in relation to items such as the contracting out of audit work, the implications of Brexit, office accommodation, provision of better performance information, the development of data analytics, continuous development in stakeholder engagement, the Voluntary Exit Scheme and the Business Transformation Programme.

During the year the Business Transformation Programme was progressed under the five key pillars of Communication and Engagement; Digitalisation; People; Governance and Audit Practice; and the Working Environment, under which 20 separate work streams have been identified, initiated, progressed and monitored.

As part of this process, our Digital Services Strategy has recognised that we have access to a wide range of data from financial management systems as well as open data, but we lack the technology to use this data to its full potential. In recognition of this we have gone through the Small Business Research Initiative (SBRI) and then the GovTech Catalyst processes, where we have sought assistance and obtained significant funding to address this issue. We have now appointed five separate suppliers to work up potential solutions, from which one (or possibly two) may be selected to progress to stage 2 development.

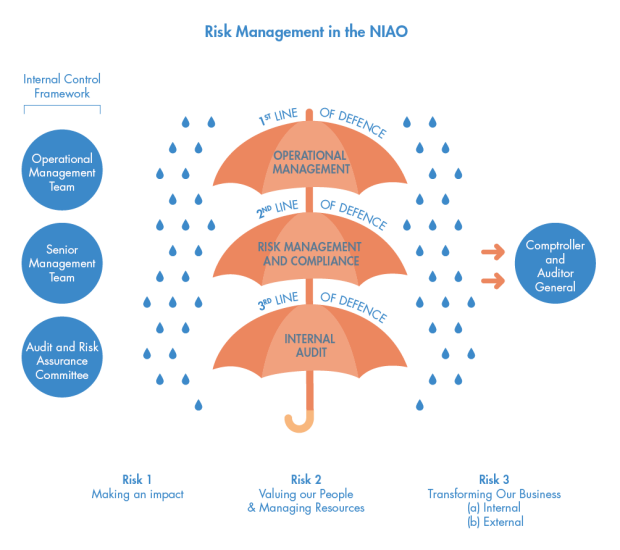

Risk management and control

Our approach to risk management is guided by professional best practice, and takes full cognisance of the context and environment in which we operate. Because of our public profile and the very nature of our work, we must uphold the highest standards in our own operations, and be able to stand the test of independent scrutiny and retain our credibility and reputation with the Assembly, audited bodies and other stakeholders. At the same time, we must ensure that we promote and secure value for money in our use of public funds.

We focus on proportionate risk management as an integral part of the way we undertake business activities. Risk is managed in a structured way, taking on board the combination of the likelihood of something happening and the impact which arises if it does actually happen, to assess the inherent risk. We then set out the actions, if any, we take to constrain the risk to an acceptable level in accordance with our risk appetite. I am responsible for determining the risk appetite of the Office, which I review on an ongoing basis. To this end, I have agreed a definition for the appetite of each risk in consultation with both the SMT and ARAC.

The risk that remains, taking on board these actions, is our residual risk. In applying these principles, we are accurately assessing the relative significance and prioritisation of each risk. We have a comprehensive risk management strategy which sets out roles and responsibilities and determines procedures for risk identification, monitoring, reporting and escalation of issues.

During 2018-19, Risk Management was a regular item at the meetings of the SMT and ARAC. The Corporate Risk Register Working Group (the Working Group), which is responsible for directly briefing the SMT and, by extension, ARAC on risk management developments, meets at least four times per year. In 2018-19 it met seven times to address various risk-related issues. The timing of its meetings and subsequent outputs dovetail with SMT and ARAC requirements.

As part of this process, the Working Group compiles a single corporate risk register which incorporates a risk assurance framework, with three lines of defence. This has been constructed in a structural and systematic way, as set out below, to facilitate the identification, assessment and ongoing monitoring of risks significant to the NIAO. It is reviewed on a regular basis.

Following the completion of the new Strategic Corporate Framework for 2018-21, we have set three key priorities:

- provide assurance, add value and promote excellence in public administration;

- support public sector transformation in Northern Ireland; and

- transform our business to meet the emerging challenges of the future.

As a result we have revised our corporate risk register to ensure that the risks identified align with our priorities, and identified three key areas of risk: making an impact; valuing our people and managing resources; and transforming our business (external and internal).

During the reporting period, a number of additional assessments were completed on the risks associated with fraud, bribery and corruption and cyber security. These were completed following the Office’s own “Managing Fraud Risk” and “Managing the Risk of Bribery and Corruption: A Good Practice Guide for the Northern Ireland Public Sector” good practice guides and the National Audit Office’s good practice guide “Cyber Security and Information Risk Guidance for Audit Committees”. Any issues arising from these assessments were discussed by the SMT and action plans were devised to address the issues arising as appropriate. The action plans were also presented to ARAC.

Quality

We apply the International Standard on Quality Control (ISQC 1), incorporating monitoring arrangements to ensure that our financial audit has complied with our audit methodology and underlying professional auditing standards. We require annual confirmation of compliance. During the reporting period, eight accounts were reviewed by teams independent of the audit team. Five of the reviews were conducted by teams from the other UK public audit agencies.